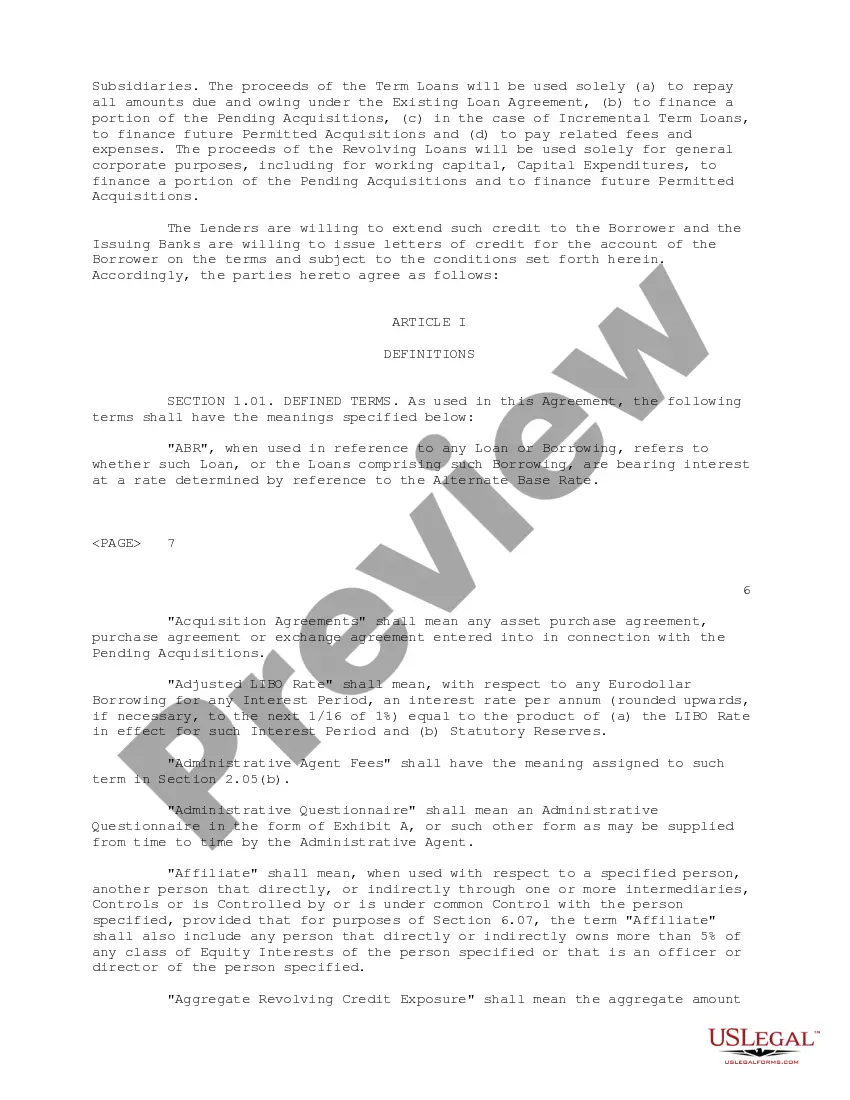

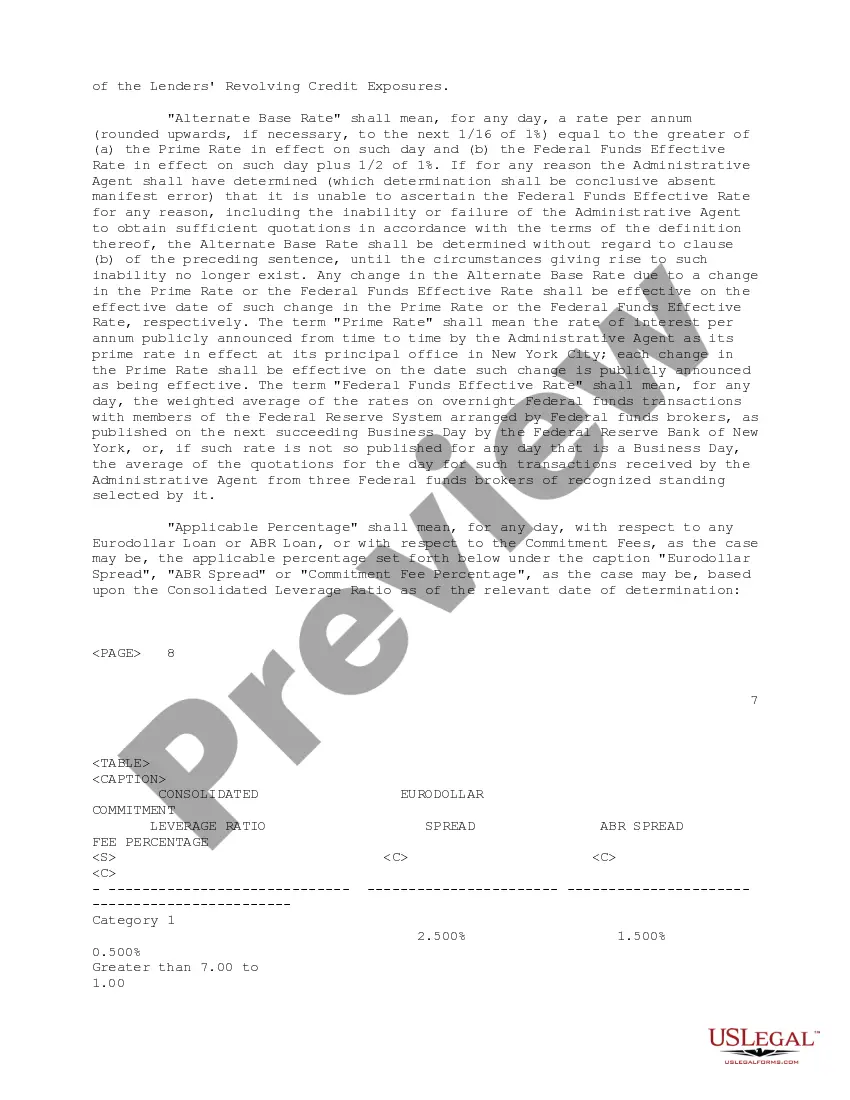

Alabama Credit Agreement Regarding Extension of Credit The Alabama Credit Agreement regarding extension of credit is a legally binding contract between a lender and a borrower that governs the terms and conditions of providing credit in the state of Alabama. This agreement outlines the rights and responsibilities of both parties and ensures compliance with state laws and regulations. The Alabama Credit Agreement may vary depending on the specific type of credit being extended. Here are some common types: 1. Revolving Credit Agreement: This type of agreement allows the borrower to have a credit limit that can be borrowed, repaid, and borrowed again in a revolving manner. The borrower has the flexibility to use the credit line whenever needed. 2. Installment Credit Agreement: In this agreement, the lender provides a fixed amount of credit to the borrower, which is to be repaid in regular installments over a set period of time. The loan terms, including the interest rate, repayment schedule, and fees, are clearly defined in the contract. 3. Secured Credit Agreement: This type of credit agreement requires the borrower to provide collateral, such as real estate or a vehicle, as security for the credit extended. Should the borrower default on the loan, the lender has the right to seize the collateral to recover the outstanding debt. 4. Unsecured Credit Agreement: Unlike a secured credit agreement, an unsecured credit agreement does not require collateral. The lender extends credit to the borrower based on their creditworthiness and trust, without any specific asset acting as security. As a result, unsecured credit agreements may have higher interest rates to compensate for the increased risk. The Alabama Credit Agreement contains various important components, including: — Parties Involved: The agreement identifies the lender and the borrower, providing their legal names, contact details, and any other pertinent information. — Credit Terms: This section outlines the specific terms of the credit being extended, including the credit amount, interest rate, and any additional fees or charges. — Repayment Schedule: The agreement specifies the duration of the credit, including the start and end dates, as well as the repayment schedule. It may include details such as the number of installments, due dates, and payment methods. — Default and Remedies: This section outlines the actions that can be taken by the lender in case of default by the borrower. It may include penalties, late payment fees, and the lender's right to pursue legal remedies, such as filing a lawsuit or initiating collection proceedings. — Governing Law: The Alabama Credit Agreement is subject to the laws of the state