The Fair Debt Collection Practices Act (FDCPA) prohibits harassment or abuse in collecting a debt such as threatening violence, use of obscene or profane language, publishing lists of debtors who refuse to pay debts, or even harassing a debtor by repeatedly calling the debtor on the phone. Also, certain false or misleading representa?¬tions are forbidden, such as representing that the debt collector is associated with the state or federal government, or stating that the debtor will go to jail if he does not pay the debt. This Act also sets out strict rules regarding communicating with the debtor.

The FDCPA applies only to those who regularly engage in the business of collecting debts for others -- primarily to collection agencies. The Act does not apply when a creditor attempts to collect debts owed to it by directly contacting the debtors. It applies only to the collection of consumer debts and does not apply to the collection of commercial debts. Consumer debts are debts for personal, home, or family purposes.

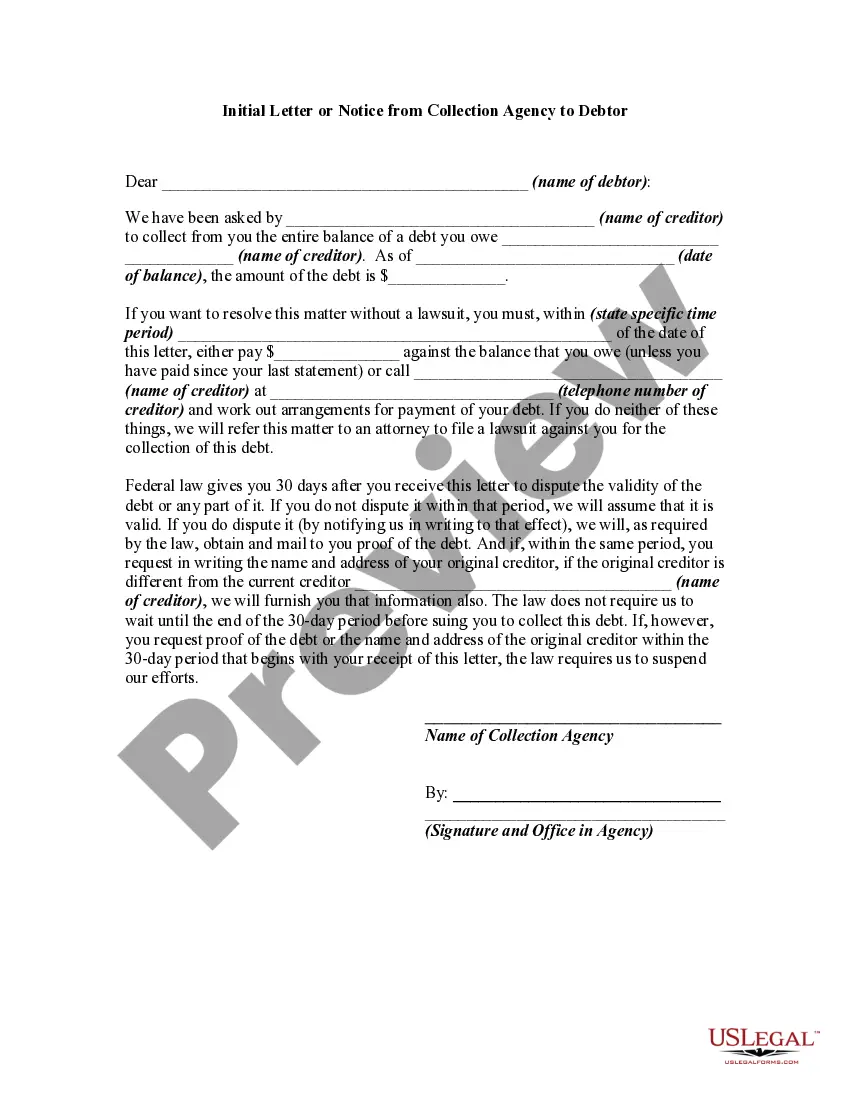

In Alabama, an Initial Letter or Notice from a Collection Agency to a Debtor is a significant step in the debt collection process. It serves as a formal communication directed towards the debtor, informing them about an outstanding debt that is overdue or in default. This initial notice aims to establish contact with the debtor and notify them about their debt obligations while providing an opportunity to resolve the matter before further collection actions are initiated. The Alabama Initial Letter or Notice from a Collection Agency to a Debtor typically includes the following key elements: 1. Identification: The letter begins with the identification of the collection agency, including its name, address, contact information, and the agency's identification number as required by Alabama law. 2. Debtor Information: The notice contains details about the debtor, such as their name, address, and any other relevant identifying information specific to the debt in question. 3. Creditor Information: The initial notice also mentions the original creditor's name, address, and contact information, informing the debtor about the entity to whom the debt is owed. 4. Debt Details: The letter provides a clear and detailed description of the debt, including the original amount owed, the outstanding balance, any accrued interest or fees, the date of default, and a breakdown of the charges if applicable. 5. Acknowledgment of Debt: The debtor is informed that they have a legal obligation to pay the debt and are requested to acknowledge the debt's validity by responding within a specified timeframe, usually around 30 days. Failure to dispute the debt within this timeframe generally results in the assumption of its validity. 6. Validation Request: The notice informs the debtor of their right to request further information that substantiates the debt's existence and its details. This includes instructions on how to request validation if the debtor believes they do not owe the debt or if there are discrepancies. 7. Repayment Options: The notice may provide information about potential payment arrangements and options available to the debtor, encouraging them to contact the collection agency to discuss a resolution. The letter may also highlight the benefits of promptly addressing the debt to avoid further consequences. 8. Legal Actions: Depending on the nature and amount of the debt, the initial letter or notice may warn the debtor about potential legal actions that the collection agency might take if the debt remains unresolved. This may include the possibility of filing a lawsuit, wage garnishment, property liens, or reporting the debt to credit bureaus, which can negatively impact the debtor's credit score. Types of Alabama Initial Letters or Notices from Collection Agencies to Debtors: 1. Initial Debt Collection Notice: This is a generic notice sent to inform the debtor about their unpaid debt and initiate communication. 2. Compliance Notice: In cases where the debtor disputes the validity of the debt within the specified timeframe, the agency may send a compliance notice, acknowledging the dispute and requesting additional information or documentation from the debtor. 3. Demand for Payment: If the debtor fails to respond or resolve the debt after receiving the initial notice, the collection agency may send a more assertive demand for payment, emphasizing the consequences of continued non-payment. 4. Final Notice: If the debt remains unpaid despite previous attempts, a final notice is often sent as a last opportunity for the debtor to settle the debt voluntarily before further collection actions are pursued. It's important to note that each collection agency's initial letters or notices may have slight variations in formatting and wording. Debtors should carefully review these documents, verify their legitimacy, and take appropriate action to address their outstanding debts promptly.