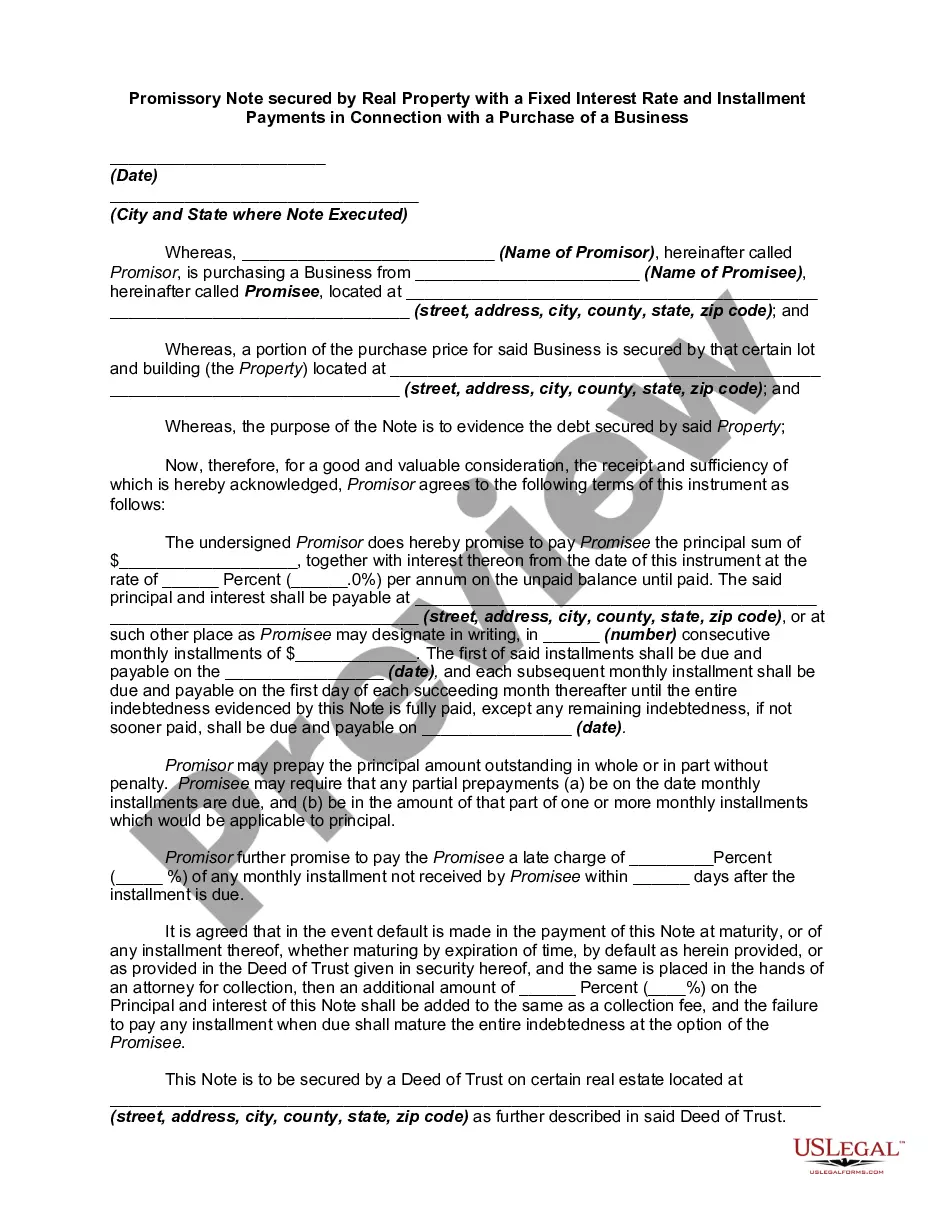

A promissory note is a written promise to pay a debt. An unconditional promise to pay on demand or at a fixed or determined future time a particular sum of money to or to the order of a specified person A promissory note should have several essential elements, including the amount of the loan, the date by which it is to be paid back, the interest rate, and a record of any collateral that is being used to secure the loan. Default terms (what happens if a payment is missed or the loan is not paid off by its due date) should also be spelled out in the promissory note.

