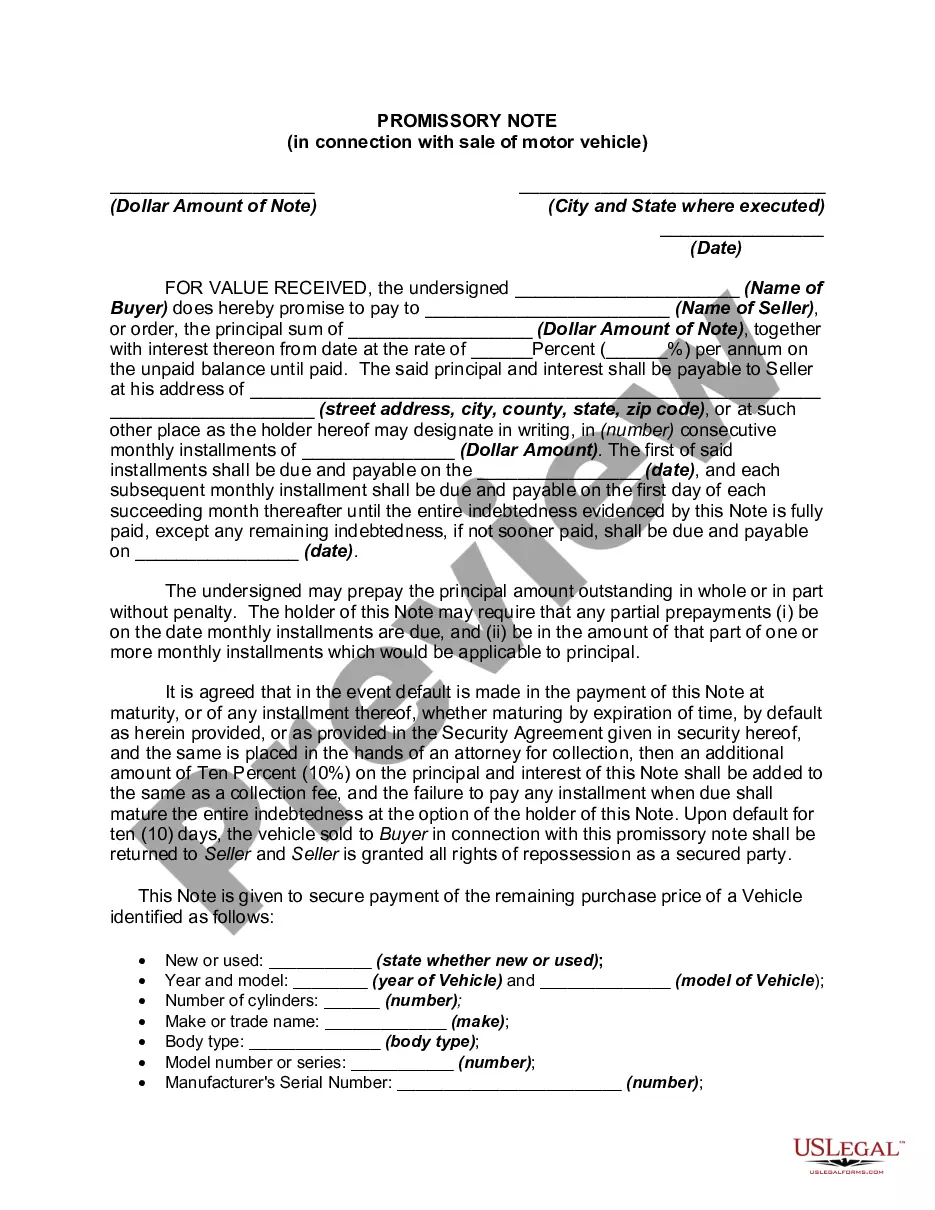

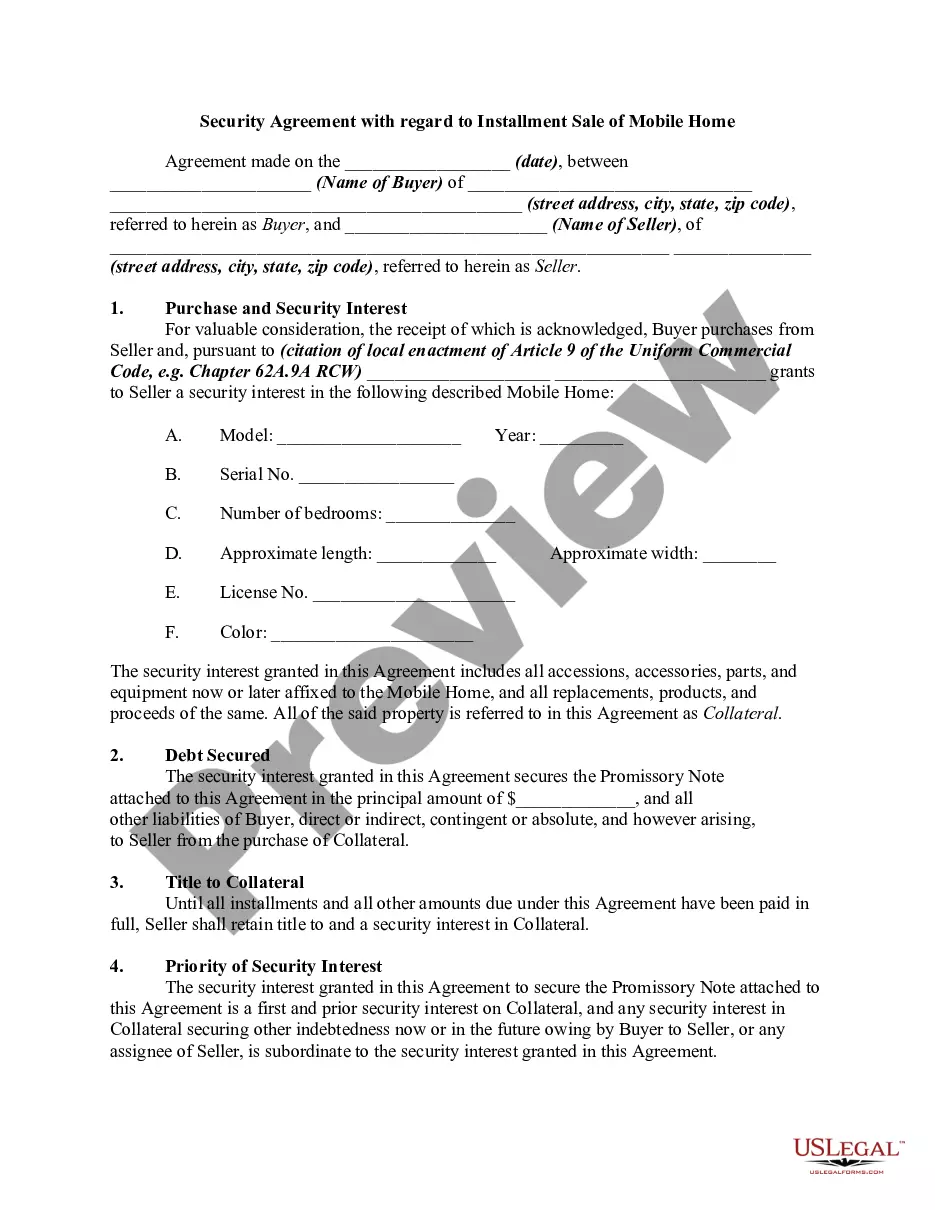

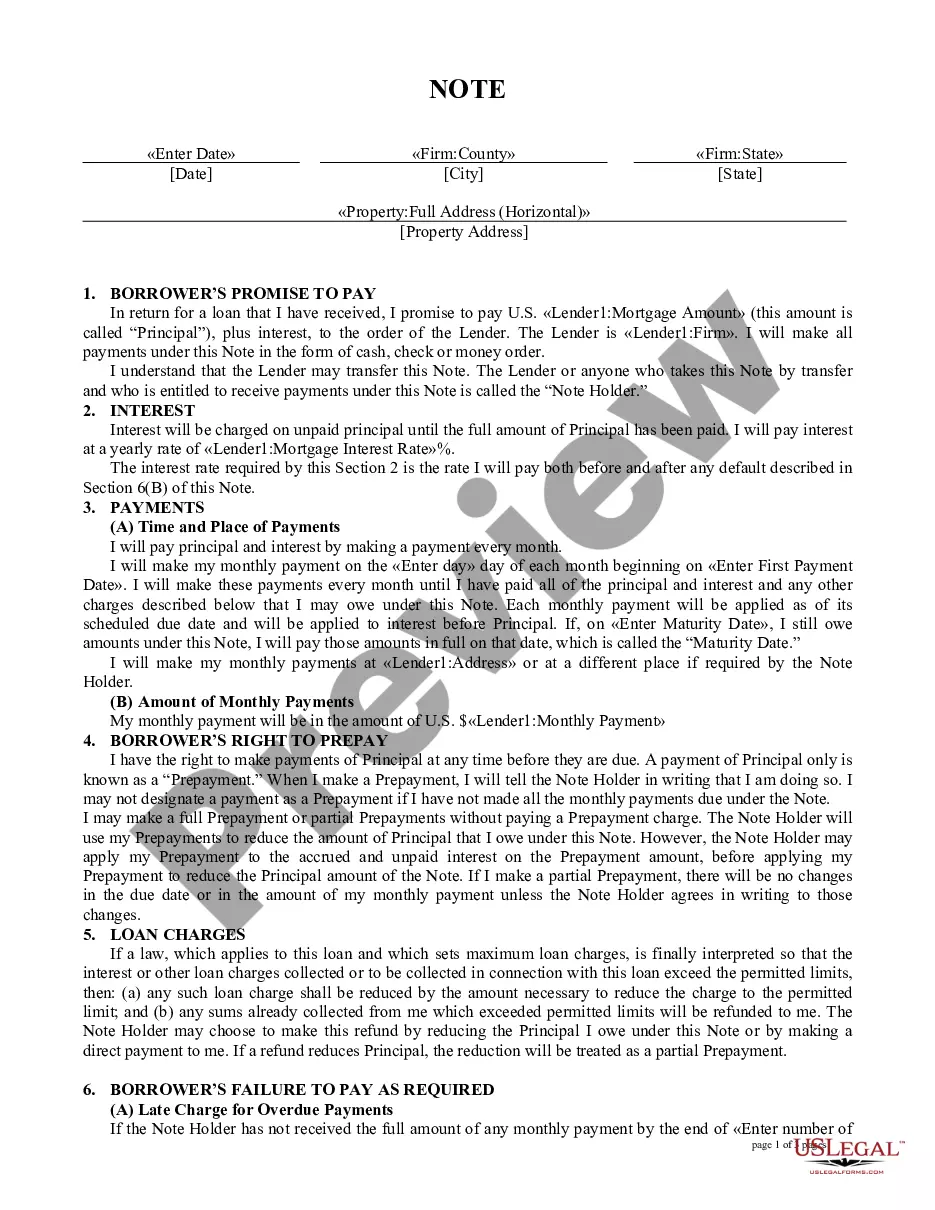

Alabama Promissory Note in Connection with a Sale and Purchase of a Mobile Home

Description

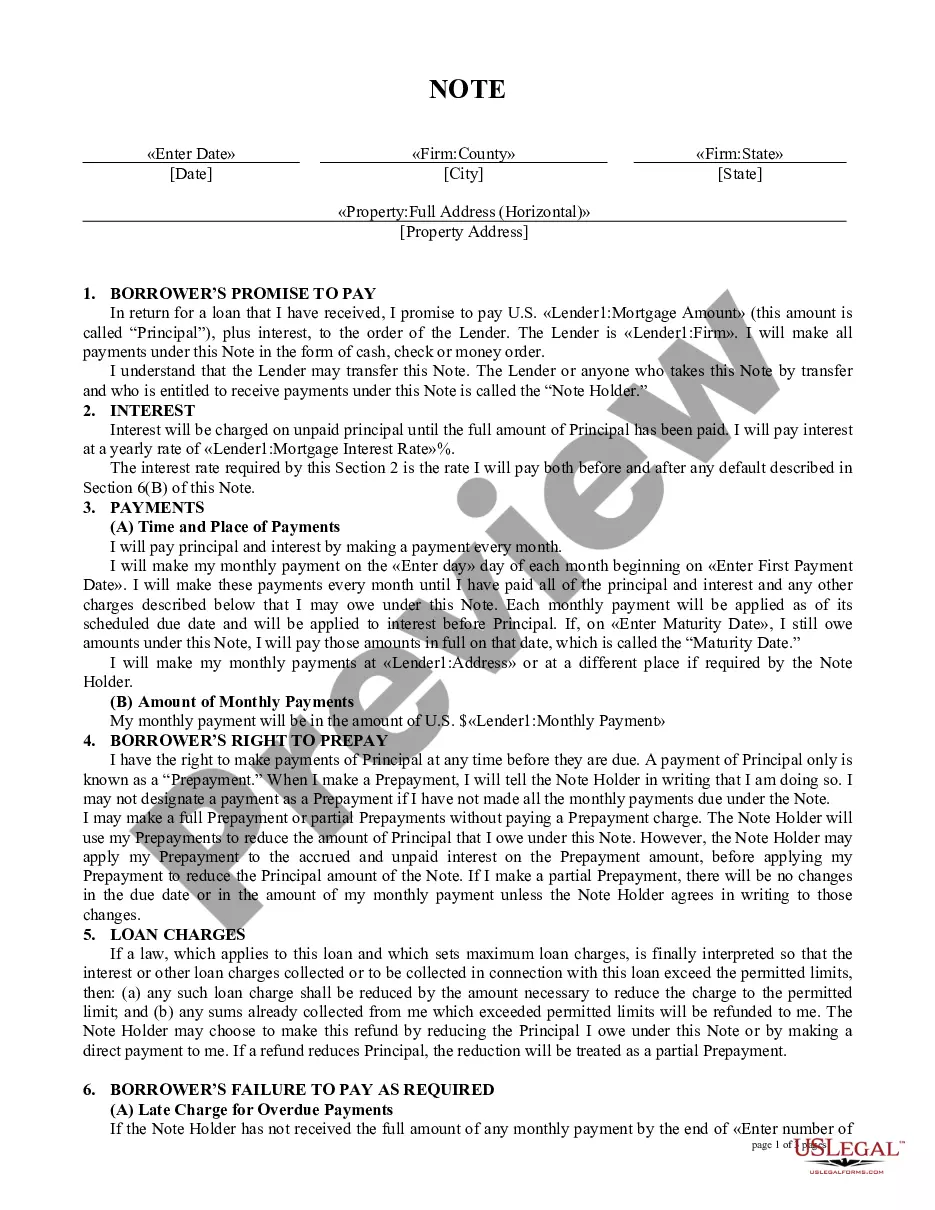

How to fill out Promissory Note In Connection With A Sale And Purchase Of A Mobile Home?

Are you in a location where you require documents for either business or personal reasons almost every day.

There are numerous legal document templates available online, but finding trustworthy ones can be challenging.

US Legal Forms offers a vast array of form templates, such as the Alabama Promissory Note for the Sale and Purchase of a Mobile Home, designed to fulfill federal and state requirements.

When you find the right form, simply click Purchase now.

Select the pricing plan you prefer, enter the required information to create your account, and complete the purchase using your PayPal or credit card.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- After that, you can download the Alabama Promissory Note for the Sale and Purchase of a Mobile Home template.

