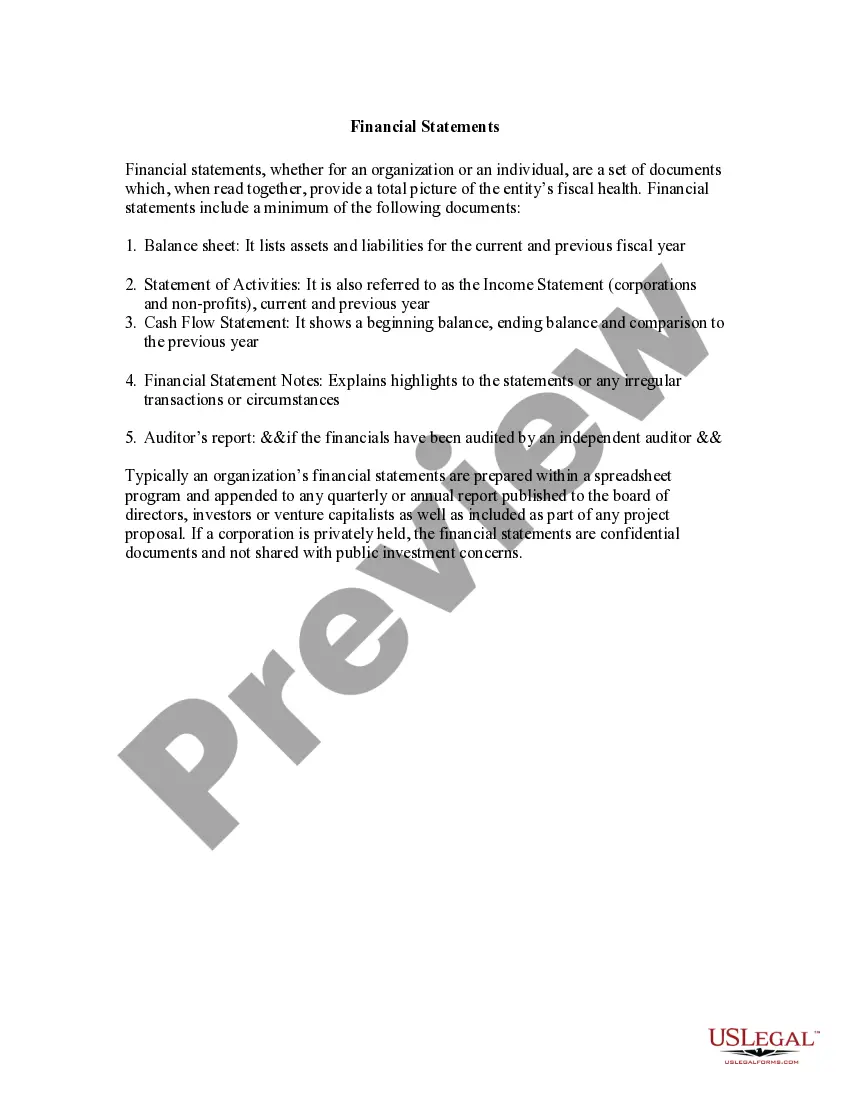

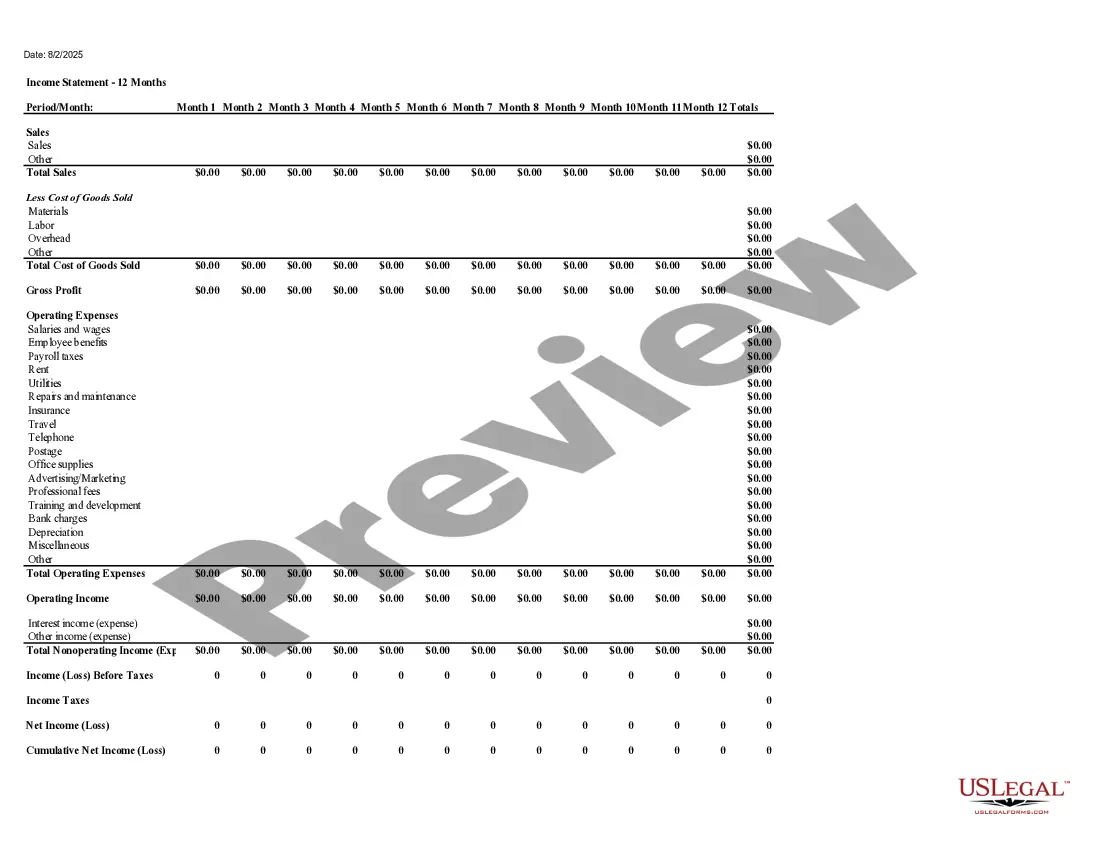

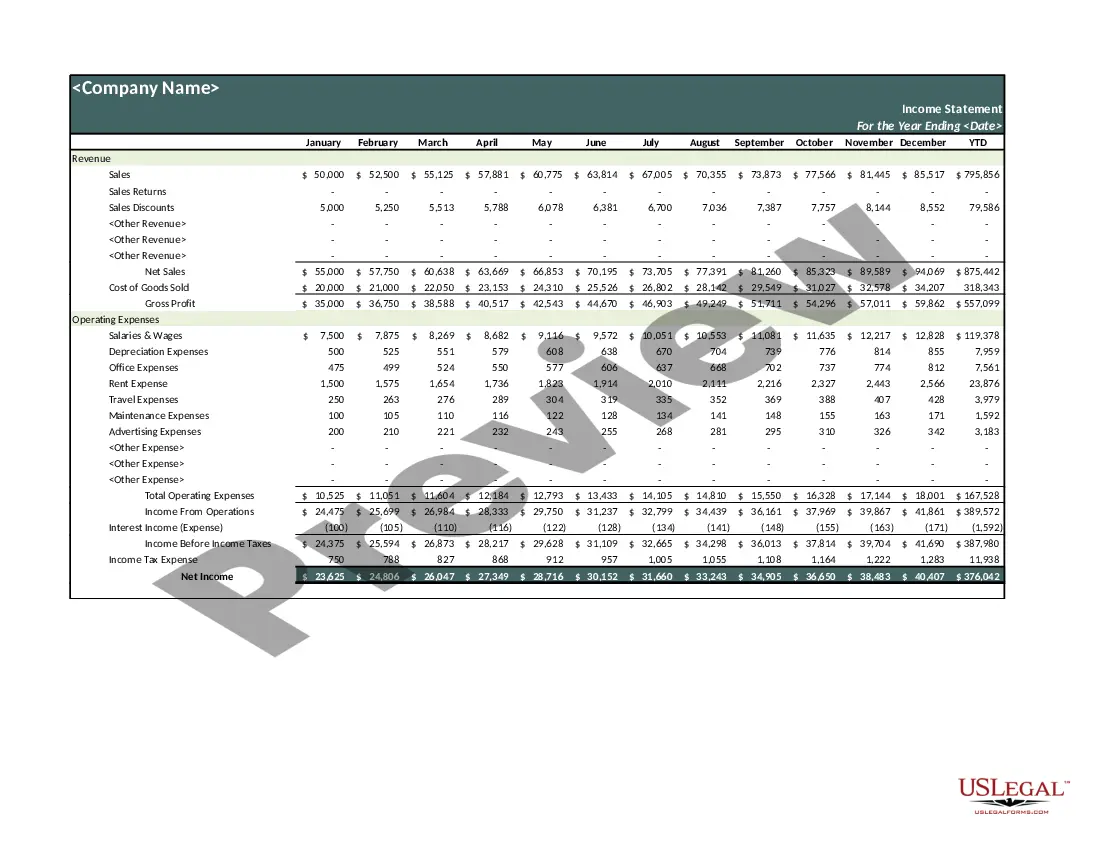