In the state of Alabama, a promissory note secured by real property with a fixed interest rate and installment payments is a legally binding agreement used in connection with the purchase of a business. This type of promissory note offers clarity and security for both parties involved in the transaction. By utilizing real property as collateral, the lender ensures protection in case of default, while the borrower benefits from a fixed interest rate and manageable monthly installment payments. The Alabama Promissory Note secured by real property with a fixed interest rate and installment payments for a business purchase can be categorized into several types based on specific terms and conditions: 1. Traditional Fixed-Rate Promissory Note: This type of note involves a fixed interest rate that remains constant throughout the repayment period. This provides stability for both the borrower and the lender, as the interest rate and installment payments will not change over time. 2. Adjustable-Rate Promissory Note: In some cases, the promissory note may have an adjustable interest rate. This rate is typically tied to an index, such as the prime rate, and can fluctuate periodically. The borrower and lender would agree upon an initial interest rate and future adjustments based on the terms set out in the note. 3. Amortization Schedule: The promissory note may outline a specific amortization schedule, which details the repayment structure of the loan. This schedule indicates the principal amount, interest rate, installment payments, and the duration of the repayment period. Understanding the amortization schedule is crucial for both parties, as it helps determine the total cost of the loan and the distribution of principal and interest payments over time. 4. Balloon Payment Option: Some promissory notes may include a balloon payment option. This arrangement allows the borrower to make lower monthly installment payments initially, but a substantial lump sum payment, known as a balloon payment, is due at the end of the loan term. It is important to discuss and negotiate the terms of a balloon payment before entering into the agreement. 5. Prepayment Penalty Clause: A promissory note may include a prepayment penalty clause, which imposes a fee on the borrower for repaying the loan early. This provision safeguards the lender's interest in receiving the agreed-upon interest payments over the loan term. It is essential for the borrower to understand the potential consequences and costs associated with early loan repayment. Overall, an Alabama Promissory Note secured by real property with a fixed interest rate and installment payments in connection with a business purchase provides a structured and legally binding agreement that ensures both the borrower and the lender are protected throughout the transaction. However, it is advisable to consult with legal professionals to ensure compliance with Alabama state laws and to customize the promissory note to meet the specific needs of the business purchase.In the state of Alabama, a promissory note secured by real property with a fixed interest rate and installment payments is a legally binding agreement used in connection with the purchase of a business. This type of promissory note offers clarity and security for both parties involved in the transaction. By utilizing real property as collateral, the lender ensures protection in case of default, while the borrower benefits from a fixed interest rate and manageable monthly installment payments. The Alabama Promissory Note secured by real property with a fixed interest rate and installment payments for a business purchase can be categorized into several types based on specific terms and conditions: 1. Traditional Fixed-Rate Promissory Note: This type of note involves a fixed interest rate that remains constant throughout the repayment period. This provides stability for both the borrower and the lender, as the interest rate and installment payments will not change over time. 2. Adjustable-Rate Promissory Note: In some cases, the promissory note may have an adjustable interest rate. This rate is typically tied to an index, such as the prime rate, and can fluctuate periodically. The borrower and lender would agree upon an initial interest rate and future adjustments based on the terms set out in the note. 3. Amortization Schedule: The promissory note may outline a specific amortization schedule, which details the repayment structure of the loan. This schedule indicates the principal amount, interest rate, installment payments, and the duration of the repayment period. Understanding the amortization schedule is crucial for both parties, as it helps determine the total cost of the loan and the distribution of principal and interest payments over time. 4. Balloon Payment Option: Some promissory notes may include a balloon payment option. This arrangement allows the borrower to make lower monthly installment payments initially, but a substantial lump sum payment, known as a balloon payment, is due at the end of the loan term. It is important to discuss and negotiate the terms of a balloon payment before entering into the agreement. 5. Prepayment Penalty Clause: A promissory note may include a prepayment penalty clause, which imposes a fee on the borrower for repaying the loan early. This provision safeguards the lender's interest in receiving the agreed-upon interest payments over the loan term. It is essential for the borrower to understand the potential consequences and costs associated with early loan repayment. Overall, an Alabama Promissory Note secured by real property with a fixed interest rate and installment payments in connection with a business purchase provides a structured and legally binding agreement that ensures both the borrower and the lender are protected throughout the transaction. However, it is advisable to consult with legal professionals to ensure compliance with Alabama state laws and to customize the promissory note to meet the specific needs of the business purchase.