- If you do not have an account and want to start using US Legal Forms, follow these steps.

- Obtain the form you need and ensure it is for the correct area/county.

- Utilize the Review option to examine the form.

- Read the description to ensure you have selected the correct form.

- If the form is not what you're looking for, use the Search field to find the document that meets your needs.

Form popularity

FAQ

Examples of promissory notes can include home loans, personal loans, or loans for purchasing vehicles and mobile homes. Each type outlines the terms of repayment and can vary in complexity. Resources on uslegalforms provide real-world samples that can guide you in creating your own note.

A promissory note typically formats essential sections such as the title, parties' names, principal amount, interest rate, payment terms, and signatures. The layout should be clear and structured to ensure understanding for all parties involved. Using a streamlined template from uslegalforms can assist in getting it right.

In Alabama, a promissory note does not require notarization to be valid. However, having it notarized can provide an extra layer of security for both the borrower and the lender. It ensures that the signatures are authentic, which can be particularly useful in disputes.

A promissory note is not the same as a contract. A contract details all the terms of a legal agreement. A promissory note covers only the following: The date by when someone needs to be paid.

A Promissory note is a contract, which means that it is legally binding. However, it must include certain conditions to ensure it is enforceable.

Information to include in a mobile home bill of sale.Mobile home description, including VIN, serial number, make, model, and year.Buyer and seller names, addresses and contact information.Sale date.Sale price, including any taxes.Sale conditions and terms, including warranties or as is status.

Texas Mobile Home PaperworkSale, transfer and current ownership of a manufactured home.Whether a home is titled as personal or real property.The home's physical location.Outstanding liens.

To move a manufactured home, the state requires the owner to get a permit from the Department of Motor Vehicles (DMV). They must submit a copy of this permit when they apply for a new Statement of Ownership, showing the new location of the home.

In many ways, a promissory note functions as a kind of IOU document, although in practice it is more complex. However, it is also much more informal than a loan agreement and does not legally bind the lender in the same way, although the borrower is still bound to the promissory note.

A promissory note is a written agreement to pay someone essentially an IOU. But it's not something to be taken lightly. "It is a legally binding written document effectuating a promise to repay money," says Andrea Wheeler, a business attorney and owner of Wheeler Legal PLLC of Florida.