Alabama Clauses Relating to Capital Withdrawals, Interest on Capital

Description

How to fill out Clauses Relating To Capital Withdrawals, Interest On Capital?

Have you been inside a situation that you will need papers for possibly organization or person uses nearly every day? There are a lot of lawful file web templates available on the net, but locating kinds you can rely isn`t easy. US Legal Forms provides thousands of form web templates, such as the Alabama Clauses Relating to Capital Withdrawals, Interest on Capital, that are published in order to meet state and federal needs.

When you are currently acquainted with US Legal Forms site and have your account, basically log in. Afterward, you can acquire the Alabama Clauses Relating to Capital Withdrawals, Interest on Capital design.

If you do not have an accounts and would like to begin to use US Legal Forms, abide by these steps:

- Discover the form you will need and ensure it is for the correct city/area.

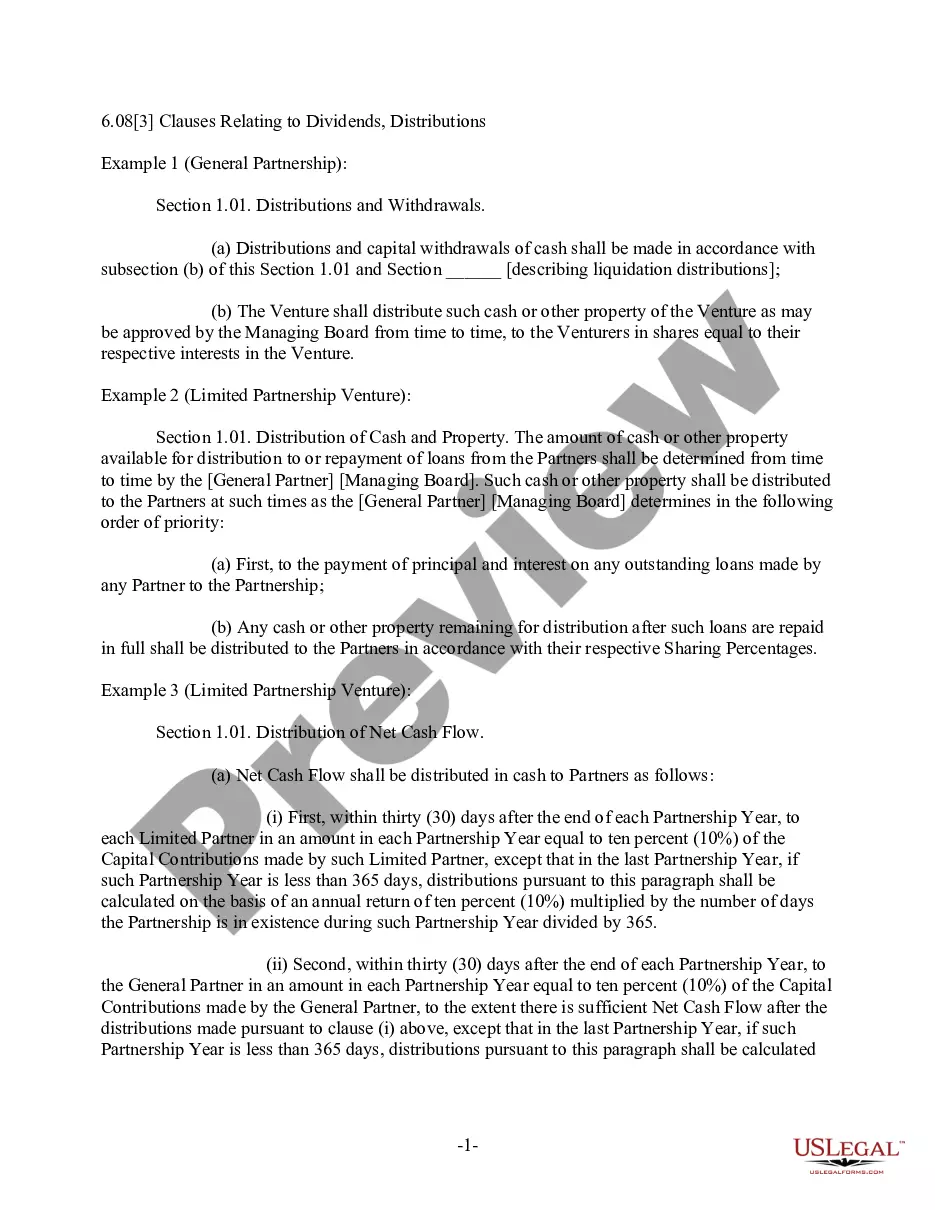

- Make use of the Review button to examine the shape.

- Read the information to actually have chosen the correct form.

- In case the form isn`t what you`re looking for, use the Look for industry to get the form that suits you and needs.

- When you discover the correct form, simply click Purchase now.

- Pick the pricing prepare you would like, fill out the desired info to generate your money, and purchase your order with your PayPal or credit card.

- Select a hassle-free data file file format and acquire your version.

Discover all of the file web templates you may have purchased in the My Forms menu. You can obtain a extra version of Alabama Clauses Relating to Capital Withdrawals, Interest on Capital anytime, if needed. Just click the necessary form to acquire or printing the file design.

Use US Legal Forms, by far the most comprehensive selection of lawful forms, to save some time and stay away from errors. The support provides skillfully produced lawful file web templates that you can use for an array of uses. Make your account on US Legal Forms and begin creating your lifestyle a little easier.

Form popularity

FAQ

Municipal Exemptions Section 40-23-4(11) and 40-23-4(15) exempt municipalities from payment of sales and use taxes. Additionally, municipalities and their instrumentalities, except for certain educational facilities, are not required to collect sales and use taxes on items they sell. See, Regulation 810-6-2-. 92.02.

Sales of automobiles, motorcycles, trucks, truck trailers, or semitrailers that will be registered or titled outside Alabama, that are exported or removed from Alabama within 72 hours by the purchaser or his or her agent for first use outside Alabama are not subject to the Alabama sales tax.

(c) An excise tax is hereby imposed on the storage, use or other consumption in this state of any automotive vehicle or truck trailer, semitrailer or house trailer, and mobile home set-up materials and supplies including but not limited to steps, blocks, anchoring, cable pipes and any other materials pertaining thereto ...

Sales to Exempt Organizations ? Sales made directly to the federal government, the state of Alabama and counties and cities within the state; sales made directly to schools (not daycares) within the state; sales made to city- and county-owned and operated hospitals and nursing homes; sales made to some nonprofit ...

09. Section 810-6-5-. 09 - Leasing and Rental of Tangible Personal Property (1) The term "rental tax" as used in this rule shall mean the privilege or license tax levied in Section 40-12-222, Code of Ala.

Alabama allows an exemption on the furnishing of electricity to a manufacturer or compounder for use in an electrolytic or electrothermal manufacturing or compounding process, natural gas which becomes a component of tangible personal property manufactured or compounded (but not used as fuel or energy), and natural gas ...

Any person or company that fails to obtain or renew a certificate of exemption prior to its expiration may not make tax exempt purchases or rent tax exempt accommodations after the expiration.

If any person liable to pay any final assessment of tax neglects or refuses to pay the same or fails to appeal such final assessment within 30 days, it shall be lawful for the commissioner to collect such tax (and such further sum as shall be sufficient to cover the expenses of the levy) as herein provided or as ...