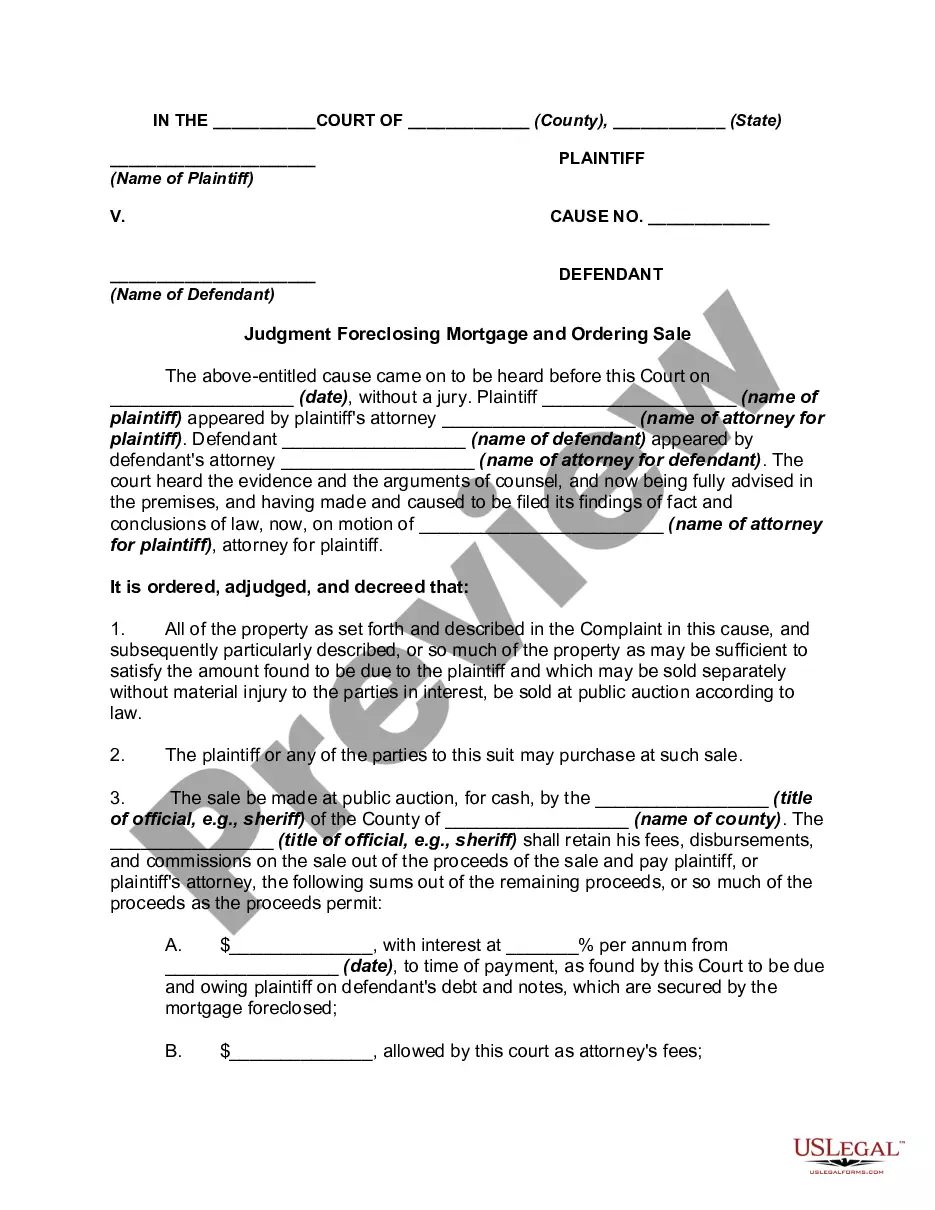

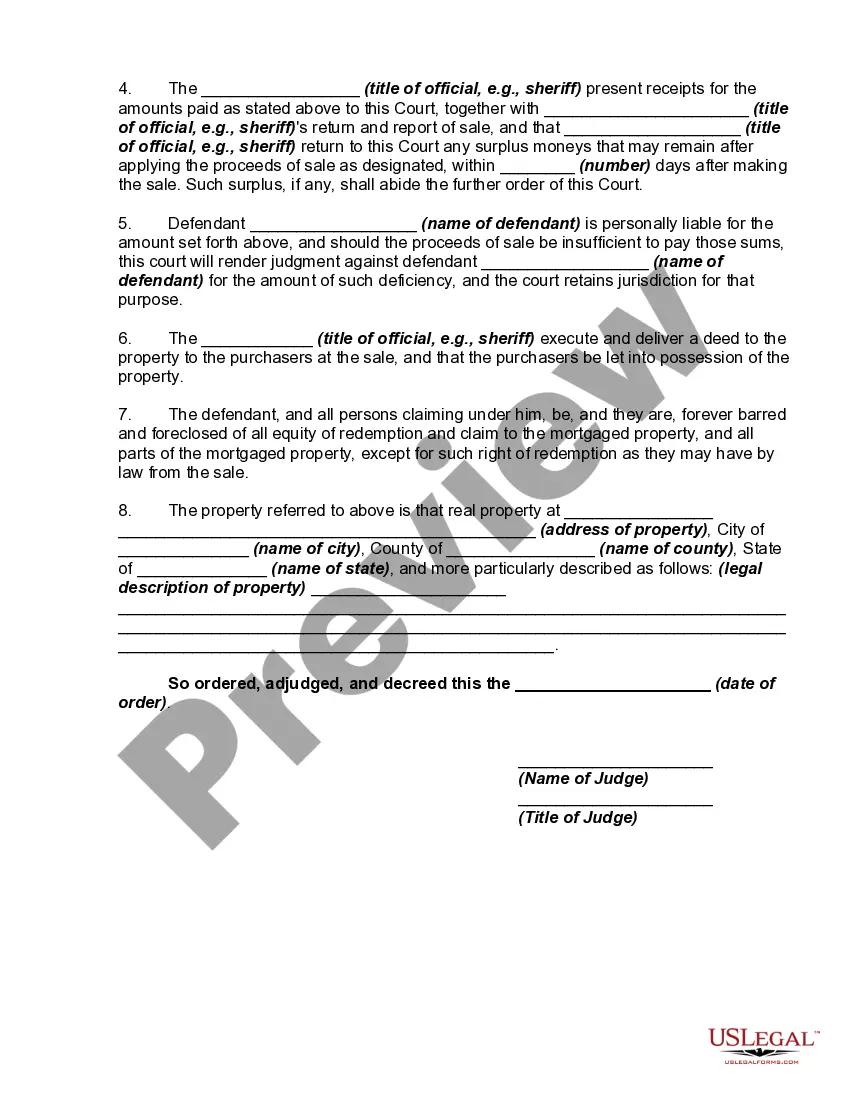

Title: Understanding Alabama Judgement Foreclosing Mortgage and Ordering Sale Introduction: When it comes to mortgage foreclosures in Alabama, a Judgment Foreclosing Mortgage and Ordering Sale is a legal process that involves the lender seeking to foreclose on a property due to the borrower's inability to make mortgage payments. This detailed description aims to provide essential information about the Alabama Judgment Foreclosing Mortgage and Ordering Sale process, its significance, and any relevant variations within this legal framework. Keywords: Alabama, judgement, foreclosing mortgage, ordering sale, legal process, lender, borrower, property, mortgage payments, variations. 1. Overview of Alabama Judgment Foreclosing Mortgage and Ordering Sale: In Alabama, when a borrower fails to meet their mortgage payment obligations, the lender has the right to initiate a foreclosure proceeding. This process is typically executed through a Judgment Foreclosing Mortgage and Ordering Sale, commonly known as a foreclosure judgement. 2. Role of the Court in Foreclosure Proceedings: The court plays a vital role in the Alabama Judgment Foreclosing Mortgage and Ordering Sale process. When a lender files a foreclosure lawsuit, the court reviews the case to ensure compliance with all legal requirements. If the court finds the lender's claim valid, it will grant a Judgment Foreclosing Mortgage and Ordering Sale, enabling the lender to sell the property at a public auction. 3. Legal Notice Requirements for Alabama Judgment Foreclosing Mortgage and Ordering Sale: Before initiating a foreclosure auction, the lender must provide the borrower with a legal notice, known as a notice of intent to foreclose. This notice must comply with Alabama state laws regarding timing, content, and delivery methods to ensure the borrower receives adequate notification. 