Alabama Loan Guaranty Agreement

Description

How to fill out Loan Guaranty Agreement?

You can invest hrs on the web searching for the lawful document template which fits the federal and state needs you want. US Legal Forms gives thousands of lawful forms that are examined by professionals. It is simple to acquire or print the Alabama Loan Guaranty Agreement from our service.

If you already possess a US Legal Forms accounts, you are able to log in and then click the Obtain button. Next, you are able to total, change, print, or indication the Alabama Loan Guaranty Agreement. Every single lawful document template you acquire is the one you have eternally. To get an additional copy for any obtained kind, go to the My Forms tab and then click the corresponding button.

If you are using the US Legal Forms site the very first time, stick to the straightforward guidelines below:

- First, be sure that you have selected the right document template for that area/town of your choice. See the kind information to ensure you have picked out the right kind. If available, utilize the Preview button to look from the document template at the same time.

- If you wish to get an additional model of your kind, utilize the Lookup area to find the template that meets your requirements and needs.

- Once you have found the template you need, click Acquire now to continue.

- Find the rates program you need, key in your qualifications, and register for a free account on US Legal Forms.

- Comprehensive the financial transaction. You can use your credit card or PayPal accounts to pay for the lawful kind.

- Find the file format of your document and acquire it in your device.

- Make adjustments in your document if required. You can total, change and indication and print Alabama Loan Guaranty Agreement.

Obtain and print thousands of document layouts while using US Legal Forms website, that provides the largest variety of lawful forms. Use expert and condition-distinct layouts to handle your small business or person requires.

Form popularity

FAQ

A guaranty, much like any other contract, can be revoked later if both the guarantor and the lender agree in writing. Some debts owed by personal guarantors can also be discharged in bankruptcy.

A loan guarantee is a legally binding commitment to pay a debt in the event the borrower defaults. This most often occurs between family members, where the borrower can't obtain a loan because of a lack of income or down payment, or due to a poor credit rating.

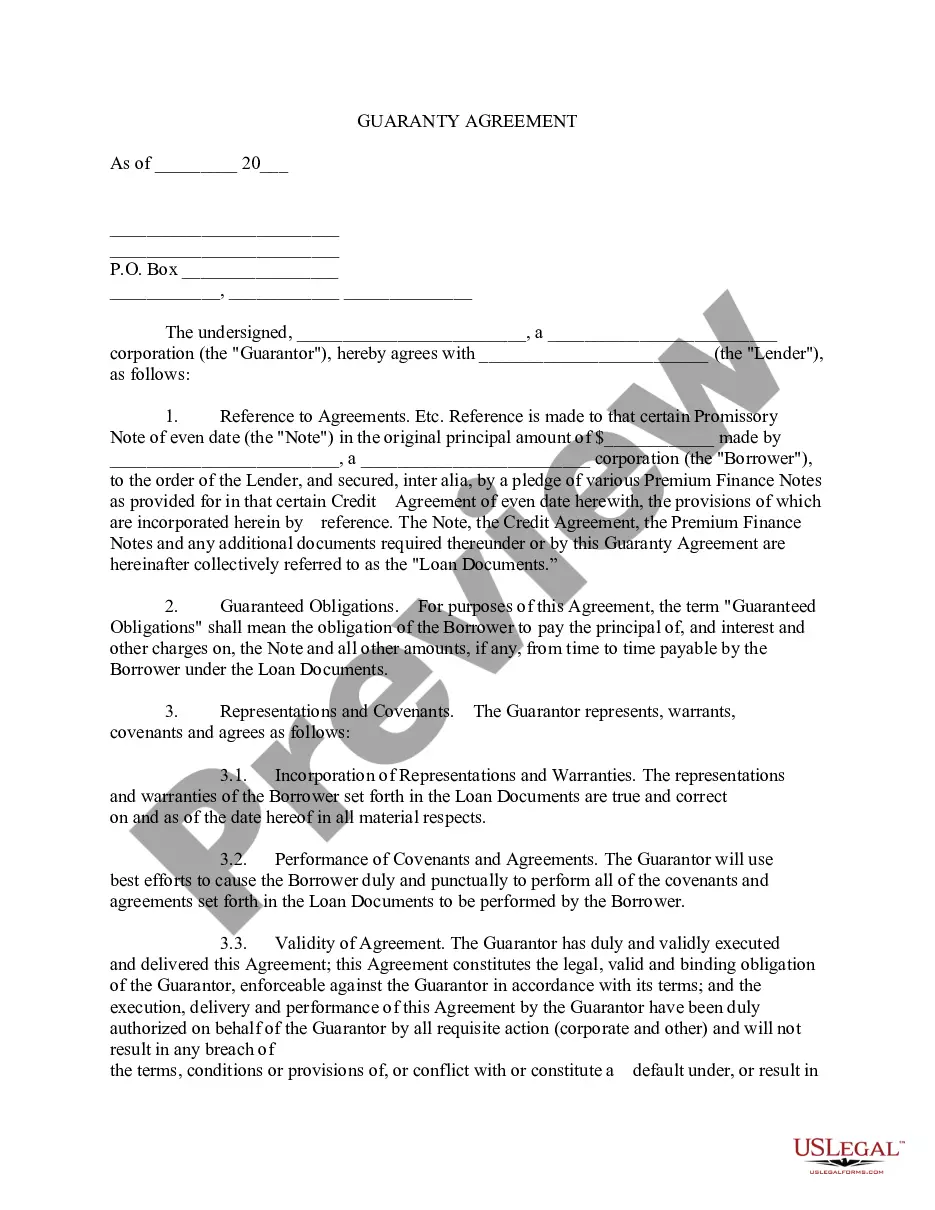

The Guarantor agrees that, if any of the Obligations are not paid when due, the Guarantor will, upon demand by the Bank, forthwith pay such Obligations, or if the maturity thereof shall have been accelerated by the Bank, the Guarantor will forthwith pay all Obligations of the Borrower.

A guaranty agreement, in the realm of commercial insurance, refers to a legally binding contract where one party, known as the guarantor, promises to be responsible for the obligations or debts of another party, known as the debtor, if they fail to fulfill their financial commitments.

Personal Financial Guarantees For example, lenders may require college students to get a guarantee from their parents or another party before they issue student loans. Other banks require a cash security deposit or form of collateral before they give out any credit. Don't confuse a guarantor with a cosigner.

As noted above, a surety is a guarantee or promise that assures payment through a legally binding contract. Under the agreement, one party promises to fulfill the financial obligations if the second party (the debtor) fails to pay the third party (the creditor).

A guaranty agreement is a two-party contract in which the first party agrees to perform a stipulated action in the event that a second party fails to perform.

Contract Of Guarantee Example There is a contract of guarantee, where A requests B to lend Rs. 20,000 to C and assures that C will pay back the sum within the agreed period. If C fails to make payments, A will repay B as per the agreement agreed between them under the ContractContract of guarantee.