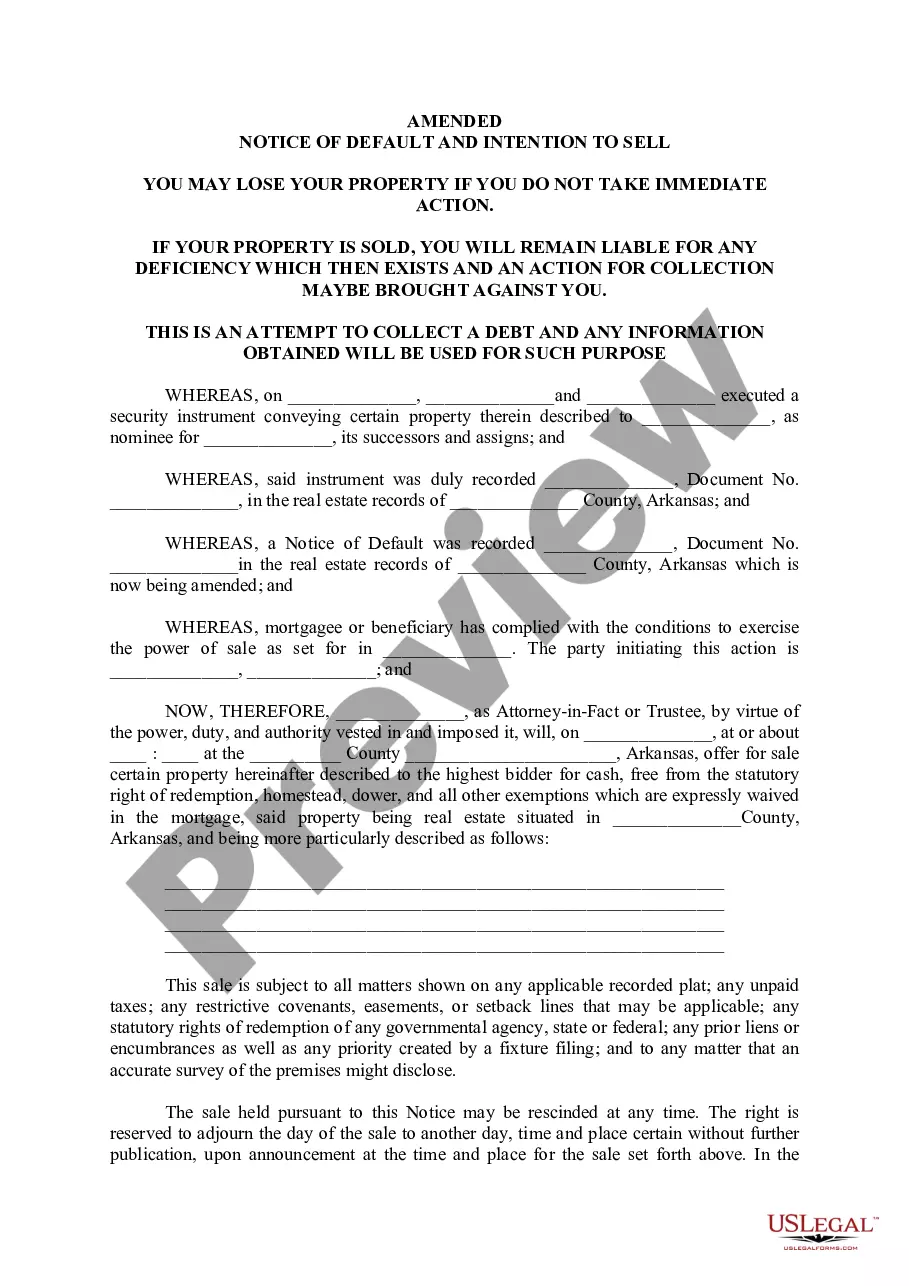

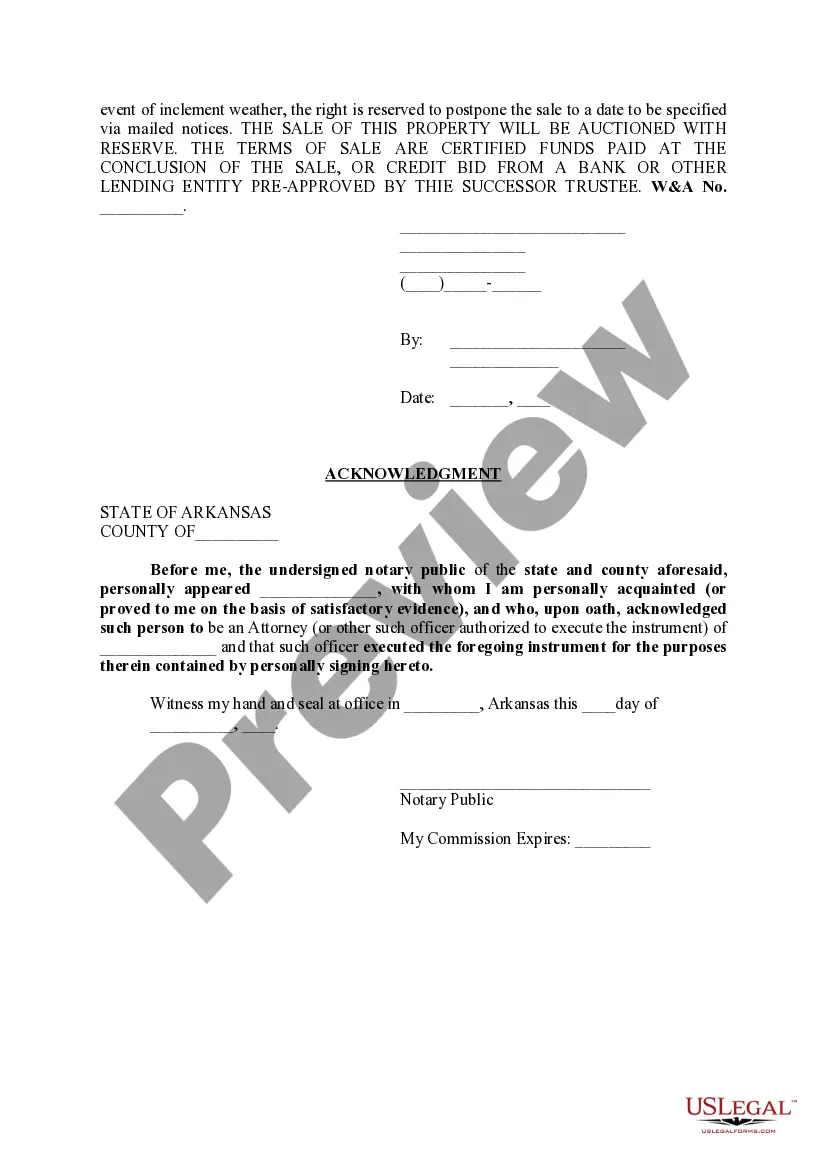

Arkansas Amended Notice of Default and Intention to Sell

Description

How to fill out Arkansas Amended Notice Of Default And Intention To Sell?

Using the Arkansas Revised Notification of Default and examples crafted by experienced attorneys helps you avoid hassles when completing paperwork.

Simply download the template from our site, fill it in, and seek legal advice to review it.

By doing this, you can save significantly more time and energy than asking a lawyer to create a document entirely from the beginning for you.

Make use of the Preview feature and check the description (if available) to confirm if you need this particular template; if yes, click Buy Now.

- If you already have a US Legal Forms membership, just Log In/">Log In to your account and navigate back to the form page.

- Locate the Download button next to the forms you are reviewing.

- After downloading a document, you will find all your saved templates in the My documents section.

- If you do not have a subscription, it’s not a major issue.

- Just follow the steps below to register for an online account, obtain, and complete your Arkansas Revised Notification of Default and template.

- Ensure you are downloading the correct state-specific form.

Form popularity

FAQ

In Arkansas, lenders may foreclose on deeds of trusts or mortgages in default using either a judicial or non-judicial foreclosure process. However, an appraisal of the property must be made prior to the schedule date of foreclosure.

Write to the agency making the claim. Present evidence of why the NOD was improperly issued or why you legitimately cannot make payments. Ask the agency in the letter if they will take a lower monthly payment, total settlement or a payment plan. Send a copy of your letter by certified mail.

