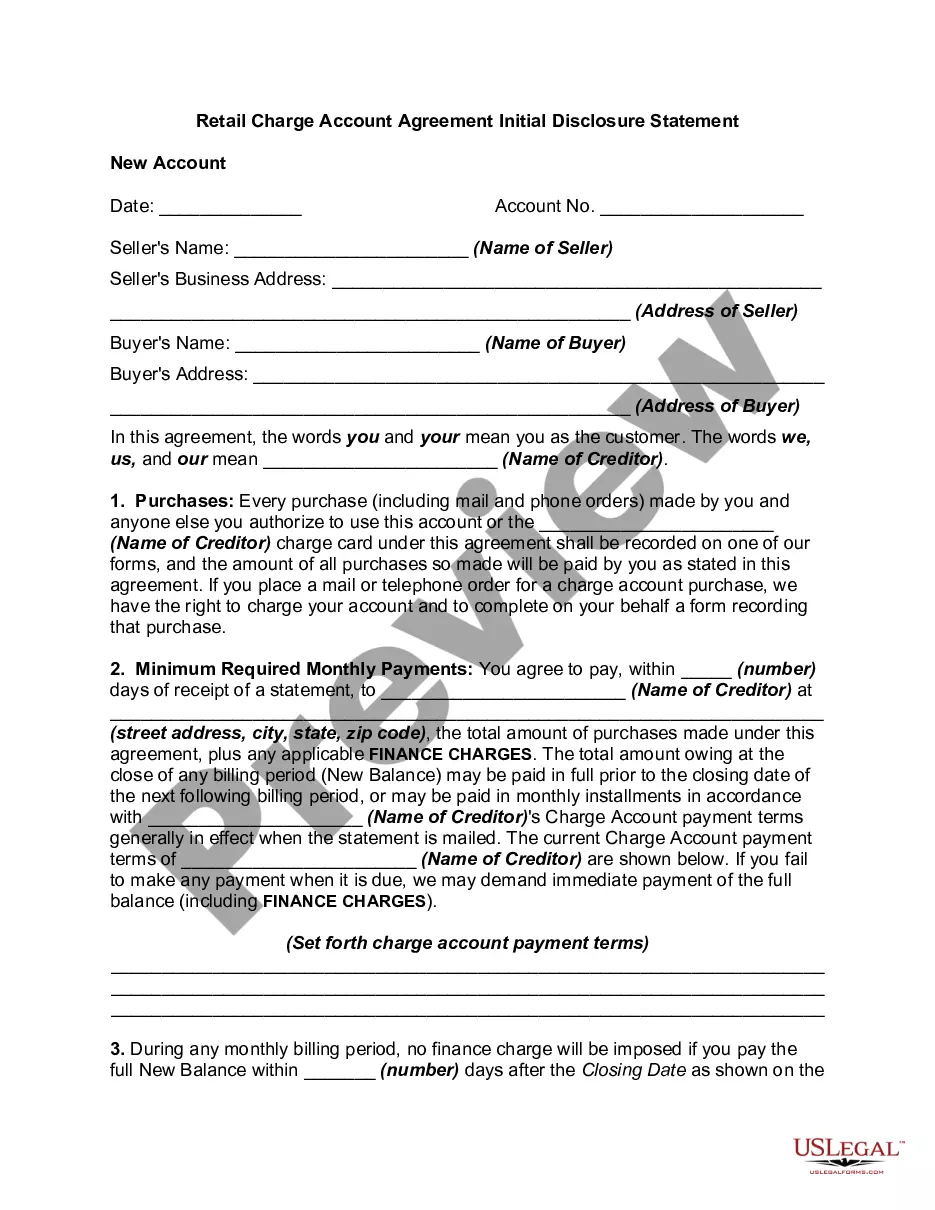

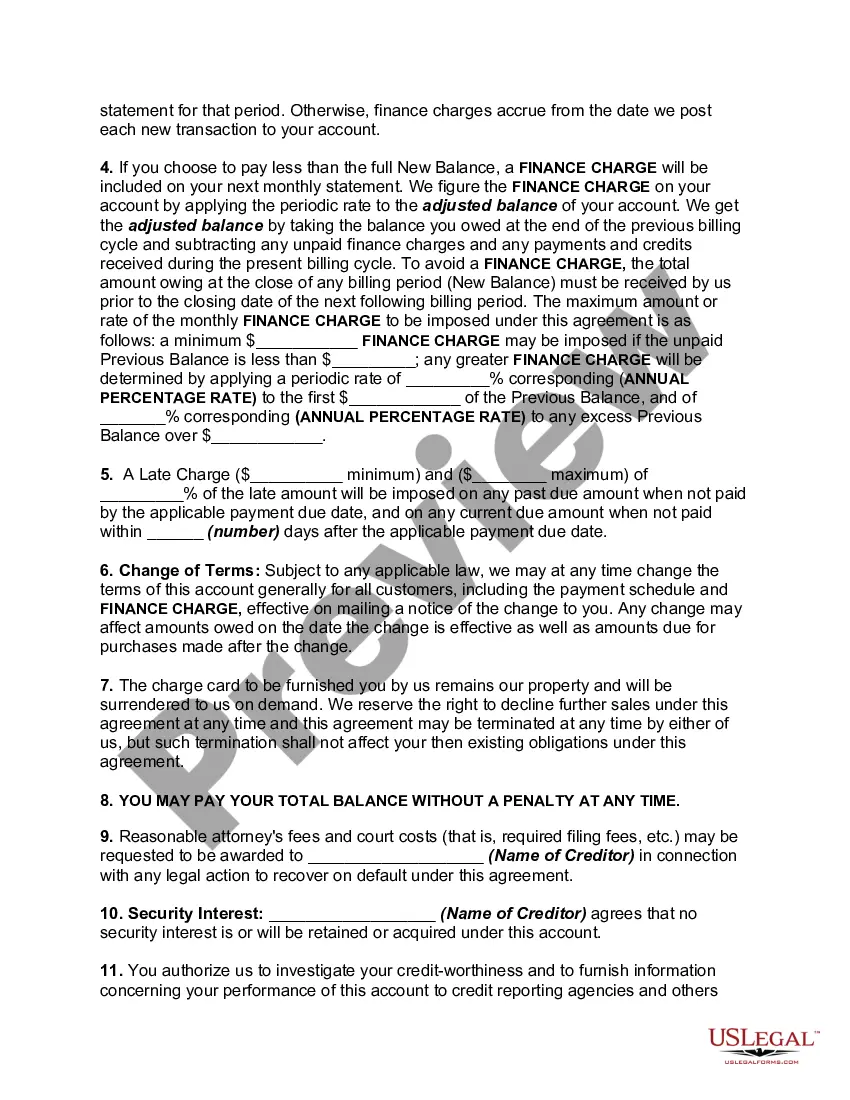

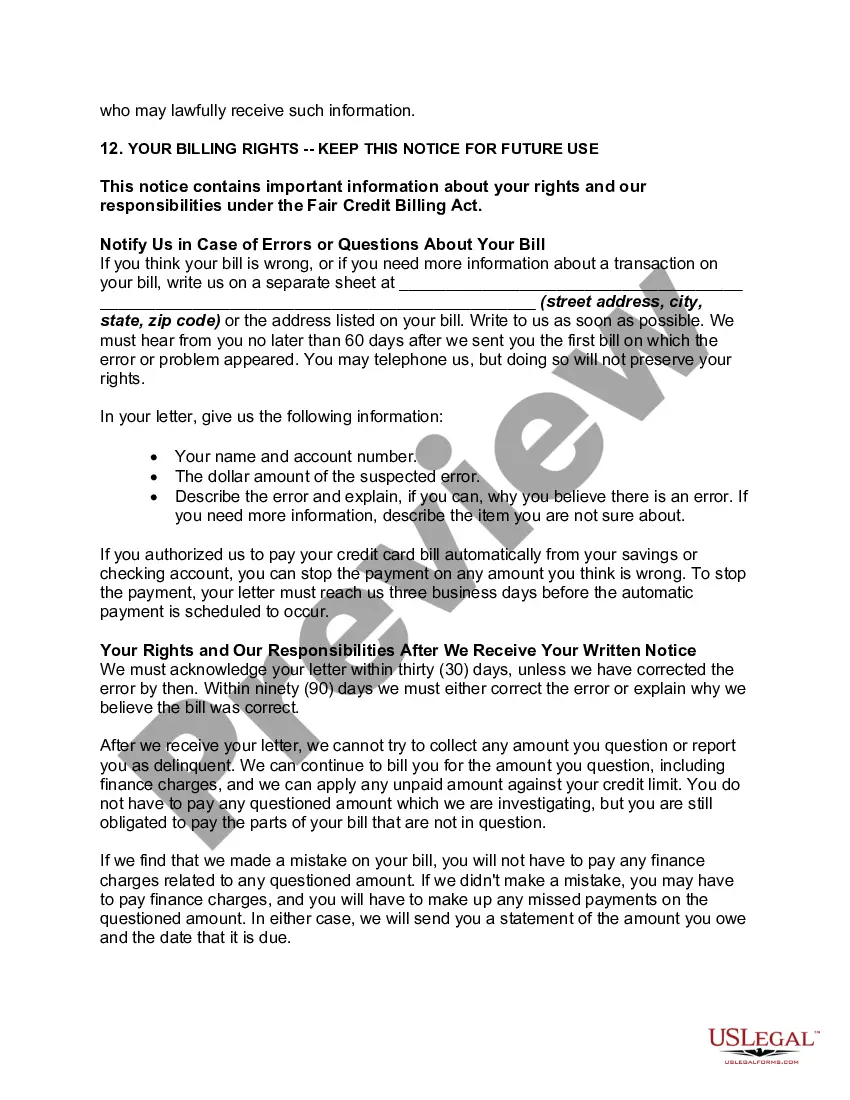

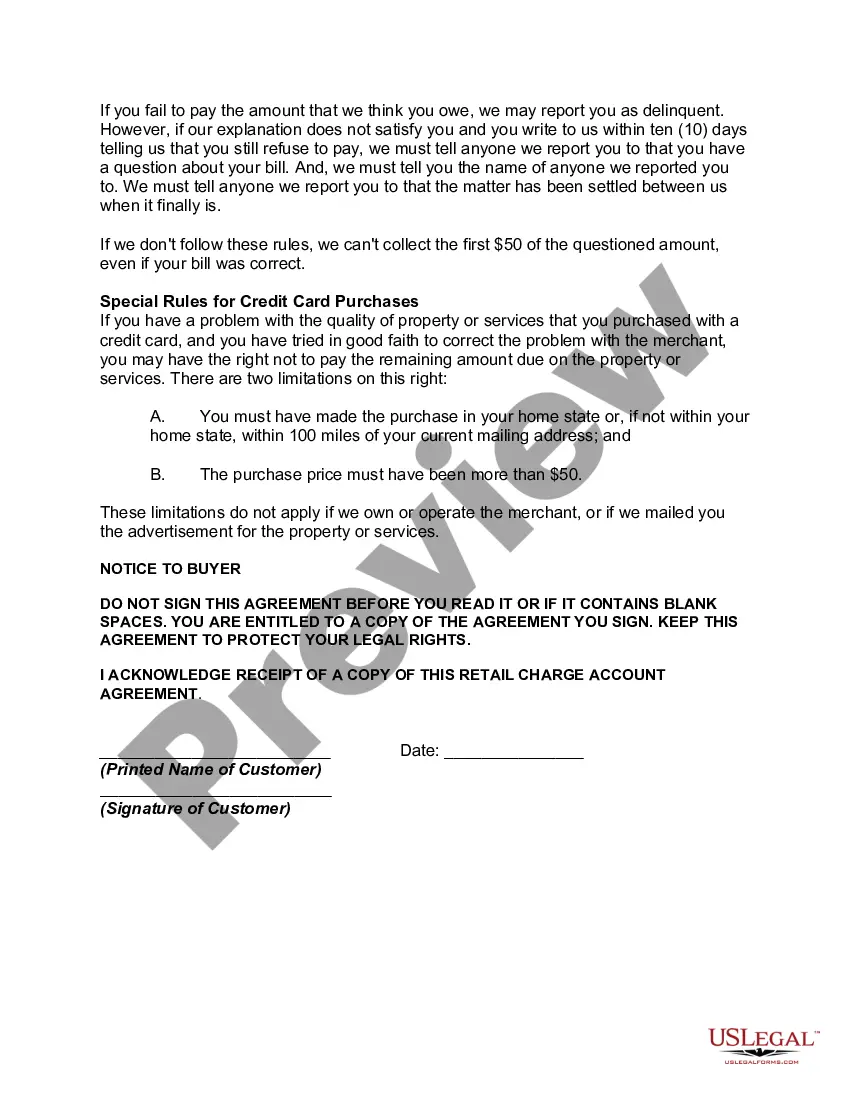

The Alabama Retail Charge Account Agreement Initial Disclosure Statement is a comprehensive document that outlines the terms and conditions associated with retail charge accounts in the state of Alabama. This disclosure statement is crucial for both retailers and consumers, as it clearly defines the rights, responsibilities, and obligations of all parties involved in these credit transactions. The Alabama Retail Charge Account Agreement Initial Disclosure Statement covers a wide range of important details, including the billing and payment terms, interest rates, fees, and penalties associated with retail charge accounts. It also highlights the consumer's rights under the federal law, such as the Truth in Lending Act (TILL) and the Fair Credit Reporting Act (FCRA), ensuring compliance with these regulations. In addition, this disclosure statement emphasizes the importance of maintaining accurate and up-to-date information about the consumer's credit