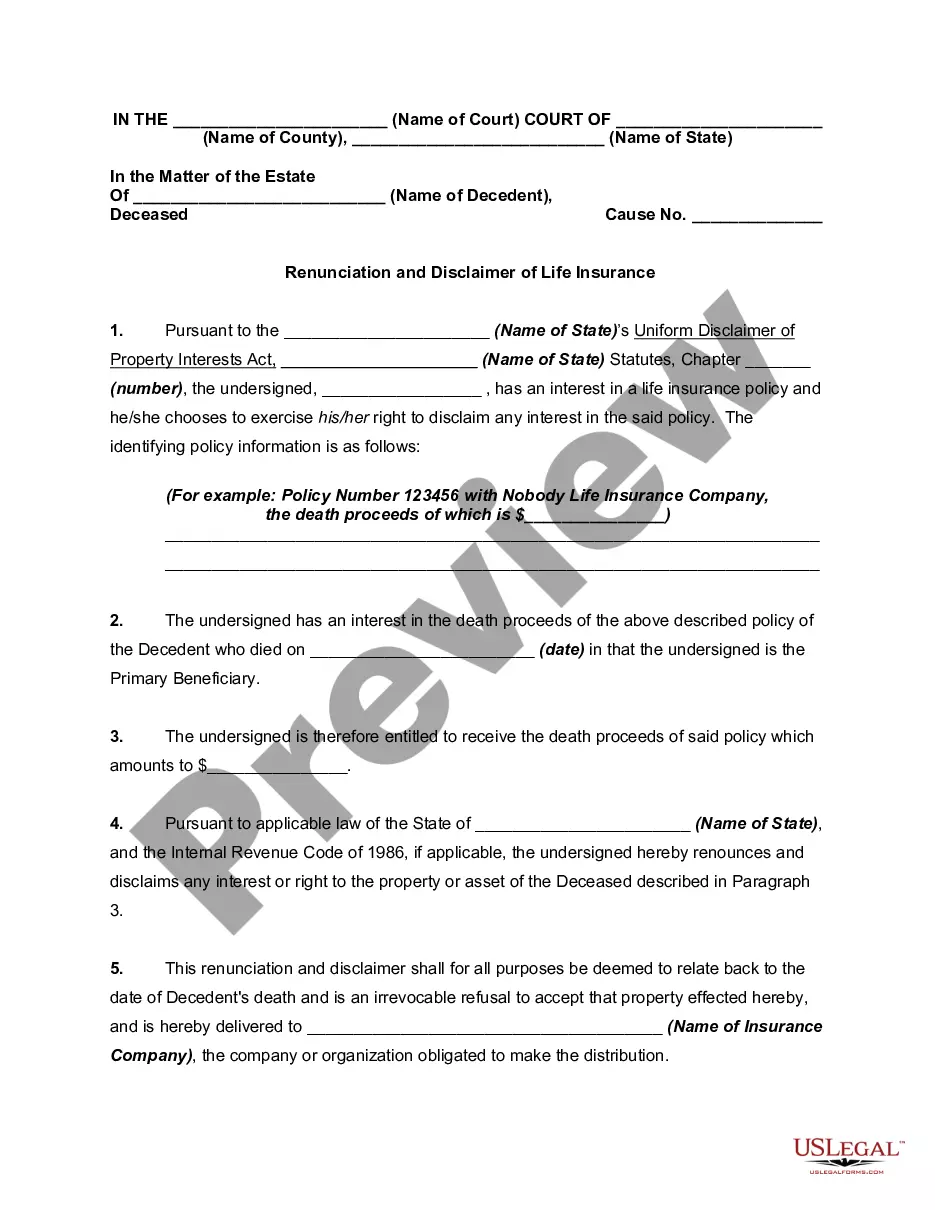

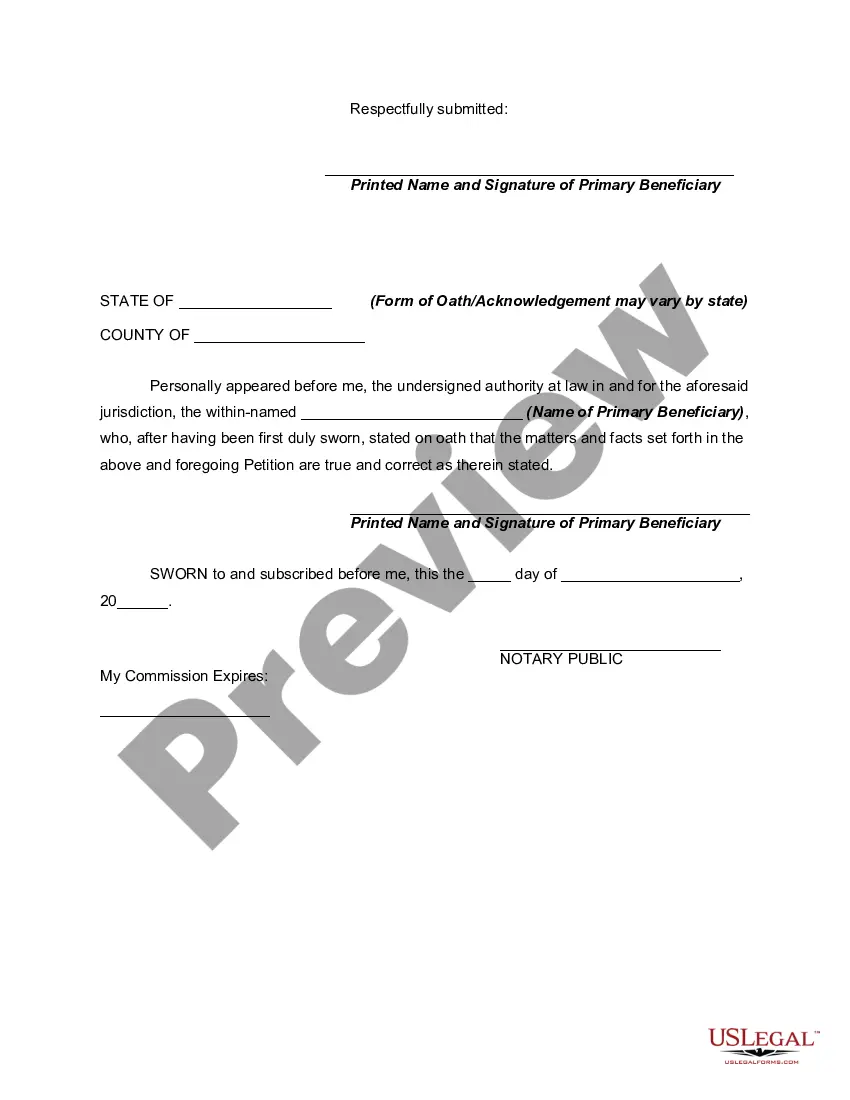

Disclaimers are used by those who receive property as heirs or legatees in an estate, or by beneficiaries of a non-testamentary transfer of property at death; for example, the beneficiaries of a life insurance policy. A disclaimer is simply a declaration by the person entitled to property that the interest in that property is disclaimed or renounced. A disclaimer allows the disclaiming heir or beneficiary to disclaim an interest in such a fashion that the right to the property that is disclaimed is treated as if it never existed.

The Uniform Disclaimers of Property Interests Act (which has been adopted by a number of states) provides the authority to make disclaimers, what interests may be disclaimed, the time when disclaimers are effective, and the effect on the distribution of the disclaimed property interests.

