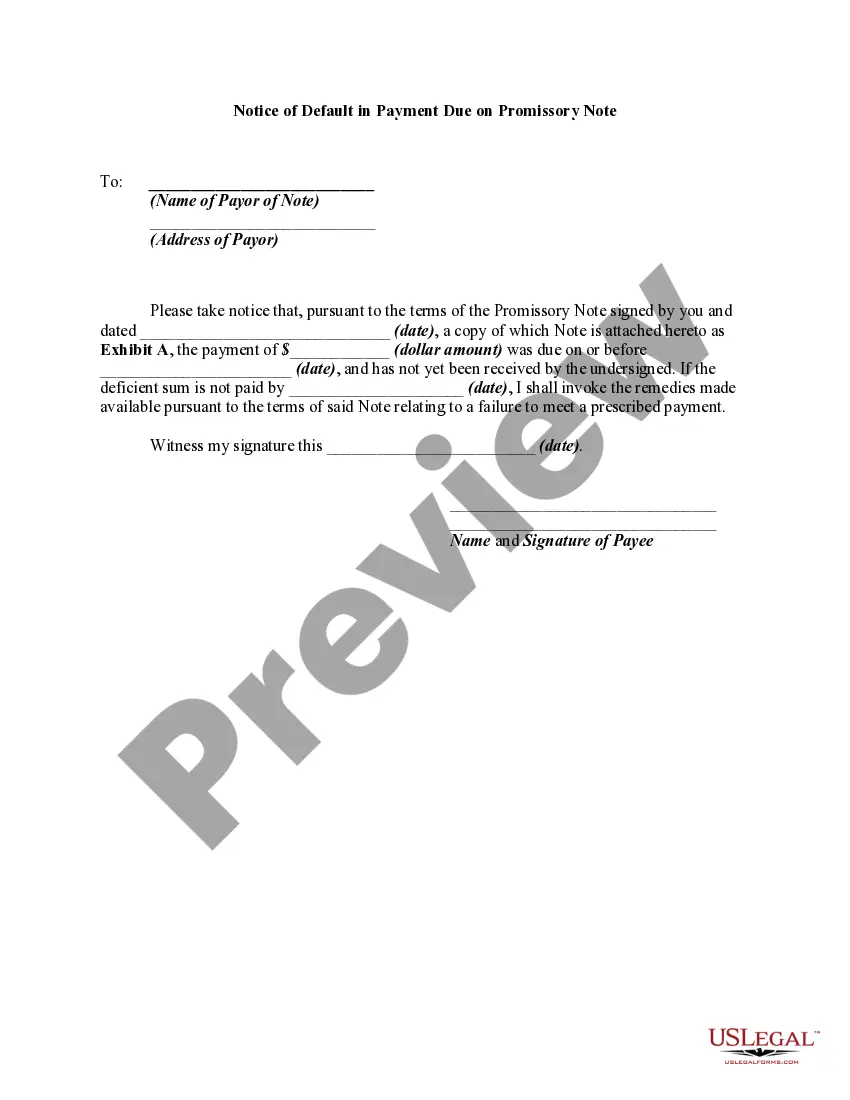

This form is a notice of a failure to make a required payment when due pursuant to a promissory note. The form also contains a warning to the breaching party that legal action will be taken unless the breach is remedied on or before a certain date. This form is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a notice in a particular jurisdiction.

The Alabama Notice of Default in Payment Due on Promissory Note is a legal document that signifies a borrower's failure to fulfill the payment obligations outlined in a promissory note. This notice serves as a formal notification to the borrower that they are in default and provides them with a specified period to rectify the situation. When a borrower fails to make scheduled payments on time as agreed upon in the promissory note, the lender may issue the Alabama Notice of Default in Payment Due on Promissory Note. This document alerts the borrower to the consequences of their non-payment and gives them an opportunity to take corrective action. Types of Alabama Notice of Default in Payment Due on Promissory Note: 1. Non-Judicial Notice of Default: In Alabama, lenders commonly use non-judicial foreclosure to handle default cases. Non-judicial proceedings do not require court involvement, and a specific notice of default is sent to the borrower, initiating the foreclosure process. 2. Judicial Notice of Default: In some situations, lenders may choose to pursue a judicial foreclosure process. This involves filing a lawsuit against the borrower, and a judicial notice of default is issued by the court to inform the borrower of their default status. 3. Notice of Default Cure Period: This type of notice grants the borrower a specific period, typically 30 days, to remedy the default by making the overdue payments, including any applicable fees and penalties. 4. Notice of Acceleration: If the borrower fails to cure the default within the provided grace period, the lender issues a notice of acceleration. This notice informs the borrower that the entire loan amount is now due, along with any accumulated interest or charges. 5. Notice of Foreclosure Sale: When all attempts to resolve the default fail, the lender issues a notice of foreclosure sale. This notice specifies the date, time, and location of the foreclosure sale, where the property securing the promissory note will be auctioned off to recover the outstanding debt. It is essential to understand the specific requirements and laws governing the Alabama Notice of Default in Payment Due on Promissory Note. Adhering to these regulations ensures a legally compliant process for both the lender and the borrower. Consulting with a qualified legal professional is advisable to navigate any complexities or disputes that may arise during the default resolution process.The Alabama Notice of Default in Payment Due on Promissory Note is a legal document that signifies a borrower's failure to fulfill the payment obligations outlined in a promissory note. This notice serves as a formal notification to the borrower that they are in default and provides them with a specified period to rectify the situation. When a borrower fails to make scheduled payments on time as agreed upon in the promissory note, the lender may issue the Alabama Notice of Default in Payment Due on Promissory Note. This document alerts the borrower to the consequences of their non-payment and gives them an opportunity to take corrective action. Types of Alabama Notice of Default in Payment Due on Promissory Note: 1. Non-Judicial Notice of Default: In Alabama, lenders commonly use non-judicial foreclosure to handle default cases. Non-judicial proceedings do not require court involvement, and a specific notice of default is sent to the borrower, initiating the foreclosure process. 2. Judicial Notice of Default: In some situations, lenders may choose to pursue a judicial foreclosure process. This involves filing a lawsuit against the borrower, and a judicial notice of default is issued by the court to inform the borrower of their default status. 3. Notice of Default Cure Period: This type of notice grants the borrower a specific period, typically 30 days, to remedy the default by making the overdue payments, including any applicable fees and penalties. 4. Notice of Acceleration: If the borrower fails to cure the default within the provided grace period, the lender issues a notice of acceleration. This notice informs the borrower that the entire loan amount is now due, along with any accumulated interest or charges. 5. Notice of Foreclosure Sale: When all attempts to resolve the default fail, the lender issues a notice of foreclosure sale. This notice specifies the date, time, and location of the foreclosure sale, where the property securing the promissory note will be auctioned off to recover the outstanding debt. It is essential to understand the specific requirements and laws governing the Alabama Notice of Default in Payment Due on Promissory Note. Adhering to these regulations ensures a legally compliant process for both the lender and the borrower. Consulting with a qualified legal professional is advisable to navigate any complexities or disputes that may arise during the default resolution process.