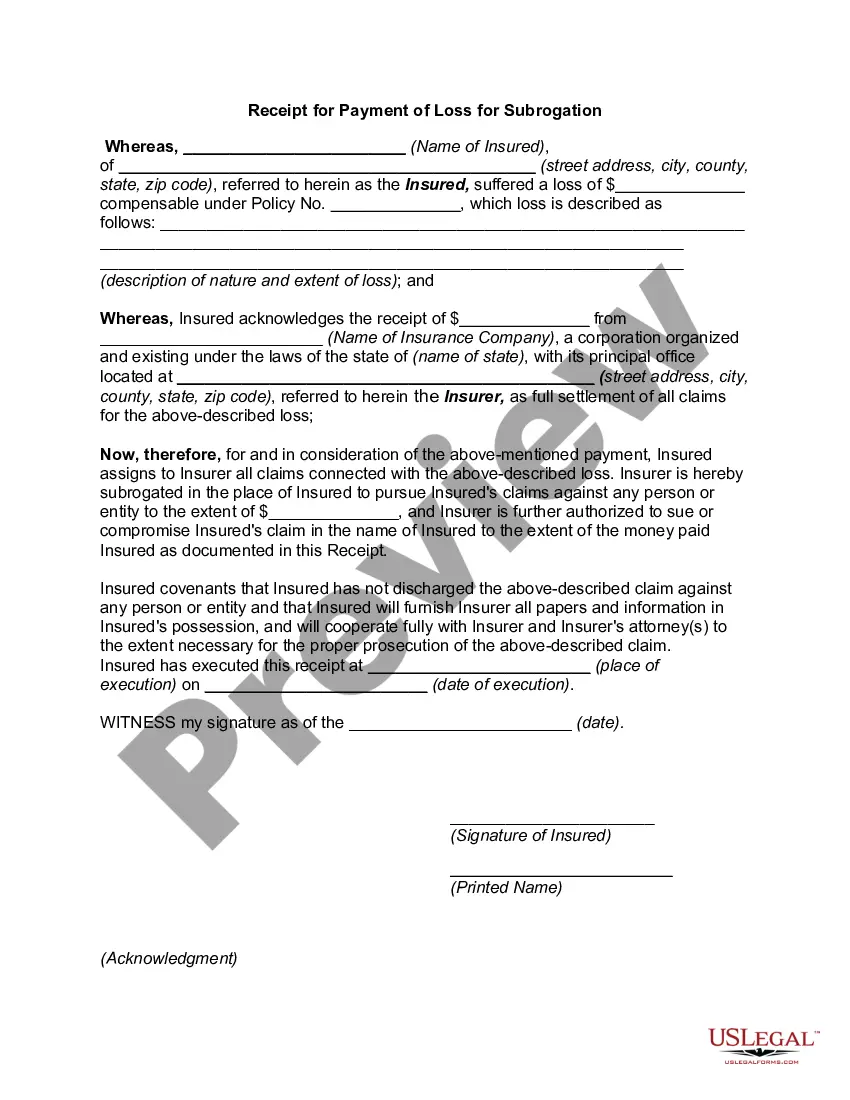

In Alabama, a Receipt for Payment of Loss for Subrogation is a legal document that acknowledges the payment made by an insurer to a policyholder for a loss covered under the insurance policy. This receipt is a crucial part of the subrogation process, which involves the transfer of the rights and claims of the policyholder to the insurer after the latter has settled a claim on the policyholder's behalf. This document serves as evidence that the insurer has reimbursed the policyholder for the loss sustained, allowing the insurer to pursue the responsible party and seek reimbursement from them. It includes specific details related to the payment, such as the amount paid, the date of payment, and the policy number. There are several types of Alabama Receipt for Payment of Loss for Subrogation, each serving a specific purpose based on the circumstances of the claim. These may include: 1. Property Subrogation Receipt: This type of receipt is used when the loss involves damage or destruction to property covered under an insurance policy. It is filled out by the policyholder and serves as confirmation of the insurer's payment for the loss incurred. 2. Auto Subrogation Receipt: When a loss involves an automobile covered under an insurance policy, an Auto Subrogation Receipt is used. Similar to the Property Subrogation Receipt, it acknowledges the insurer's payment to the policyholder for damages to the insured vehicle. 3. Workers' Compensation Subrogation Receipt: In cases where an employee sustains a work-related injury or illness, the employer's workers' compensation insurer may need to issue a Workers' Compensation Subrogation Receipt. This receipt confirms that the insurer has compensated the policyholder for their medical expenses, lost wages, or other incurred costs due to the workplace incident. By issuing the Alabama Receipt for Payment of Loss for Subrogation, insurers ensure that their rights are protected and may pursue legal action against liable parties to recover the amount paid to policyholders. It is crucial for both insurers and policyholders involved in subrogation to understand and adhere to the requirements and processes outlined by Alabama law.

Alabama Receipt for Payment of Loss for Subrogation

Description

How to fill out Alabama Receipt For Payment Of Loss For Subrogation?

If you wish to total, down load, or print legitimate document themes, use US Legal Forms, the most important collection of legitimate types, that can be found on the Internet. Make use of the site`s basic and convenient lookup to discover the files you will need. A variety of themes for business and person uses are categorized by categories and claims, or keywords and phrases. Use US Legal Forms to discover the Alabama Receipt for Payment of Loss for Subrogation with a few mouse clicks.

In case you are presently a US Legal Forms client, log in in your profile and click the Down load option to obtain the Alabama Receipt for Payment of Loss for Subrogation. You may also accessibility types you in the past acquired from the My Forms tab of your profile.

If you are using US Legal Forms for the first time, follow the instructions below:

- Step 1. Be sure you have chosen the form for your correct area/country.

- Step 2. Make use of the Preview choice to examine the form`s content material. Never forget to read through the explanation.

- Step 3. In case you are not satisfied together with the develop, take advantage of the Look for discipline near the top of the screen to locate other versions of your legitimate develop web template.

- Step 4. Upon having located the form you will need, go through the Purchase now option. Pick the costs prepare you prefer and include your qualifications to sign up to have an profile.

- Step 5. Method the deal. You can utilize your Мisa or Ьastercard or PayPal profile to complete the deal.

- Step 6. Choose the file format of your legitimate develop and down load it on your own product.

- Step 7. Comprehensive, change and print or indicator the Alabama Receipt for Payment of Loss for Subrogation.

Each and every legitimate document web template you get is the one you have eternally. You possess acces to each develop you acquired in your acccount. Go through the My Forms segment and choose a develop to print or down load again.

Remain competitive and down load, and print the Alabama Receipt for Payment of Loss for Subrogation with US Legal Forms. There are millions of specialist and state-certain types you may use to your business or person needs.