4. Calculation of Debt Owed: Once a Judgment Foreclosing Mortgage and Ordering Sale is granted, the court determines the outstanding debt owed by the borrower. This amount usually includes the unpaid principal, interest, legal fees, and any additional costs related to the foreclosure process. 5. Foreclosure Auction Process: The Judgment Foreclosing Mortgage and Ordering Sale authorizes the lender to proceed with a public auction of the foreclosed property. This auction is typically overseen by the court or a designated representative. The highest bidder at the auction becomes the new owner of the property, subject to any redemption rights or applicable laws. 6. Redemption Period and Deficiency Judgements: In Alabama, the foreclosure process may include a redemption period allowing the borrower to redeem the property by paying off the outstanding debt. If the borrower fails to redeem the property within the redemption period, the court may issue a deficiency judgement, holding the borrower responsible for any remaining debt. Types of Alabama Judgment Foreclosing Mortgage and Ordering Sale: — Standard Foreclosure: The traditional type of foreclosure process, involving a lender initiating proceedings against a borrower for non-payment of mortgage obligations. — Judicial Foreclosure: A foreclosure process conducted through the court system, where a Judgment Foreclosing Mortgage and Ordering Sale is issued to allow the lender to sell the property. — Non-Judicial Foreclosure: In cases where the mortgage contains a "power of sale" clause, the lender can foreclose on the property without going through a court-supervised process. Conclusion: Alabama Judgment Foreclosing Mortgage and Ordering Sale is a legal process wherein a lender seeks to foreclose on a property and sell it at auction due to the borrower's default on mortgage payments. Understanding the specifics of this process, including notice requirements, auction procedures, and potential variations such as standard, judicial, or non-judicial foreclosure, is crucial for both borrowers and lenders involved in Alabama's real estate market.

Alabama Judgment Foreclosing Mortgage and Ordering Sale