of Alabama, ensuring compliance with the state's regulations pertaining to credit agreements. — Dispute Resolution: The agreement may include a provision specifying how any disputes arising from the agreement will be resolved. This can include mediation, arbitration, or litigation in the appropriate courts. In conclusion, the Alabama Credit Agreement regarding extension of credit is a crucial legal document that outlines the terms and conditions under which credit is provided in Alabama. Understanding the different types of agreements and the key components of the contract is essential for both lenders and borrowers to ensure a smooth credit relationship.

Alabama Credit Agreement regarding extension of credit

Description

How to fill out Alabama Credit Agreement Regarding Extension Of Credit?

Are you inside a placement where you require papers for either organization or specific reasons almost every day time? There are tons of authorized papers themes available online, but finding versions you can rely isn`t straightforward. US Legal Forms provides a large number of develop themes, such as the Alabama Credit Agreement regarding extension of credit, that are composed to satisfy state and federal needs.

Should you be previously familiar with US Legal Forms internet site and get your account, merely log in. Following that, it is possible to obtain the Alabama Credit Agreement regarding extension of credit template.

Unless you provide an accounts and wish to start using US Legal Forms, abide by these steps:

- Discover the develop you need and make sure it is for your appropriate city/county.

- Take advantage of the Preview button to review the form.

- Browse the information to ensure that you have selected the correct develop.

- When the develop isn`t what you`re trying to find, take advantage of the Research area to obtain the develop that suits you and needs.

- Once you discover the appropriate develop, click Purchase now.

- Opt for the pricing strategy you need, complete the required details to generate your money, and pay money for the transaction making use of your PayPal or bank card.

- Choose a hassle-free file structure and obtain your version.

Find all the papers themes you possess purchased in the My Forms menus. You can get a additional version of Alabama Credit Agreement regarding extension of credit whenever, if needed. Just select the essential develop to obtain or print out the papers template.

Use US Legal Forms, probably the most extensive selection of authorized forms, to save lots of some time and steer clear of blunders. The support provides appropriately made authorized papers themes which can be used for a selection of reasons. Generate your account on US Legal Forms and commence producing your lifestyle a little easier.