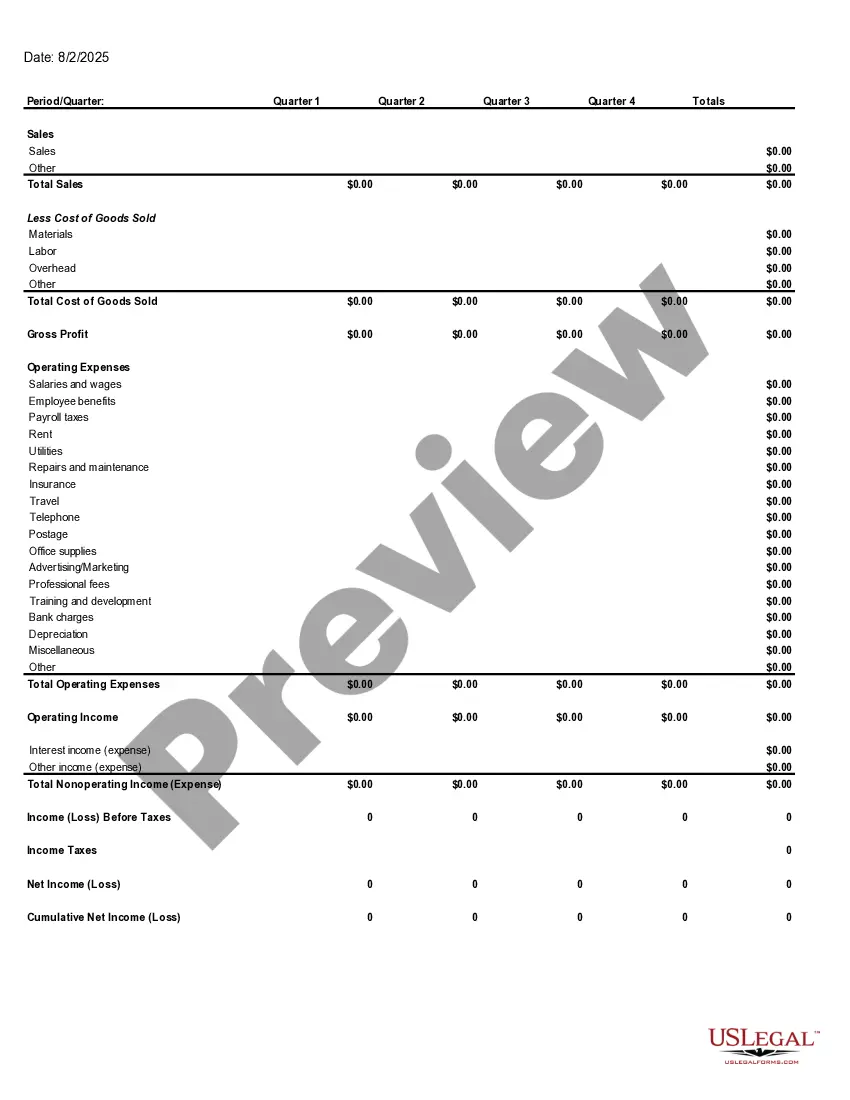

An income statement (sometimes called a profit and loss statement) lists your revenues and expenses, and tells you the profit or loss of your business for a given period of time. You can use this income statement form as a starting point to create one yourself.

