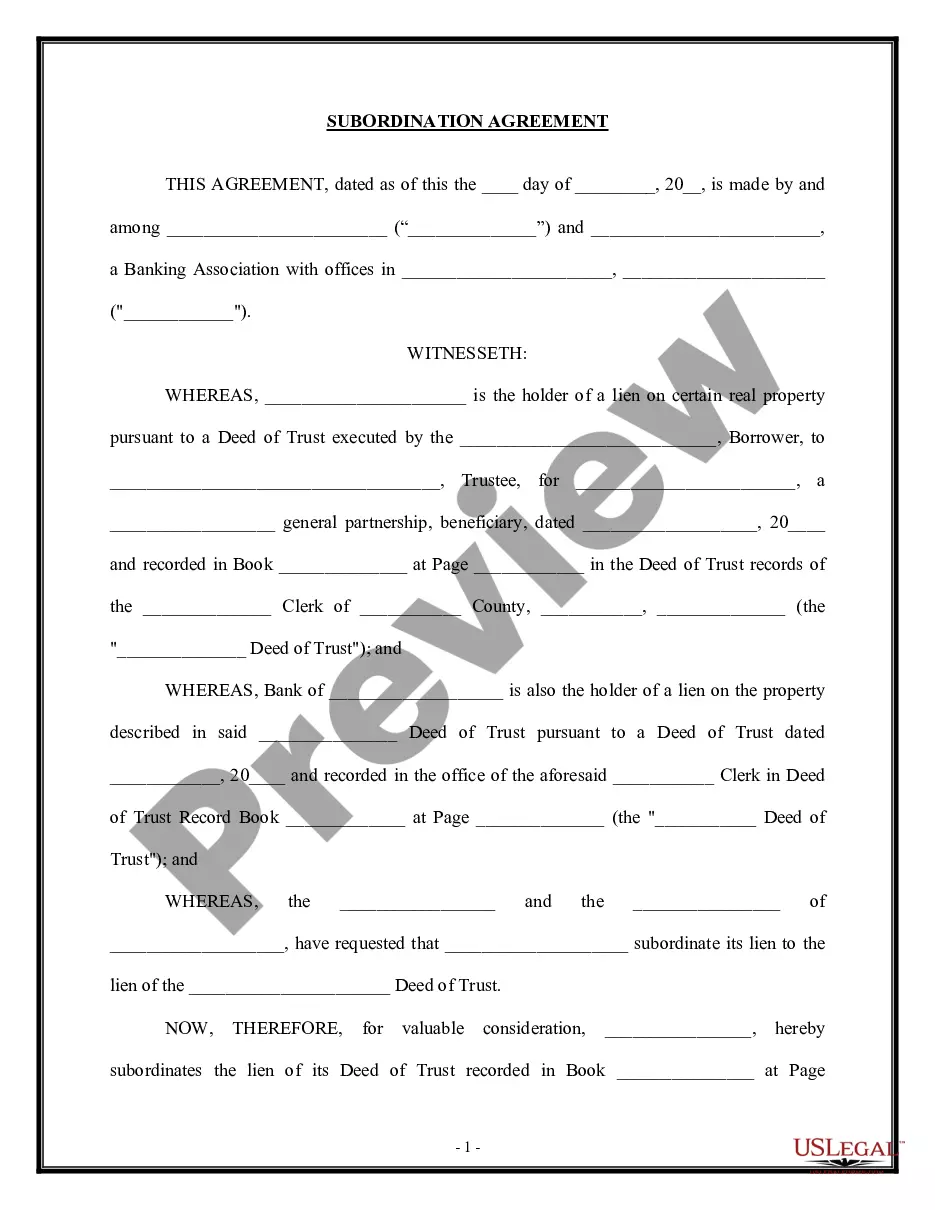

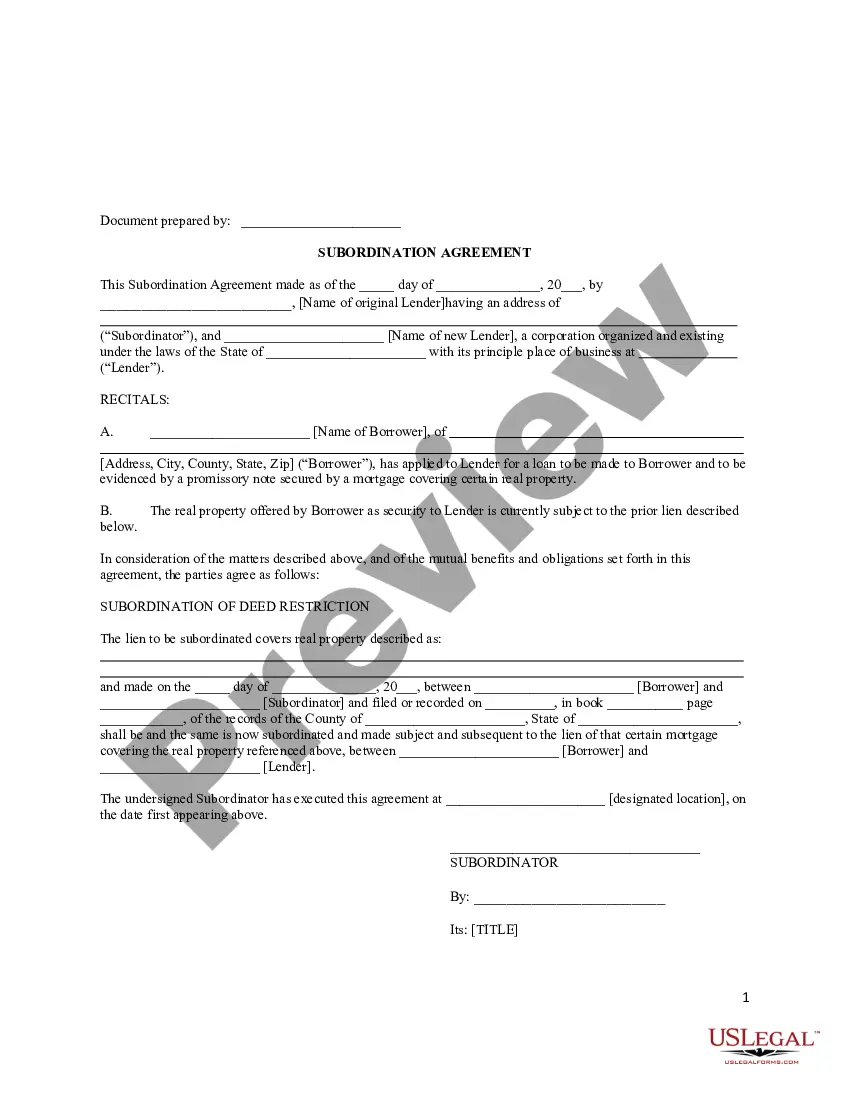

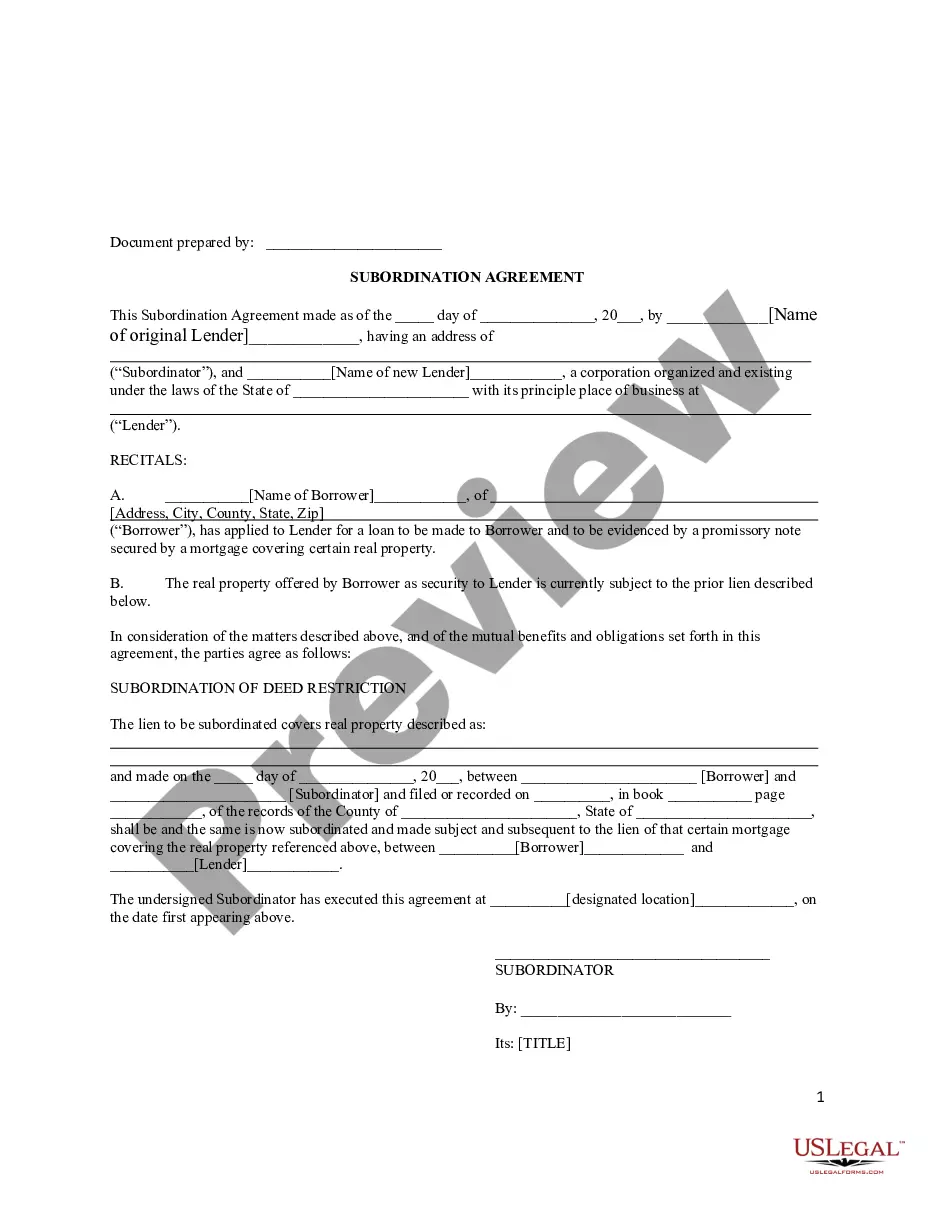

Alabama Subordination Agreement Subordinating Existing Mortgage to New Mortgage

Description

How to fill out Subordination Agreement Subordinating Existing Mortgage To New Mortgage?

You can invest hours on the Internet searching for the legitimate papers format that fits the state and federal demands you will need. US Legal Forms provides thousands of legitimate varieties that happen to be examined by experts. It is possible to down load or produce the Alabama Subordination Agreement Subordinating Existing Mortgage to New Mortgage from my service.

If you currently have a US Legal Forms bank account, you are able to log in and click on the Download option. Next, you are able to complete, edit, produce, or indication the Alabama Subordination Agreement Subordinating Existing Mortgage to New Mortgage. Every single legitimate papers format you acquire is the one you have for a long time. To get an additional backup associated with a bought type, go to the My Forms tab and click on the corresponding option.

Should you use the US Legal Forms web site initially, follow the basic instructions under:

- Initial, make certain you have chosen the right papers format to the region/town of your choosing. Browse the type outline to ensure you have picked the proper type. If readily available, make use of the Review option to appear throughout the papers format also.

