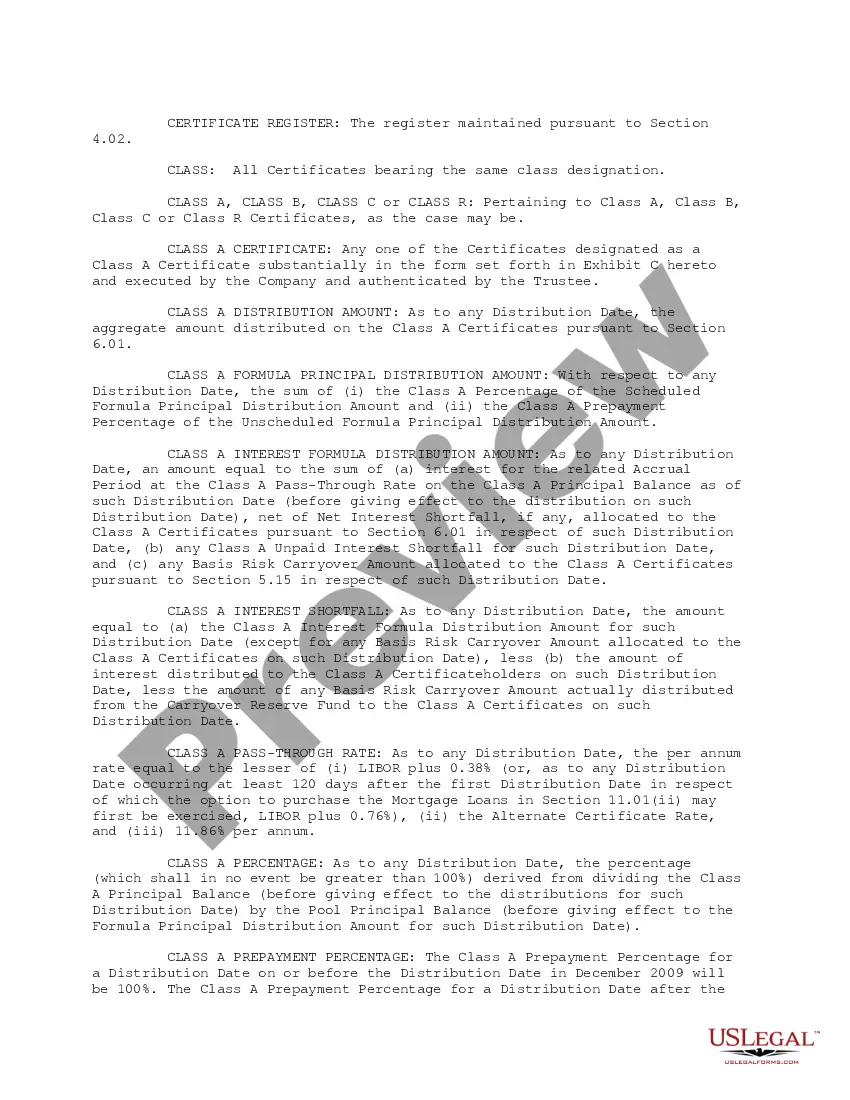

Alabama Pooling and Servicing Agreement: Contemplating the Sale of Mortgage Loans to Trustee for Inclusion in the Trust Fund by the Company The Alabama Pooling and Servicing Agreement (PSA) is a legal document that outlines the terms and conditions for the sale of mortgage loans by a company to a trustee. The purpose of this agreement is to combine multiple mortgage loans into a single investment entity known as a trust fund. By doing so, the company aims to transfer the loan ownership and associated risks to the trustee, ultimately allowing for the creation of mortgage-backed securities. In this process, the company, often a mortgage originator or loan service, sells a pool of mortgage loans to the trustee. The trustee, which can be a financial institution or a specialized entity, assumes the responsibility of managing and administering the loans on behalf of the investors who hold an interest in the trust fund. This arrangement allows for the diversification of risks and the potential for investors to earn returns based on the performance of the underlying mortgage loans. The Alabama PSA ensures compliance with legal requirements and establishes guidelines for the servicing of the mortgage loans within the trust fund. It typically covers aspects such as: 1. Loan Pool Composition: The agreement outlines the characteristics of the mortgage loans eligible for inclusion in the trust fund. Criteria including loan type, interest rate, loan-to-value ratio, credit score requirements, and other relevant factors are defined to ensure the quality and consistency of the loan portfolio. 2. Sale and Transfer Process: The steps involved in the sale and transfer of the mortgage loans from the company to the trustee are detailed in the PSA. This includes the transfer of title, documentation requirements, and the delivery of requisite loan files, ensuring a smooth transition of ownership. 3. Trustee Responsibilities: The PSA specifies the trustee's obligations, including the administration, monitoring, and management of the mortgage loans within the trust fund. This involves collecting principal and interest payments from borrowers, distributing funds to investors, handling default management, and ensuring compliance with applicable regulations. 4. Servicing Standards: The agreement defines the servicing standards that the trustee must adhere to when interacting with borrowers and managing the loans. This encompasses borrower communications, payment processing, escrow management, loan modifications, collections, foreclosure procedures, and other borrower-related matters. 5. Reporting and Disclosures: The PSA stipulates reporting requirements for the trustee to provide regular updates to investors regarding the performance of the trust fund. This includes the provision of periodic statements, investor reports, and disclosure of any material events or changes that may affect the trust fund's performance. Different types of Alabama Pooling and Servicing Agreements contemplating the sale of mortgage loans to the trustee for inclusion in the trust fund may vary based on specific features or characteristics of the mortgage loans. Common variations include: 1. Fixed-Rate Mortgage PSA: This type of PSA focuses on the sale and servicing of fixed-rate mortgage loans, where the borrowers pay a consistent interest rate throughout the loan term. 2. Adjustable-Rate Mortgage PSA: This variation of the agreement deals with the sale and servicing of adjustable-rate mortgage loans, where the interest rates can fluctuate over the course of the loan term based on prevailing market conditions. 3. Government-Insured Mortgage PSA: This PSA addresses the sale and servicing of mortgage loans insured by government agencies such as the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA). In conclusion, the Alabama Pooling and Servicing Agreement provides a comprehensive framework for the sale and administration of mortgage loans within a trust fund. It facilitates the packaging of these loans into mortgage-backed securities, allowing investors to participate in the potential returns and risks associated with the underlying mortgage loans.