Alabama Income Statement

Category:

State:

Multi-State

Control #:

US-03600BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Income Statement?

You can spend hours online trying to locate the legal document template that meets the federal and state requirements you seek.

US Legal Forms provides thousands of legal documents that are vetted by professionals.

You can obtain or create the Alabama Income Statement from the service.

If available, use the Preview button to view the document template as well.

- If you already have a US Legal Forms account, you can sign in and click the Download button.

- After that, you can complete, modify, print, or sign the Alabama Income Statement.

- Every legal document template you receive is yours permanently.

- To obtain another copy of the purchased template, visit the My documents tab and click the relevant button.

- If you're using the US Legal Forms website for the first time, follow the simple instructions below.

- First, ensure that you have selected the right document template for the area/city of your choice.

- Review the template details to confirm you’ve selected the correct form.

Form popularity

FAQ

You should file your Alabama annual report with the Alabama Secretary of State's office. This is essential for maintaining your business compliance and must accompany your Alabama Income Statement. If you seek assistance, platforms like US Legal Forms provide comprehensive resources to guide you through the report filing process. Ensuring your annual report is filed correctly is crucial for your business's success.

Yes, Alabama Form PPT can be filed electronically, making the process more efficient and convenient for you. Many taxpayers use online platforms to submit their Alabama Income Statement and other forms. US Legal Forms offers straightforward solutions for electronic filing, helping you navigate the requirements with ease. Embracing electronic filing can save you time and reduce the risk of errors.

Yes, you must file Alabama state income tax if you have a sufficient income level as defined by Alabama's tax laws. The Alabama Income Statement can help you report your earnings accurately. Consider using services like US Legal Forms for submitting your income statement smoothly and correctly. Filing on time ensures you meet your legal obligations and avoid penalties.

To calculate Alabama state income tax, begin by determining your taxable income, which is your total income minus any applicable deductions. Use the state’s tax rates to find your tax liability. The figures from your Alabama Income Statement will be crucial in this calculation. Consider using a tax calculator or professional advice to ensure accuracy in your computations.

In Alabama, individuals must file an income tax return if their gross income exceeds certain thresholds outlined by the state. This requirement applies regardless of filing status, so be sure to check the latest guidelines. Your Alabama Income Statement submission is essential to comply with these regulations. Understanding these requirements early can streamline your tax filing process.

Filing an income tax statement involves choosing a method that suits your needs, whether online or by mail. Collect your income documents and complete the necessary forms, keeping in mind to report all relevant income, including wages or self-employment earnings. Use online resources or platforms such as USLegalForms for assistance with your Alabama Income Statement. Don't forget to check the deadlines to avoid penalties.

A 1040 tax statement is the standard form used for individual income tax returns in the United States. It allows you to report your income, deductions, and credits. This form is crucial for completing your Alabama Income Statement accurately. It provides a comprehensive overview of your financial situation for the tax year.

To file your income tax, gather essential documents such as W-2 forms, 1099s, receipts for deductions, and previous tax returns. If you are self-employed, include your business financial records. These documents collectively contribute to your Alabama Income Statement, ensuring your filing process is organized and compliant. Always check for any additional documentation required by Alabama state rules.

When filling out your self-employment income, start by documenting all revenue generated from your business activities. Use Schedule C to report this income on your return. The totals from your Schedule C contribute to your Alabama Income Statement, so it’s vital to maintain accurate records of expenses as well. This will help in calculating your net profit and any tax dues.

Filing an income statement involves recording your earnings and expenses for the tax year. You can use templates available on platforms like USLegalForms to simplify this process. Ensure that all figures are accurate, as you will use this information in your Alabama Income Statement. Finally, submit your completed statement as required by the state.