Description

How to fill out Alabama Judgment Foreclosing Mortgage And Ordering Sale?

Are you inside a position where you will need papers for both organization or specific functions virtually every day? There are a lot of authorized papers web templates accessible on the Internet, but finding ones you can depend on isn`t simple. US Legal Forms gives 1000s of kind web templates, just like the Alabama Judgment Foreclosing Mortgage and Ordering Sale , which can be written to satisfy state and federal demands.

When you are presently acquainted with US Legal Forms website and have an account, merely log in. Afterward, you may obtain the Alabama Judgment Foreclosing Mortgage and Ordering Sale format.

Should you not have an accounts and want to begin using US Legal Forms, adopt these measures:

- Find the kind you will need and ensure it is for your appropriate metropolis/region.

- Utilize the Preview switch to review the form.

- Browse the description to actually have selected the appropriate kind.

- If the kind isn`t what you`re looking for, use the Look for industry to get the kind that meets your requirements and demands.

- When you get the appropriate kind, click Get now.

- Select the rates program you need, fill out the necessary information and facts to generate your bank account, and buy the transaction making use of your PayPal or Visa or Mastercard.

- Choose a handy data file file format and obtain your version.

Locate all of the papers web templates you have purchased in the My Forms food selection. You can obtain a extra version of Alabama Judgment Foreclosing Mortgage and Ordering Sale anytime, if possible. Just go through the required kind to obtain or produce the papers format.

Use US Legal Forms, by far the most extensive selection of authorized types, to save lots of efforts and prevent faults. The services gives professionally manufactured authorized papers web templates which you can use for a variety of functions. Make an account on US Legal Forms and commence making your life a little easier.