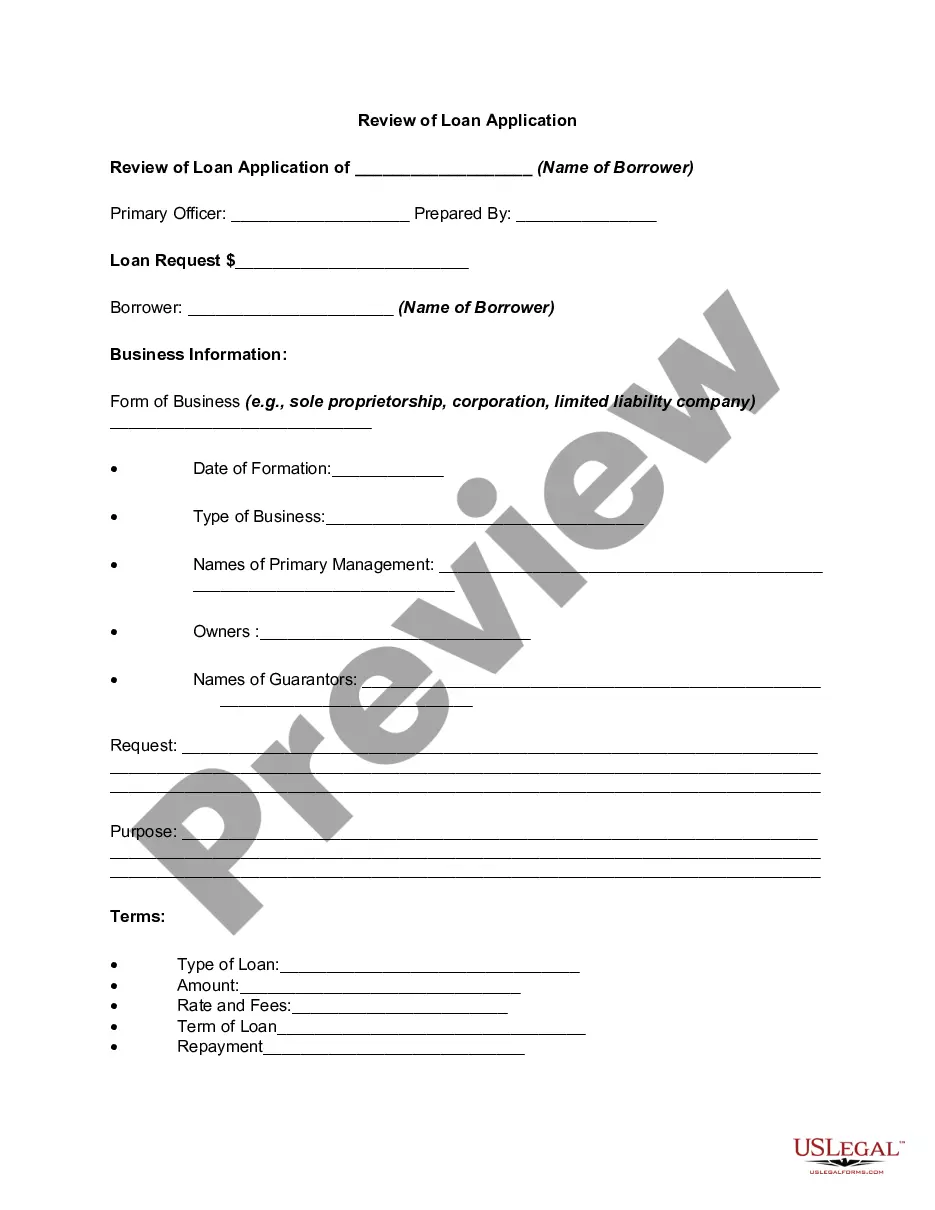

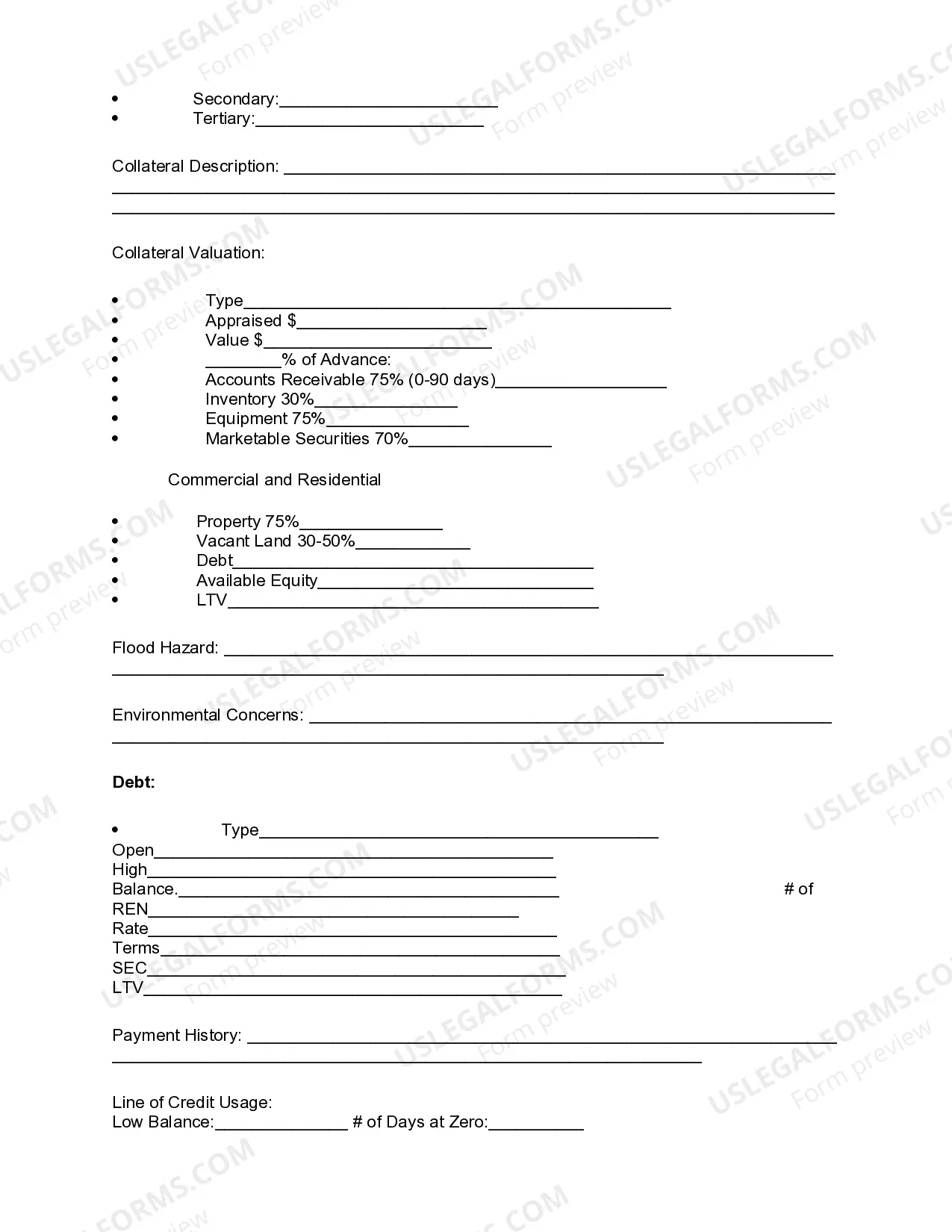

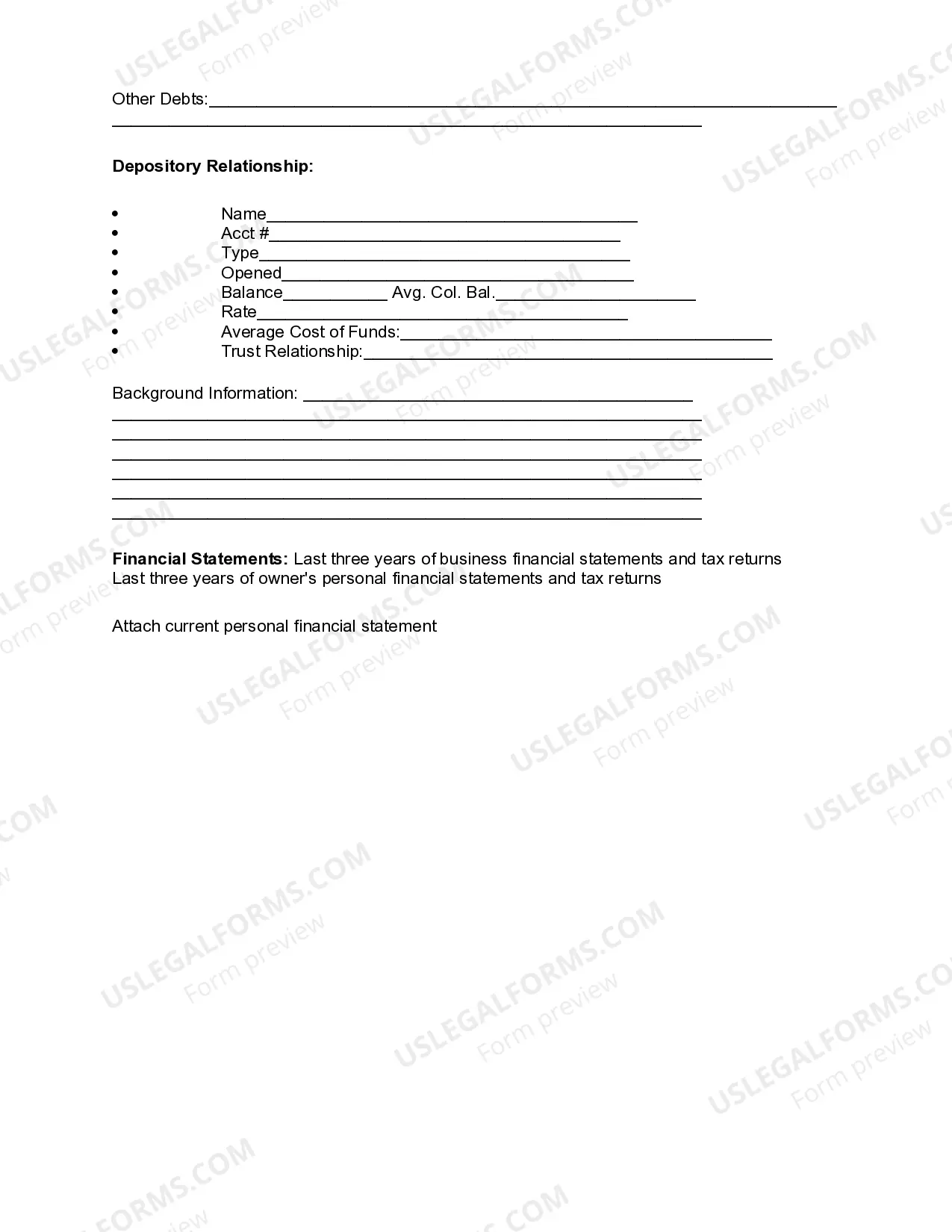

Title: Alabama Review of Loan Application: A Comprehensive Overview Introduction: The Alabama Review of Loan Application is a crucial process that determines the eligibility and feasibility of loan applications within the state of Alabama. This detailed description aims to provide an in-depth understanding of Alabama's loan application review process, including its various types and key considerations. Keywords: Alabama, loan application, review process, eligibility, feasibility, types, key considerations 1. Basic Rundown of the Alabama Review of Loan Application: The Alabama Review of Loan Application is a meticulous evaluation conducted by financial institutions to assess the eligibility and feasibility of loan applications. It ensures that applicants meet the established criteria for borrowing funds within the state. 2. Key Objectives of Alabama's Review Process: The main objectives of the Alabama Review of Loan Application include: — Assessing the borrower's creditworthiness — Verifying the borrower's financial stability — Evaluating the purpose and viability of the loan — Analyzing the potential risks associated with the loan request — Complying with state and federal lending regulations 3. Different Types of Alabama Review of Loan Application: a) Personal Loan Application Review: The personal loan application review focuses on individuals seeking financial assistance for personal endeavors, such as medical expenses, home renovations, or debt consolidation. This review examines the applicant's income, credit history, and overall financial standing. b) Business Loan Application Review: The business loan application review primarily caters to entrepreneurs and