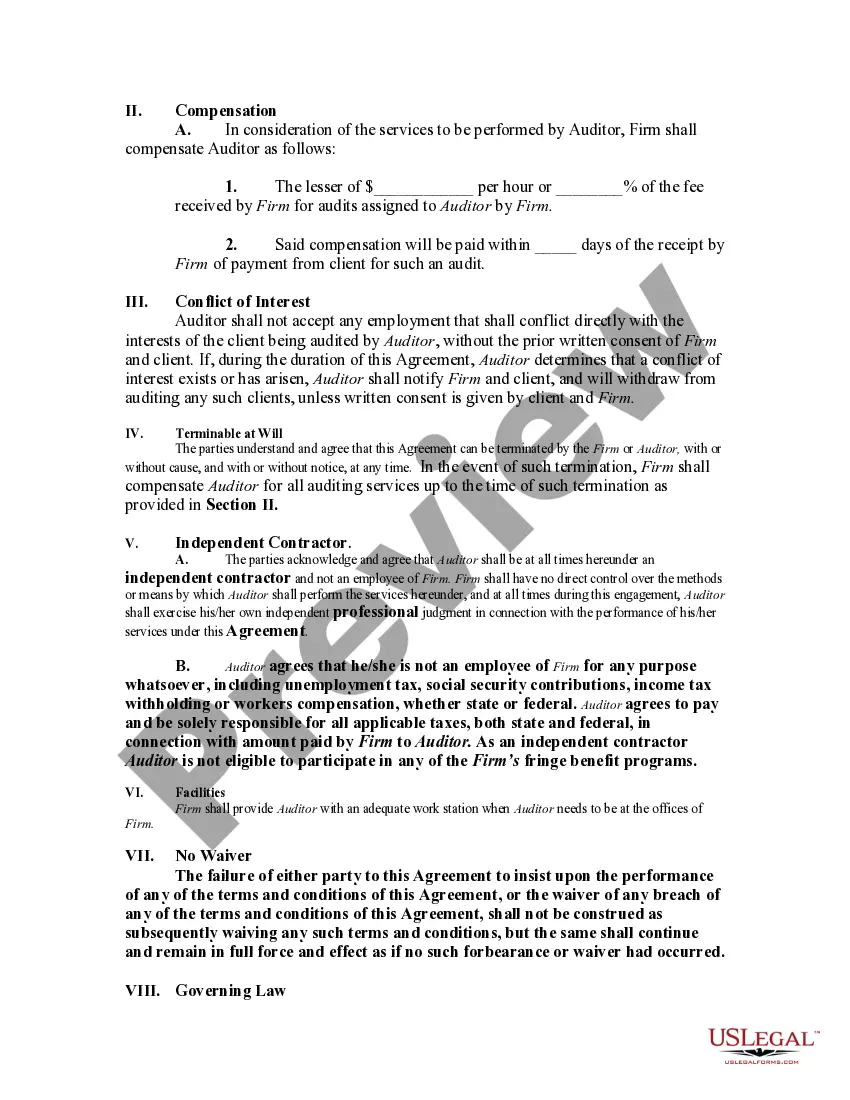

Although no definite rule exists for determining whether one is an independent contractor or an employee, certain indicia of the status of an independent contractor are recognized, and the insertion of provisions embodying these indicia in the contract will help to insure that the relationship reflects the intention of the parties. These indicia generally relate to the basic issue of control. The general test of what constitutes an independent contractor relationship involves which party has the right to direct what is to be done, and how and when. Another important test involves the method of payment of the contractor.