Alabama Renunciation and Disclaimer of Interest in Life Insurance Proceeds: Explained In Alabama, a renunciation and disclaimer of interest in life insurance proceeds refers to the legal act of disclaiming or surrendering one's right to receive funds from a life insurance policy. This renunciation typically occurs when a beneficiary has been named in the policy but chooses not to accept or claim the insurance proceeds. Instead of receiving the funds, the beneficiary effectively waives their interest, allowing the proceeds to pass to an alternate beneficiary or to the estate of the deceased policyholder. There are two main types of Alabama Renunciation and Disclaimer of Interest in Life Insurance Proceeds: 1. Voluntary Renunciation: This occurs when the named beneficiary voluntarily decides not to receive the life insurance proceeds. Reasons for this can vary, including financial considerations, the beneficiary's preference to avoid potential tax liabilities, or if there is a more suitable candidate for receiving the funding. 2. Involuntary Renunciation: This type of renunciation happens when the named beneficiary is legally unable to accept the life insurance proceeds. For instance, if the beneficiary has predeceased the policyholder, or is deemed legally incompetent or incapacitated, they are then unable to claim the proceeds. In this case, the designation of a contingent or secondary beneficiary becomes crucial. The Alabama Renunciation and Disclaimer of Interest in Life Insurance Proceeds is a formal process that involves a written disclaimer statement by the beneficiary. It must meet specific requirements to be legally valid, including a clear and explicit intent to renounce or disclaim the interest in the life insurance proceeds, identification of the insurance policy, and a formal acknowledgment of understanding the consequences of the renunciation. By renouncing their interest in the life insurance proceeds, the beneficiary essentially steps aside, allowing the funds to pass to the next eligible party, whether it be an alternate beneficiary or the deceased's estate. It is essential to consult with an attorney or seek professional legal advice when considering or initiating this process, as it affects the distribution of valuable assets. In conclusion, the Alabama Renunciation and Disclaimer of Interest in Life Insurance Proceeds is a formal legal act that allows a beneficiary to surrender their right to receive funds from a life insurance policy. Whether voluntary or involuntary, this process ensures the smooth transfer of assets to the intended recipients and helps navigate complex estate planning matters.Alabama Renunciation and Disclaimer of Interest in Life Insurance Proceeds: Explained In Alabama, a renunciation and disclaimer of interest in life insurance proceeds refers to the legal act of disclaiming or surrendering one's right to receive funds from a life insurance policy. This renunciation typically occurs when a beneficiary has been named in the policy but chooses not to accept or claim the insurance proceeds. Instead of receiving the funds, the beneficiary effectively waives their interest, allowing the proceeds to pass to an alternate beneficiary or to the estate of the deceased policyholder. There are two main types of Alabama Renunciation and Disclaimer of Interest in Life Insurance Proceeds: 1. Voluntary Renunciation: This occurs when the named beneficiary voluntarily decides not to receive the life insurance proceeds. Reasons for this can vary, including financial considerations, the beneficiary's preference to avoid potential tax liabilities, or if there is a more suitable candidate for receiving the funding. 2. Involuntary Renunciation: This type of renunciation happens when the named beneficiary is legally unable to accept the life insurance proceeds. For instance, if the beneficiary has predeceased the policyholder, or is deemed legally incompetent or incapacitated, they are then unable to claim the proceeds. In this case, the designation of a contingent or secondary beneficiary becomes crucial. The Alabama Renunciation and Disclaimer of Interest in Life Insurance Proceeds is a formal process that involves a written disclaimer statement by the beneficiary. It must meet specific requirements to be legally valid, including a clear and explicit intent to renounce or disclaim the interest in the life insurance proceeds, identification of the insurance policy, and a formal acknowledgment of understanding the consequences of the renunciation. By renouncing their interest in the life insurance proceeds, the beneficiary essentially steps aside, allowing the funds to pass to the next eligible party, whether it be an alternate beneficiary or the deceased's estate. It is essential to consult with an attorney or seek professional legal advice when considering or initiating this process, as it affects the distribution of valuable assets. In conclusion, the Alabama Renunciation and Disclaimer of Interest in Life Insurance Proceeds is a formal legal act that allows a beneficiary to surrender their right to receive funds from a life insurance policy. Whether voluntary or involuntary, this process ensures the smooth transfer of assets to the intended recipients and helps navigate complex estate planning matters.