- If you wish to discover an additional model in the type, make use of the Research field to get the format that suits you and demands.

- Upon having found the format you desire, simply click Buy now to move forward.

- Select the pricing prepare you desire, key in your references, and register for an account on US Legal Forms.

- Total the financial transaction. You can use your credit card or PayPal bank account to purchase the legitimate type.

- Select the file format in the papers and down load it to the system.

- Make alterations to the papers if needed. You can complete, edit and indication and produce Alabama Subordination Agreement Subordinating Existing Mortgage to New Mortgage.

Download and produce thousands of papers themes using the US Legal Forms web site, that provides the biggest collection of legitimate varieties. Use specialist and state-particular themes to handle your business or individual needs.

Form popularity

FAQ

Many people have a subordinate mortgage in the form of a home equity line of credit or home equity loan. A subordinate mortgage is secured by your property but sits in second position, if you have a primary mortgage, for getting paid in the event you default.

A subordinate mortgage loan is any loan not in the first lien position. The subordination order goes by the order the loans were recorded. For example, your first mortgage (the mortgage used to buy the house) is recorded first because it's the first loan you borrow.

Many people have a subordinate mortgage in the form of a home equity line of credit or home equity loan. A subordinate mortgage is secured by your property but sits in second position, if you have a primary mortgage, for getting paid in the event you default.

When you get a mortgage loan, the lender will likely include a subordination clause essentially stating that their lien will take precedence over any other liens placed on the house. A subordination clause serves to protect the lender if a homeowner defaults.

Subordination agreements may be included in existing deeds of trust or may be outlined in an independent contract. In situations where two deeds of trust are being recorded concurrently, the lien priority is typically handled by instructing the title company as to which security instrument will be recorded first.

Subordination clauses are most commonly found in mortgage refinancing agreements. Consider a homeowner with a primary mortgage and a second mortgage. If the homeowner refinances his primary mortgage, this in effect means canceling the first mortgage and reissuing a new one.

A subordinated loan is debt that's only paid off after all primary loans are paid off, if there's any money left. It's also known as subordinated debt, junior debt or a junior security, while primary loans are also known as senior or unsubordinated debt.

Any subsequent loan that is taken out after your initial purchase loan is considered to be a junior-lien or subordinate mortgage. Therefore, subordinate financing is the use of two or more mortgages to finance the purchase of real estate or using your home's equity for liquid cash.