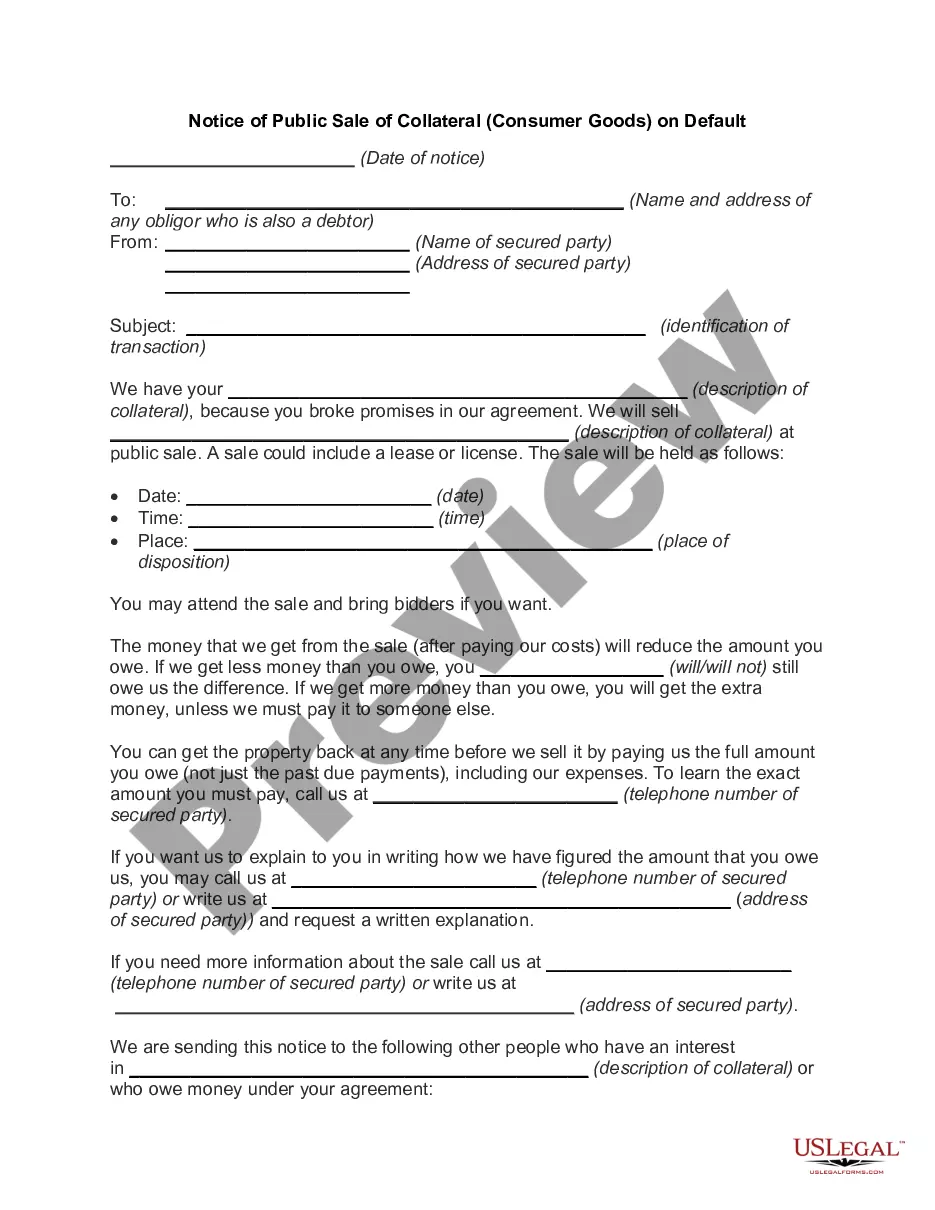

Title: Alabama Notice of Public Sale of Collateral (Consumer Goods) on Default: A Comprehensive Guide Introduction: The Alabama Notice of Public Sale of Collateral (Consumer Goods) on Default is a legal document that outlines the process and requirements for a public sale of collateral, specifically consumer goods, in the event of a default on a secured loan. This detailed description serves as a valuable reference for individuals seeking information about the process and types of Alabama Notice of Public Sale of Collateral (Consumer Goods) on Default. Keywords: Alabama, Notice of Public Sale, Collateral, Consumer Goods, Default, Secured Loan Types of Alabama Notice of Public Sale of Collateral (Consumer Goods) on Default: 1. Vehicle Repossession: In cases where an individual defaults on an auto loan or lease agreement, the lender may issue an Alabama Notice of Public Sale of Collateral (Consumer Goods) to initiate the process of repossessing and selling the vehicle to recover the outstanding debt. 2. Foreclosure Sale: For defaulting on mortgage loans related to residential properties, lenders can issue an Alabama Notice of Public Sale of Collateral (Consumer Goods) to organize a foreclosure sale. This serves as a means for the lender to recover the amount owed by selling the property to the highest bidder. 3. Personal Property Sale: In situations where an individual defaults on a loan secured by personal property, such as electronics, appliances, furniture, or jewelry, lenders may issue an Alabama Notice of Public Sale of Collateral (Consumer Goods) to initiate the sale of these items in order to recoup the outstanding debt. Key Components of an Alabama Notice of Public Sale of Collateral (Consumer Goods) on Default: 1. Identification of Parties: The notice should clearly identify the lender, as well as the borrower or debtor involved in the transaction. 2. Description of Collateral: A detailed description of the consumer goods being offered for sale must be included in the notice. This typically includes make, model, year, VIN (Vehicle Identification Number), condition, and any other relevant details. 3. Default Information: The notice should state the specifics of the default, including the amount owed, the date of default, and any previous attempts made to resolve the issue. 4. Auction/Sale Details: Important information about the date, time, and location of the public sale should be provided. This enables potential buyers to participate in the auction or attend the sale. 5. Redemption Rights and Cure Period: Informing the borrower of their rights to redeem or cure the default within a specified period is crucial. This allows them an opportunity to settle the debt before the public sale proceeds. 