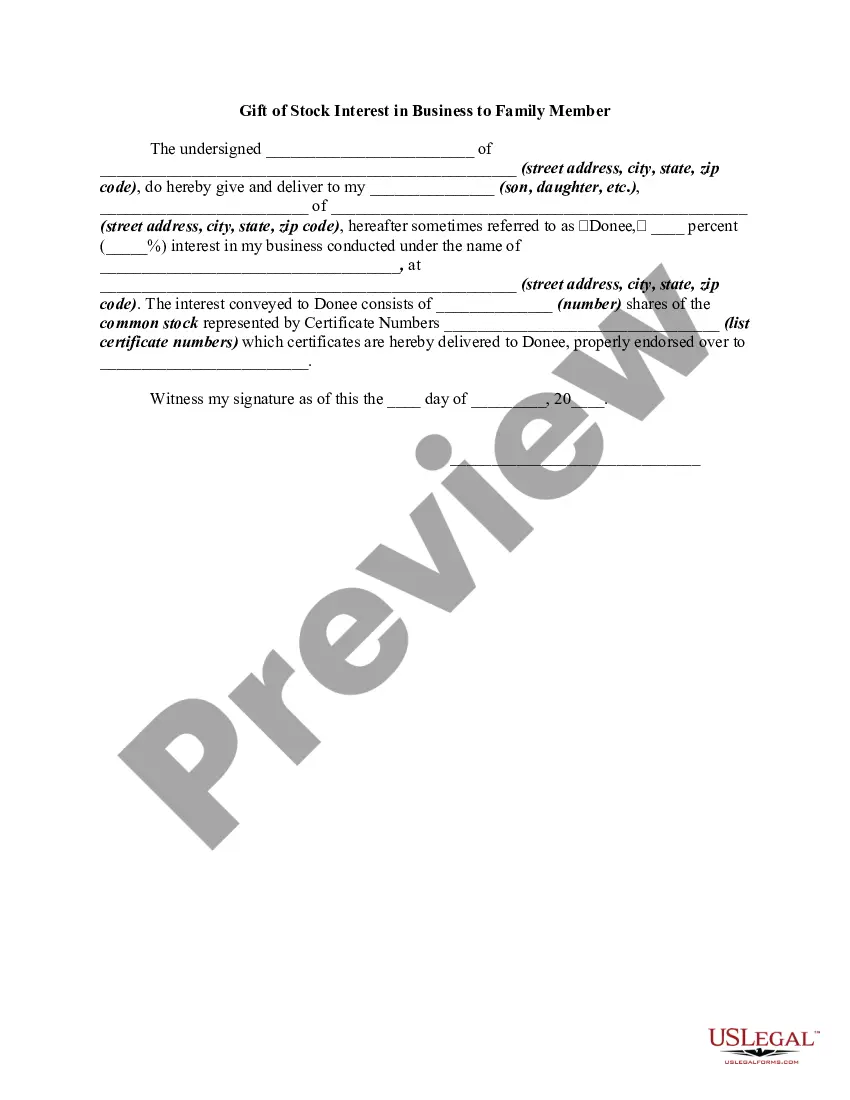

- passing of title;

- made with the intent to pass title;

- without receiving money or value in consideration for the passing of title.

The following form is a gift to a family member of stock in a business owned by the donor.

Arkansas Gift of Stock Interest in Business to Family Member refers to the act of transferring ownership or shares of a business to a family member as a gift. This process involves giving away stock or equity in a business entity to a relative or spouse without any monetary exchange or consideration. This type of gift holds significance both for estate planning purposes and the continuation of a family business. There are several types of Arkansas Gift of Stock Interest in Business to Family Member, including: 1. Direct Gift: This type of gift involves transferring the stock interest directly to the family member without any intermediaries or complex arrangements. It requires legal documentation and compliance with state laws. 2. Indirect Gift: In some cases, the gift may be made indirectly by creating a trust or using a holding entity such as a limited liability company (LLC) or a partnership. This allows for more flexibility and control over the stock interest being transferred. 3. Minority Interest Gift: It is possible to gift a minority interest in the business, meaning the family member receives less than 50% ownership. This type of gift may limit the recipient's decision-making power and voting rights within the business. 4. Majority Interest Gift: The owner can also gift a majority interest in the business, transferring control and decision-making authority to the family member. This type of gift is common when passing on a family business to the next generation. When conducting an Arkansas Gift of Stock Interest in Business to a Family Member, it is essential to follow specific legal requirements. These may include drafting a stock transfer agreement, obtaining any necessary approvals from other shareholders or stakeholders, and complying with state and federal tax laws. The gift can have various purposes, such as estate planning to reduce the owner's taxable estate or transferring the business to a capable family member who wishes to take over its operations. It also allows for the preservation and continuation of a family legacy for future generations. Overall, an Arkansas Gift of Stock Interest in Business to a Family Member provides a way to transfer ownership in a business to a family member without a monetary exchange, enabling the family business to thrive and pass on the benefits to the next generation.