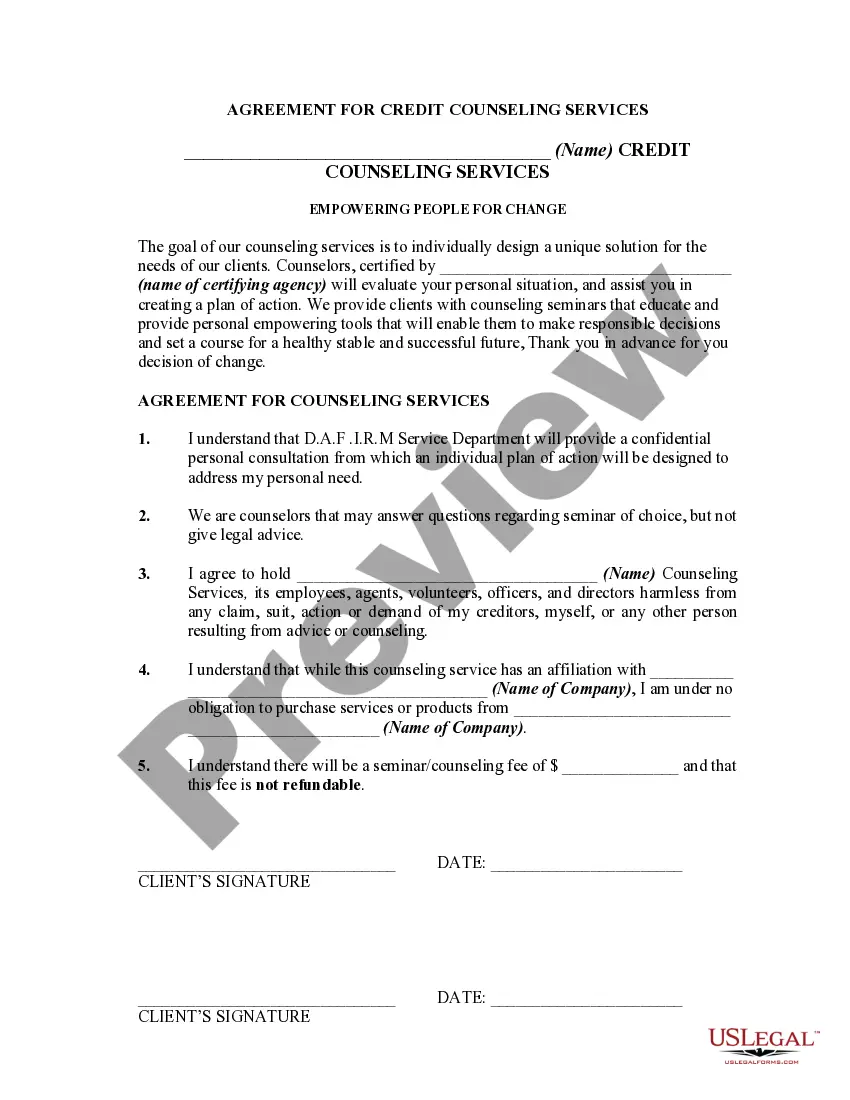

This type of form may be used in connection with a credit counseling seminar which also includes individual credit counseling. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Alabama Agreement for Credit Counseling Services is a legal document that outlines the terms and conditions agreed upon between the credit counseling service provider and the consumer seeking assistance with their debts in the state of Alabama. This agreement is essential to ensure both parties are aware of their rights, responsibilities, and obligations. The Alabama Agreement for Credit Counseling Services typically includes the following key elements: 1. Parties involved: Clearly identifies the credit counseling agency and the client seeking financial counseling services. 2. Purpose: States the objective of the agreement, which is usually to provide the client with comprehensive assistance and guidance in managing their debts effectively. 3. Services offered: Describes the range of credit counseling services available to the client, such as budgeting assistance, debt management plans, financial education, or debt consolidation options. 4. Client's responsibilities: Outlines the client's obligations, which may include providing accurate financial information, maintaining regular payments towards debts, attending counseling sessions, and adhering to the agreed-upon plan. 5. Fees and payments: Specifies any fees associated with the credit counseling services and their payment structure, ensuring transparency in the financial arrangement. This section may also mention any fee waivers or reductions available for low-income clients. 6. Confidentiality: Highlights the importance of maintaining confidentiality of the client's personal and financial information in accordance with applicable laws and regulations. 7. Term and termination: Defines the duration of the agreement and the circumstances under which either party can terminate the agreement, typically with prior notice. 8. Dispute resolution: Details the process for resolving any disputes or disagreements that may arise during the course of the credit counseling relationship, such as mediation or arbitration. Different types of Alabama Agreement for Credit Counseling Services can include variations based on the specific programs offered by credit counseling agencies. Some notable types are: 1. Debt Management Agreement: If the consumer decides to enroll in a debt management plan, a separate agreement may be established, outlining additional terms related to the repayment schedule and disbursement of funds to creditors. 2. Housing Counseling Agreement: For individuals seeking assistance with mortgage or housing-related financial issues, a specialized agreement focusing on housing counseling may be provided. 