companies seeking financial support for business-related purposes. It assesses factors like the borrower's business plan, financial statements, cash flow projections, and assets or collateral offered. c) Mortgage Loan Application Review: Mortgage loan application review primarily targets individuals or families looking for financing to purchase or refinance residential properties. It scrutinizes the applicant's credit history, employment stability, income, and valuable assets to determine loan eligibility. 4. Key Considerations within the Alabama Review Process: a) Credit History and Score: The credit history and credit score play a pivotal role in determining loan approval. Lenders evaluate the applicant's repayment habits, past delinquencies, and credit utilization. b) Debt-to-Income Ratio (DTI): Lenders review an applicant's DTI to assess their ability to repay the loan. It compares their total monthly debt obligations to their monthly income. c) Collateral and Assets: In some loan types, collateral or assets may be required to secure the loan. This allows lenders to mitigate potential risks by utilizing the underlying asset as a source of repayment in case of default. d) Employment Stability and Income: Lenders evaluate an applicant's employment history, stability, and income to determine their ability to repay the loan on time. Conclusion: The Alabama Review of Loan Application is an extensive evaluation process that determines the feasibility and eligibility of loan applicants. By considering factors such as credit history, debt-to-income ratio, collateral/assets, and employment stability, lenders ensure responsible lending practices within the state of Alabama.

Alabama Review of Loan Application

Description

How to fill out Alabama Review Of Loan Application?