A notice of default is the first step to a bank or mortgage lender's foreclosure process.If the mortgage is not paid up to date, the lender will seize the home. A notice of default is also known as a reinstatement period, notice of public auction, or notice of foreclosure.

After you've received a Notice of Default, you have 3 months in which to attempt to get your loan current. As mentioned above, that means paying all back payments, interest, fees, property taxes, and insurance. After 3 months, the bank can officially set a date for the auction of your home.

A notice of default is the first step to a bank or mortgage lender's foreclosure process.If the mortgage is not paid up to date, the lender will seize the home. A notice of default is also known as a reinstatement period, notice of public auction, or notice of foreclosure.

The foreclosure process is defined by California civil code 2924 and begins with the filing of a Notice of Default (NOD) with the county recorder. Once a borrower is at least 90 days behind in making mortgage payments, the lender will file a Notice of Default with the court of the county where the property is located.

The notice of default doesn't affect your credit file, but when the account defaults this will be recorded.If the debt is regulated by the Consumer Credit Act, you must be sent a default notice warning letter and have time to act on it before the default is recorded on your credit file.

After the lender files the Notice of Default, you get 90 days to bring your past-due bill current. After the 90 days pass, the lender files a Notice of Sale with the clerk. The Notice of Sale displays the location, date and time of the sale. It lists the trustee's name and contact information.