profile. It addresses how the retailer will use and safeguard the consumer's personal and financial information, as well as the consumer's rights to dispute billing errors and obtain credit report disclosures. Different types of Alabama Retail Charge Account Agreement Initial Disclosure Statements may exist depending on the specific retailer or financial institution offering the retail charge account. Each retailer or financial institution may have its own unique terms and conditions, interest rates, fees, and penalties. Therefore, it is crucial for consumers to carefully review and understand the terms outlined in the disclosure statement provided by the retailer or financial institution before entering into a retail charge account agreement. Ultimately, the Alabama Retail Charge Account Agreement Initial Disclosure Statement serves as a vital tool for promoting transparency, fairness, and accountability in retail charge account transactions within the state. By clearly defining the rights and responsibilities of both retailers and consumers, it ensures a smooth and mutually beneficial credit relationship while protecting the consumer's interests and complying with relevant laws and regulations.

Alabama Retail Charge Account Agreement Initial Disclosure Statement

Description

How to fill out Alabama Retail Charge Account Agreement Initial Disclosure Statement?

Discovering the right legitimate file design could be a struggle. Needless to say, there are plenty of layouts available on the net, but how would you discover the legitimate develop you need? Utilize the US Legal Forms web site. The assistance delivers 1000s of layouts, for example the Alabama Retail Charge Account Agreement Initial Disclosure Statement, that you can use for enterprise and private demands. All of the varieties are examined by experts and meet up with state and federal demands.

When you are already signed up, log in for your account and then click the Acquire option to have the Alabama Retail Charge Account Agreement Initial Disclosure Statement. Utilize your account to appear throughout the legitimate varieties you have acquired in the past. Proceed to the My Forms tab of your own account and have an additional backup in the file you need.

When you are a whole new customer of US Legal Forms, allow me to share basic guidelines so that you can adhere to:

- Initial, make sure you have selected the appropriate develop to your town/region. You can look through the shape making use of the Preview option and browse the shape explanation to guarantee it will be the best for you.

- In the event the develop will not meet up with your expectations, utilize the Seach industry to get the right develop.

- Once you are sure that the shape is proper, click the Acquire now option to have the develop.

- Choose the prices strategy you desire and enter the needed information. Make your account and pay for the order with your PayPal account or Visa or Mastercard.

- Opt for the data file structure and obtain the legitimate file design for your system.

- Total, edit and printing and indication the attained Alabama Retail Charge Account Agreement Initial Disclosure Statement.

US Legal Forms will be the biggest catalogue of legitimate varieties where you can see numerous file layouts. Utilize the company to obtain expertly-produced paperwork that adhere to condition demands.