Discovering the right lawful file design might be a have a problem. Naturally, there are a lot of web templates available on the net, but how do you get the lawful develop you need? Utilize the US Legal Forms web site. The service provides 1000s of web templates, such as the Alabama Review of Loan Application, which can be used for business and private needs. All the varieties are checked out by professionals and meet federal and state needs.

In case you are presently authorized, log in to your accounts and then click the Download option to get the Alabama Review of Loan Application. Make use of accounts to look from the lawful varieties you may have acquired formerly. Proceed to the My Forms tab of your own accounts and acquire one more version of the file you need.

In case you are a new customer of US Legal Forms, allow me to share basic recommendations so that you can stick to:

- Initial, be sure you have chosen the right develop for your personal town/county. You can look over the form utilizing the Review option and browse the form outline to make sure it is the best for you.

- In the event the develop will not meet your requirements, use the Seach industry to get the appropriate develop.

- When you are certain the form is acceptable, click on the Acquire now option to get the develop.

- Opt for the pricing plan you would like and enter the needed details. Build your accounts and pay for the transaction utilizing your PayPal accounts or charge card.

- Select the submit format and download the lawful file design to your device.

- Full, revise and print and indication the received Alabama Review of Loan Application.

US Legal Forms is the greatest library of lawful varieties for which you will find numerous file web templates. Utilize the company to download expertly-created files that stick to state needs.