3. Bankruptcy Counseling Agreement: In cases where clients require credit counseling prior to filing for bankruptcy, a specific agreement tailored to bankruptcy counseling services will be used. In conclusion, the Alabama Agreement for Credit Counseling Services is a comprehensive document that outlines the responsibilities and expectations of both the credit counseling agency and the consumer seeking financial assistance. It ensures transparency, clarity, and legal protection for both parties involved in the credit counseling process.Alabama Agreement for Credit Counseling Services is a legal document that outlines the terms and conditions agreed upon between the credit counseling service provider and the consumer seeking assistance with their debts in the state of Alabama. This agreement is essential to ensure both parties are aware of their rights, responsibilities, and obligations. The Alabama Agreement for Credit Counseling Services typically includes the following key elements: 1. Parties involved: Clearly identifies the credit counseling agency and the client seeking financial counseling services. 2. Purpose: States the objective of the agreement, which is usually to provide the client with comprehensive assistance and guidance in managing their debts effectively. 3. Services offered: Describes the range of credit counseling services available to the client, such as budgeting assistance, debt management plans, financial education, or debt consolidation options. 4. Client's responsibilities: Outlines the client's obligations, which may include providing accurate financial information, maintaining regular payments towards debts, attending counseling sessions, and adhering to the agreed-upon plan. 5. Fees and payments: Specifies any fees associated with the credit counseling services and their payment structure, ensuring transparency in the financial arrangement. This section may also mention any fee waivers or reductions available for low-income clients. 6. Confidentiality: Highlights the importance of maintaining confidentiality of the client's personal and financial information in accordance with applicable laws and regulations. 7. Term and termination: Defines the duration of the agreement and the circumstances under which either party can terminate the agreement, typically with prior notice. 8. Dispute resolution: Details the process for resolving any disputes or disagreements that may arise during the course of the credit counseling relationship, such as mediation or arbitration. Different types of Alabama Agreement for Credit Counseling Services can include variations based on the specific programs offered by credit counseling agencies. Some notable types are: 1. Debt Management Agreement: If the consumer decides to enroll in a debt management plan, a separate agreement may be established, outlining additional terms related to the repayment schedule and disbursement of funds to creditors. 2. Housing Counseling Agreement: For individuals seeking assistance with mortgage or housing-related financial issues, a specialized agreement focusing on housing counseling may be provided. 3. Bankruptcy Counseling Agreement: In cases where clients require credit counseling prior to filing for bankruptcy, a specific agreement tailored to bankruptcy counseling services will be used. In conclusion, the Alabama Agreement for Credit Counseling Services is a comprehensive document that outlines the responsibilities and expectations of both the credit counseling agency and the consumer seeking financial assistance. It ensures transparency, clarity, and legal protection for both parties involved in the credit counseling process.