Alabama Pooling and Servicing Agreement contemplating the sale of mortgage loans to Trustee for inclusion in the Trust Fund by the company

Description

How to fill out Alabama Pooling And Servicing Agreement Contemplating The Sale Of Mortgage Loans To Trustee For Inclusion In The Trust Fund By The Company?

US Legal Forms - one of the greatest libraries of authorized types in the United States - delivers a wide array of authorized papers layouts you may acquire or print out. Using the web site, you will get thousands of types for organization and person purposes, categorized by groups, claims, or search phrases.You will find the newest variations of types much like the Alabama Pooling and Servicing Agreement contemplating the sale of mortgage loans to Trustee for inclusion in the Trust Fund by the company in seconds.

If you already have a membership, log in and acquire Alabama Pooling and Servicing Agreement contemplating the sale of mortgage loans to Trustee for inclusion in the Trust Fund by the company from your US Legal Forms library. The Obtain key can look on every single form you see. You have access to all formerly delivered electronically types within the My Forms tab of your own bank account.

In order to use US Legal Forms for the first time, listed here are easy directions to obtain started out:

- Be sure you have chosen the best form for the metropolis/area. Go through the Review key to review the form`s content material. Browse the form outline to actually have chosen the appropriate form.

- If the form doesn`t fit your demands, take advantage of the Lookup discipline near the top of the display to discover the one which does.

- If you are satisfied with the shape, verify your selection by clicking on the Purchase now key. Then, pick the pricing plan you favor and provide your qualifications to register to have an bank account.

- Method the financial transaction. Use your credit card or PayPal bank account to complete the financial transaction.

- Choose the file format and acquire the shape in your product.

- Make modifications. Fill up, edit and print out and indicator the delivered electronically Alabama Pooling and Servicing Agreement contemplating the sale of mortgage loans to Trustee for inclusion in the Trust Fund by the company.

Each and every web template you included in your account does not have an expiration date and it is the one you have forever. So, in order to acquire or print out yet another backup, just go to the My Forms portion and click around the form you require.

Obtain access to the Alabama Pooling and Servicing Agreement contemplating the sale of mortgage loans to Trustee for inclusion in the Trust Fund by the company with US Legal Forms, the most substantial library of authorized papers layouts. Use thousands of expert and status-certain layouts that fulfill your business or person requires and demands.

Form popularity

FAQ

PSA is used primarily to derive an implied prepayment speed of new production loans. 00% PSA assumes a prepayment rate of 2% per month in the first month following the date of issue, increasing at 2% percentage points per month thereafter until the 30th month. PSA Prepayment Rate Definition - Nasdaq nasdaq.com ? glossary ? psa-prepayment-rate nasdaq.com ? glossary ? psa-prepayment-rate

An MBS is made up of a pool of mortgages purchased from issuing banks and then sold to investors. An MBS allows investors to benefit from the mortgage business without needing to buy or sell home loans themselves. What Are Mortgage-Backed Securities? rocketmortgage.com ? learn ? mortgage-bac... rocketmortgage.com ? learn ? mortgage-bac...

Mortgage servicing rights (MSR) refer to a contractual agreement in which the right to service an existing mortgage is sold by the original mortgage lender to another party that specializes in the various functions involved with servicing mortgages.

What is a Pooling Agreement? A pooling agreement is a type of contract where corporate shareholders create a voting trust by pooling their voting rights and transferring them to a trustee. This is also called a voting agreement or shareholder-control agreement since it is used to control the affairs of the corporation. Pooling Agreement: Definition & Sample - Contracts Counsel contractscounsel.com ? pooling-agreement contractscounsel.com ? pooling-agreement

A mortgage pool is a group of home and other real estate loans that have been bundled so they can be sold. A mortgage pool is a group of home and other real estate loans that have been bundled so they can be sold. What Is a Mortgage Pool? - The Balance thebalancemoney.com ? what-is-a-mortgage... thebalancemoney.com ? what-is-a-mortgage...

The ?Pooling and Servicing Agreement? is the legal document that contains the responsibilities and rights of the servicer, the trustee, and others over a pool of mortgage loans.