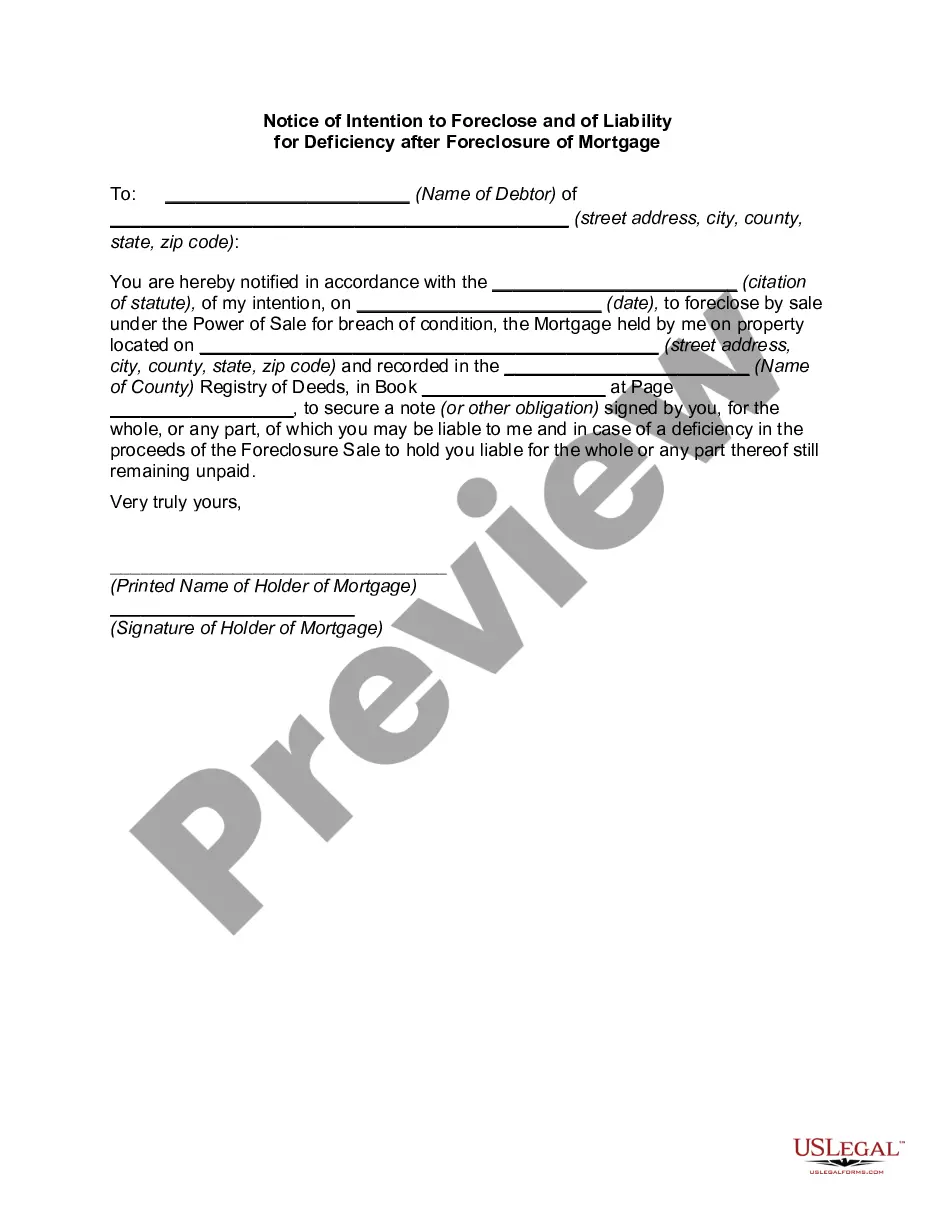

A number of states have enacted measures to facilitate greater communication between borrowers and lenders by requiring mortgage servicers to provide certain notices to defaulted borrowers prior to commencing a foreclosure action. The measures serve a dual purpose, providing more meaningful notice to borrowers of the status of their loans and slowing down the rate of foreclosures within these states. For instance, one state now requires a mortgagee to mail a homeowner a notice of intent to foreclose at least 45 days before initiating a foreclosure action on a loan. The notice must be in writing, and must detail all amounts that are past due and any itemized charges that must be paid to bring the loan current, inform the homeowner that he or she may have options as an alternative to foreclosure, and provide contact information of the servicer, HUD-approved foreclosure counseling agencies, and the state Office of Commissioner of Banks.

Alabama Notice and Demand to Mortgagor regarding Intent to Foreclose

Description

How to fill out Notice And Demand To Mortgagor Regarding Intent To Foreclose?

