A secured transaction is created when a buyer or borrower (debtor) grants a seller or lender (creditor or secured party) a security interest in personal property (collateral). A security interest allows a creditor to repossess and sell the collateral if a debtor fails to pay a secured debt.

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use or business purposes.

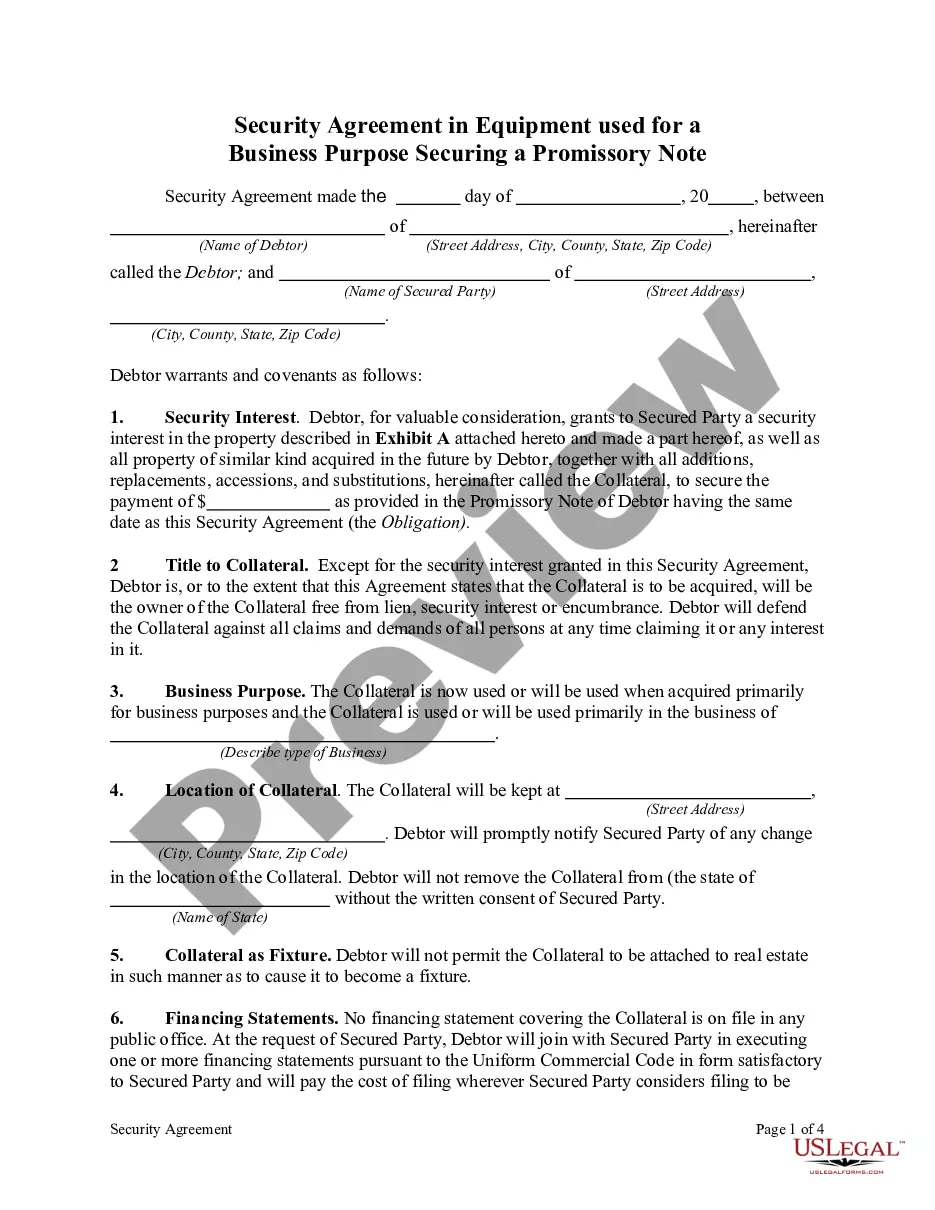

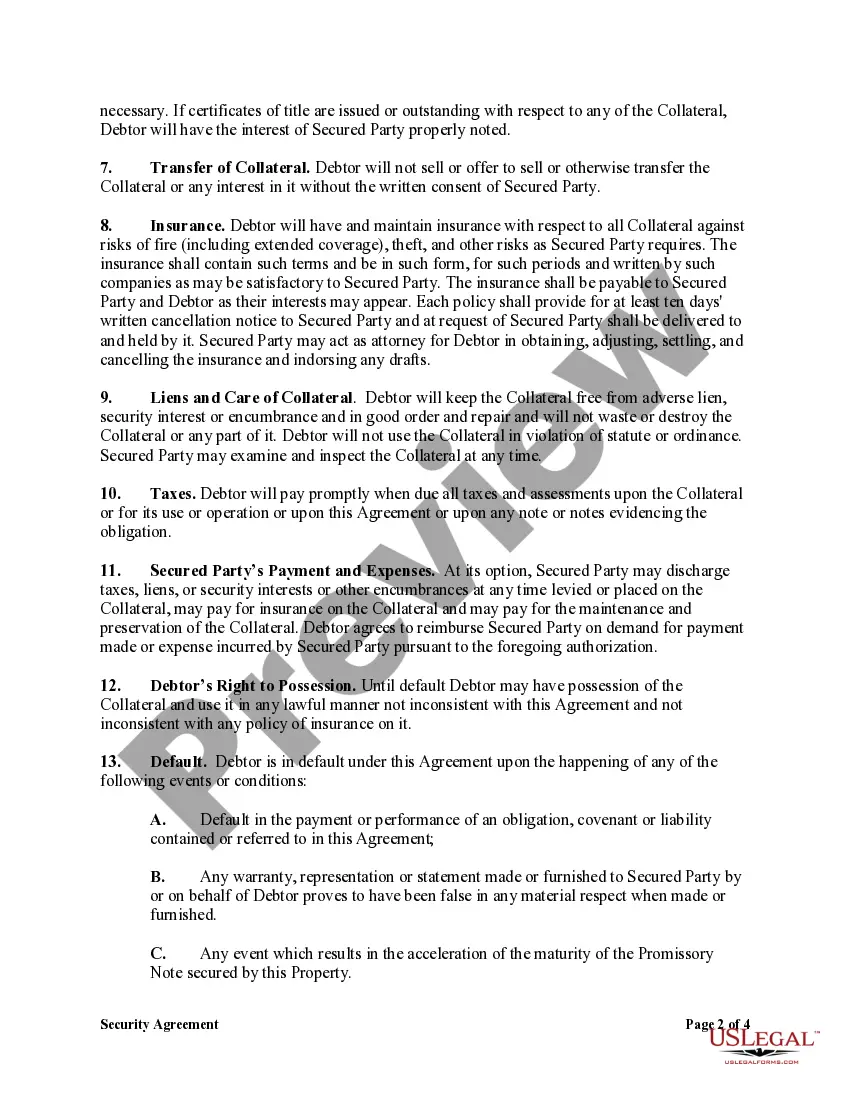

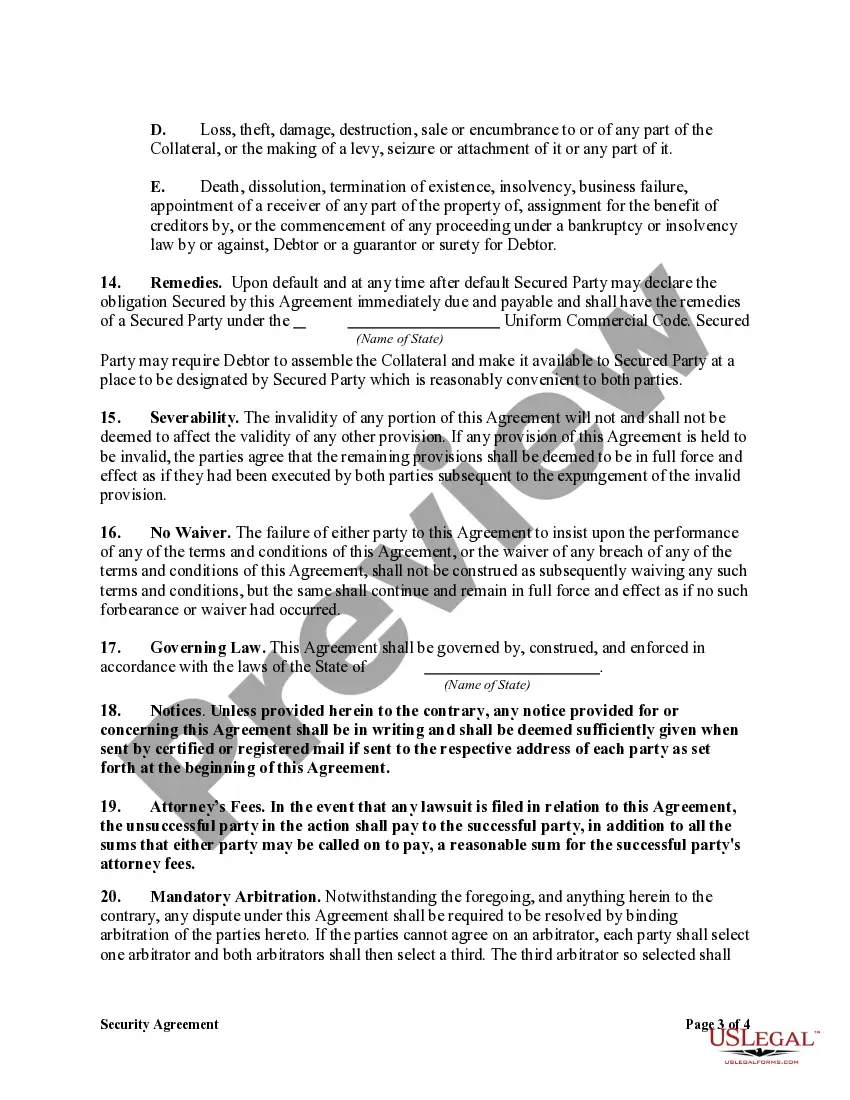

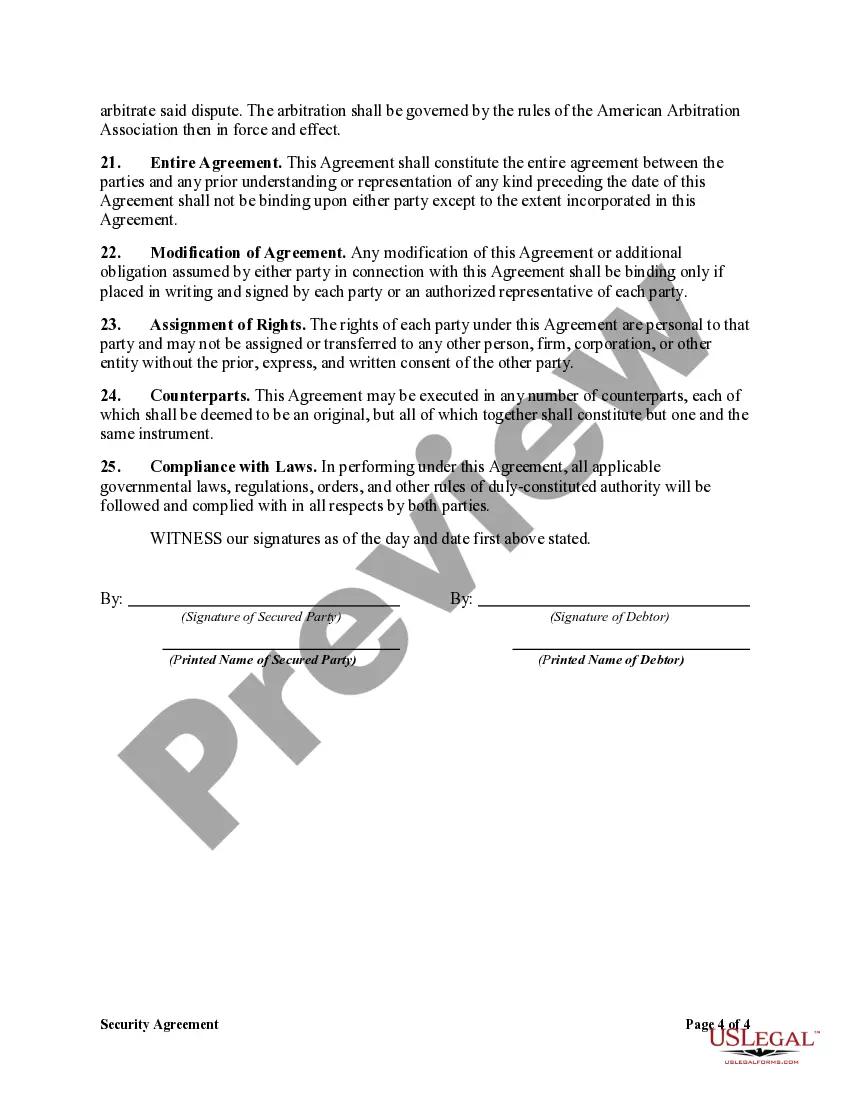

An Alabama Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a legal document that provides security for a promissory note in the state of Alabama. This agreement allows a lender to take possession of and sell the equipment listed in the agreement in the event that the borrower defaults on their loan payments. The equipment listed serves as collateral for the loan, giving the lender a right to reclaim their investment. The purpose of this agreement is to protect the lender's interest and provide assurance that they will be repaid in case the borrower fails to meet their obligations. By securing the promissory note with equipment, the lender gains a sense of security and reduces