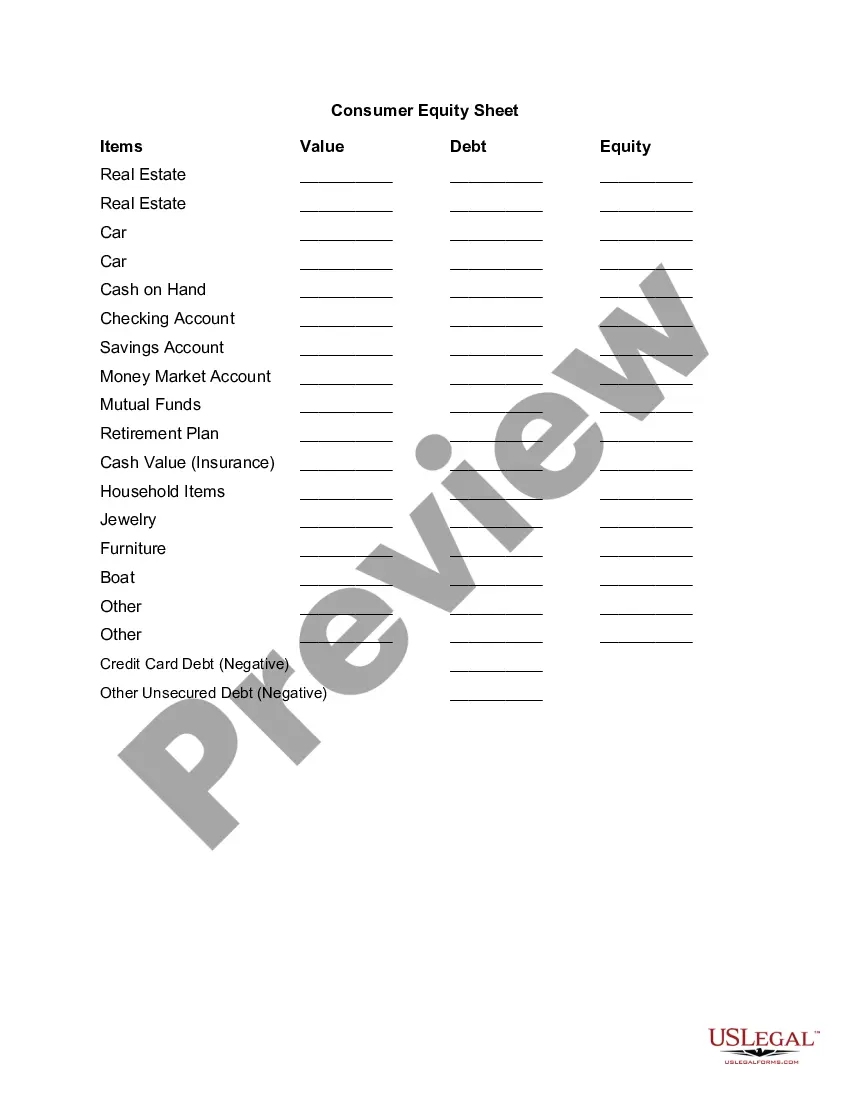

Alabama Consumer Equity Sheet is a comprehensive document that provides detailed information on the financial standing of consumers in the state of Alabama. This document contains relevant statistics, figures, and data to assess the economic health of individuals and households residing in Alabama. The Alabama Consumer Equity Sheet serves as a consolidated report, highlighting key indicators such as assets, liabilities, net worth, debt ratios, and equity for both individuals and families. This comprehensive overview allows policymakers, economists, and financial institutions to understand and analyze the economic landscape and trends in Alabama. This consumer equity sheet is crucial in evaluating the financial stability and well-being of Alabama residents. It provides a snapshot of their overall financial health, including homeownership, investments, savings, and outstanding debts. By examining this data, it becomes possible to assess the level of financial security and stability among Alabama consumers. Key elements included in the Alabama Consumer Equity Sheet are: 1. Assets: This section outlines the various assets owned by Alabama consumers, including real estate properties, vehicles, investments, retirement savings, and other valuable possessions. 2. Liabilities: Here, Alabama individuals and households will find a breakdown of their outstanding debts, such as mortgages, auto loans, student loans, credit card debts, and other forms of liabilities. 3. Net worth: The net worth section provides an overview of the financial health of Alabama consumers by calculating the difference between their total assets and total liabilities. It indicates the overall financial standing and wealth accumulation of individuals and families residing in Alabama. 4. Debt ratios: This section focuses on measuring the debt burden of Alabama consumers. It presents key debt ratios such as debt-to-income ratio, debt-to-asset ratio, and debt-to-equity ratio, offering insights into the level of debt compared to income and assets. 5. Equity: The equity portion of the Alabama Consumer Equity Sheet showcases the amount of ownership individuals and households have in their assets. It calculates the equity value in properties, investments, and other assets, reflecting the degree of ownership and financial stability of Alabama residents. Different types of Alabama Consumer Equity Sheets may include specific categories tailored to various demographics or sectors within the state. For instance: — Personal Consumer Equity Sheet: This focuses on individual financial statistics and indicators, providing insights into personal net worth, asset allocation, and debt management. — Household Consumer Equity Sheet: This type offers a broader perspective by considering the financial position of households, including multiple individuals residing together. It provides a comprehensive overview of assets, liabilities, and net worth for the entire household. Overall, the Alabama Consumer Equity Sheet plays a pivotal role in understanding the financial landscape of Alabama residents, aiding policymakers, economists, and financial institutions in making informed decisions and developing strategies that contribute to the economic growth and well-being of the state's consumers.

Alabama Consumer Equity Sheet

Description

How to fill out Alabama Consumer Equity Sheet?

You can invest hours online trying to find the legitimate file format that fits the state and federal requirements you will need. US Legal Forms supplies 1000s of legitimate forms that happen to be examined by experts. You can easily down load or produce the Alabama Consumer Equity Sheet from your services.

If you already have a US Legal Forms profile, you can log in and then click the Down load key. After that, you can full, change, produce, or signal the Alabama Consumer Equity Sheet. Every single legitimate file format you purchase is the one you have permanently. To have yet another backup of the purchased form, check out the My Forms tab and then click the corresponding key.

If you use the US Legal Forms website for the first time, stick to the basic guidelines beneath:

- Initially, make sure that you have chosen the best file format for that region/area of your choice. See the form description to make sure you have chosen the right form. If available, utilize the Review key to look through the file format also.

- If you want to discover yet another version from the form, utilize the Lookup industry to obtain the format that meets your needs and requirements.

- After you have found the format you want, click Get now to carry on.

- Find the pricing program you want, type in your accreditations, and register for an account on US Legal Forms.

- Complete the purchase. You should use your charge card or PayPal profile to fund the legitimate form.

- Find the file format from the file and down load it to the system.

- Make changes to the file if needed. You can full, change and signal and produce Alabama Consumer Equity Sheet.

Down load and produce 1000s of file themes utilizing the US Legal Forms website, which provides the greatest assortment of legitimate forms. Use specialist and express-certain themes to deal with your business or specific requirements.