You might invest numerous hours online trying to locate the valid document template that complies with the state and federal requirements you need.

US Legal Forms provides a plethora of valid forms that have been verified by experts.

You can download or print the Alabama Notice and Demand to Mortgagor regarding Intent to Foreclose from your account.

First, ensure you have selected the correct document template for the area or city of your choice. Review the form description to confirm that you have chosen the appropriate form. If available, utilize the Review option to examine the document template as well. To find another version of the form, use the Look for field to locate the template that fits your needs and requirements. Once you have located the template you want, click Buy now to proceed. Choose the pricing plan you prefer, enter your credentials, and register for an account on US Legal Forms. Complete the transaction using your credit card or PayPal account to pay for the valid form. Select the format of the document and download it to your device. Make modifications to your document if necessary. You can fill out, edit, and sign and print the Alabama Notice and Demand to Mortgagor regarding Intent to Foreclose. Access and print thousands of document templates using the US Legal Forms website, which offers the largest selection of valid forms. Utilize professional and state-specific templates to address your business or personal requirements.

- If you already possess a US Legal Forms account, you may Log In and then select the Obtain option.

- Then, you can fill out, edit, print, or sign the Alabama Notice and Demand to Mortgagor regarding Intent to Foreclose.

- Every valid document template you purchase becomes yours permanently.

- To get another copy of any acquired form, go to the My documents tab and click the relevant option.

- If you are visiting the US Legal Forms site for the first time, follow the simple guidelines below.

Form popularity

FAQ

To stop foreclosure immediately in Alabama, you can take several steps. First, consider contacting your lender to discuss your financial situation and see if they can offer a temporary solution. You can also file for bankruptcy, as it may automatically halt foreclosure actions. Additionally, submitting an Alabama Notice and Demand to Mortgagor regarding Intent to Foreclose may provide a formal way to assert your rights and negotiate a resolution with your lender.

A request for notice of mortgage foreclosure is a formal appeal made by a borrower or interested party to be notified about any foreclosure proceedings. This request ensures that they stay informed throughout the process. Recognizing the significance of the Alabama Notice and Demand to Mortgagor regarding Intent to Foreclose in this context can help protect you from surprises in the foreclosure timeline.

Foreclosure in New Mexico involves a judicial process where the lender must file a lawsuit to obtain a court order for foreclosure. This process can be lengthy and requires specific documentation, including the Alabama Notice and Demand to Mortgagor regarding Intent to Foreclose that establishes the lender’s claims. Knowing this can help homeowners prepare for what lies ahead.

A foreclosure notice is a legal document that notifies a borrower of the lender's intent to reclaim the property due to non-payment. This document usually outlines the total amount owed and the repercussions of failing to address the debt. By understanding the Alabama Notice and Demand to Mortgagor regarding Intent to Foreclose, you can take informed actions to protect your interests.

The notice of intention to foreclose is a formal statement indicating the lender's plan to initiate foreclosure proceedings against a property. It typically details the reasons and timelines involved in the process. Familiarizing yourself with the Alabama Notice and Demand to Mortgagor regarding Intent to Foreclose can help clarify your rights and responsibilities at this stage.

Responding to a foreclosure notice involves understanding the contents of the notice and acting quickly. You may choose to contact the lender to discuss possible repayment options or negotiate alternative solutions. Utilizing resources like the Alabama Notice and Demand to Mortgagor regarding Intent to Foreclose and platforms such as USLegalForms can provide clear guidance during this critical process.

A letter of intent to foreclosure formally informs the property owner of the lender's desire to initiate foreclosure proceedings. This document usually outlines the reasons for the impending action and any missed payments. Understanding the Alabama Notice and Demand to Mortgagor regarding Intent to Foreclose can help you respond appropriately and know your options moving forward.

In real estate, a letter of intent serves as a preliminary agreement between parties aiming to enter into a formal contract. This document outlines the key terms and conditions, including any contingencies that may apply. When it comes to the Alabama Notice and Demand to Mortgagor regarding Intent to Foreclose, such letters help clarify the lender's position and the expectations placed on the borrower. This clarity is vital for making informed decisions in real estate transactions.

A letter of intent for foreclosure is a formal document sent by a lender to inform the borrower of their intention to initiate foreclosure proceedings. This letter typically outlines the reasons for the impending action and the specific amount owed on the mortgage. Understanding the Alabama Notice and Demand to Mortgagor regarding Intent to Foreclose is crucial, as it contains essential information that may help the borrower take appropriate action. It's important to seek assistance in responding to this letter promptly.