the risk associated with lending money. Some common types of Alabama Security Agreement in Equipment for Business Purposes — Securing Promissory Note include: 1. Conditional Sales Agreement: In this type of agreement, the lender retains the ownership of the equipment until the borrower pays off the entire loan amount. The borrower can use the equipment, but the ownership rights remain with the lender until the loan is fully repaid. 2. Chattel Mortgage: This type of agreement allows the lender to hold a lien on the equipment, giving them the right to repossess and sell the equipment if the borrower defaults on the loan. Once the loan is paid off, the lender releases the mortgage, transferring full ownership to the borrower. 3. Equipment Lease Agreement: A lease agreement allows the borrower to rent or lease the equipment from the lender for a specified period. The lender retains ownership and security interest in the equipment until the lease term ends or the borrower exercises an option to purchase the equipment. The Alabama Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a critical document for lenders and borrowers engaging in business transactions involving equipment purchases. It ensures that both parties are protected, providing legal recourse in case of financial difficulties or default. Seeking legal advice is recommended to draft a comprehensive and enforceable agreement that suits the specific needs and circumstances of the parties involved.An Alabama Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a legal document that provides security for a promissory note in the state of Alabama. This agreement allows a lender to take possession of and sell the equipment listed in the agreement in the event that the borrower defaults on their loan payments. The equipment listed serves as collateral for the loan, giving the lender a right to reclaim their investment. The purpose of this agreement is to protect the lender's interest and provide assurance that they will be repaid in case the borrower fails to meet their obligations. By securing the promissory note with equipment, the lender gains a sense of security and reduces the risk associated with lending money. Some common types of Alabama Security Agreement in Equipment for Business Purposes — Securing Promissory Note include: 1. Conditional Sales Agreement: In this type of agreement, the lender retains the ownership of the equipment until the borrower pays off the entire loan amount. The borrower can use the equipment, but the ownership rights remain with the lender until the loan is fully repaid. 2. Chattel Mortgage: This type of agreement allows the lender to hold a lien on the equipment, giving them the right to repossess and sell the equipment if the borrower defaults on the loan. Once the loan is paid off, the lender releases the mortgage, transferring full ownership to the borrower. 3. Equipment Lease Agreement: A lease agreement allows the borrower to rent or lease the equipment from the lender for a specified period. The lender retains ownership and security interest in the equipment until the lease term ends or the borrower exercises an option to purchase the equipment. The Alabama Security Agreement in Equipment for Business Purposes — Securing Promissory Note is a critical document for lenders and borrowers engaging in business transactions involving equipment purchases. It ensures that both parties are protected, providing legal recourse in case of financial difficulties or default. Seeking legal advice is recommended to draft a comprehensive and enforceable agreement that suits the specific needs and circumstances of the parties involved.