6. Sale Conduct: The notice should outline the procedure for bidding, accepted payment methods, and any special terms or conditions set forth by the lender. Conclusion: Understanding the intricacies of an Alabama Notice of Public Sale of Collateral (Consumer Goods) on Default is crucial for both lenders and borrowers. By following the necessary steps and complying with legal requirements, lenders can recover their dues, while borrowers retain an opportunity to reclaim their collateral before the public sale.

Alabama Notice of Public Sale of Collateral (Consumer Goods) on Default

Description

How to fill out Alabama Notice Of Public Sale Of Collateral (Consumer Goods) On Default?

You are able to commit several hours on the Internet trying to find the legitimate file design that suits the state and federal needs you need. US Legal Forms offers a large number of legitimate types that happen to be evaluated by pros. It is simple to obtain or printing the Alabama Notice of Public Sale of Collateral (Consumer Goods) on Default from your assistance.

If you already have a US Legal Forms profile, you may log in and click the Down load option. Following that, you may full, revise, printing, or sign the Alabama Notice of Public Sale of Collateral (Consumer Goods) on Default. Every single legitimate file design you purchase is your own property eternally. To acquire yet another duplicate of the purchased kind, visit the My Forms tab and click the related option.

Should you use the US Legal Forms site for the first time, follow the easy recommendations beneath:

- First, ensure that you have selected the right file design to the state/area of your choosing. Look at the kind explanation to ensure you have picked out the appropriate kind. If accessible, take advantage of the Review option to search from the file design also.

- If you wish to get yet another model of the kind, take advantage of the Research discipline to discover the design that meets your needs and needs.

- Once you have located the design you want, simply click Acquire now to proceed.

- Choose the rates program you want, enter your qualifications, and sign up for your account on US Legal Forms.

- Comprehensive the purchase. You can use your bank card or PayPal profile to pay for the legitimate kind.

- Choose the structure of the file and obtain it in your device.

- Make modifications in your file if needed. You are able to full, revise and sign and printing Alabama Notice of Public Sale of Collateral (Consumer Goods) on Default.

Down load and printing a large number of file web templates utilizing the US Legal Forms site, that provides the greatest collection of legitimate types. Use expert and state-certain web templates to take on your organization or personal needs.