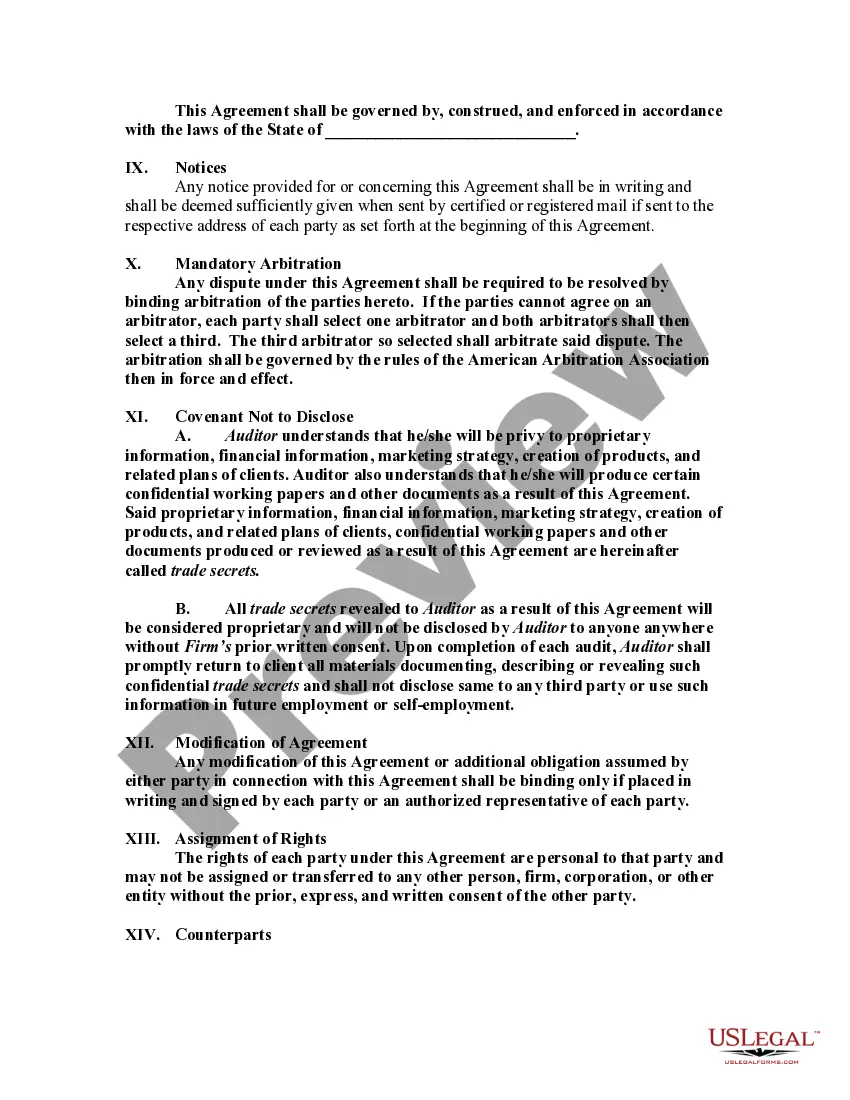

Title: Arkansas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: Exploring its Types and Importance Introduction: In the realm of accounting, businesses often hire auditors as self-employed independent contractors to ensure financial accuracy and compliance. The state of Arkansas recognizes this practice and offers an Arkansas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor. This detailed description will delve into the various types of such agreements and shed light on their significance for accounting firms and auditors alike. Types of Arkansas Agreements by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. General Arkansas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: This type of agreement serves as a basic framework, outlining the relationship between an accounting firm and an auditor working as a self-employed contractor within Arkansas. It encompasses key terms and conditions, responsibilities, compensation, and other important contractual aspects. 2. Arkansas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor with Non-Disclosure Clause: Where additional confidentiality measures are required, accounting firms may opt for this agreement type. Alongside the standard terms, it includes a comprehensive non-disclosure clause, safeguarding sensitive financial information and trade secrets of the firm and its clients. 3. Arkansas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor with Non-Compete Clause: To protect their business interests, accounting firms may utilize this agreement type. In addition to the regular provisions, it contains a non-compete clause, which restricts the auditor's ability to work for direct competitors within a specified geographical area for a given period after contract termination. Importance of Arkansas Agreements by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. Legal Clarity and Compliance: These agreements establish a solid legal foundation for the working relationship between an accounting firm and its auditor. They ensure compliance with federal and state laws governing independent contractors, thus reducing the risk of potential legal disputes or misclassification claims. 2. Clearly Defined Roles and Responsibilities: By outlining specific duties and responsibilities, these agreements eliminate confusion regarding the scope of work. They establish expectations on deliverables, working hours, and reporting mechanisms, ensuring a smooth workflow between the accounting firm and the auditor. 3. Protection of Intellectual Property and Confidentiality: With the inclusion of non-disclosure clauses, these agreements safeguard the confidentiality of sensitive financial information, proprietary data, and trade secrets, preventing unauthorized use or disclosure, and maintaining the integrity of the accounting firm's operations. 4. Mitigation of Liability Risks: These agreements may include clauses that allocate liability and indemnify parties involved, protecting the accounting firm from potential financial losses resulting from auditing errors or non-compliance issues. Conclusion: Utilizing an Arkansas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is crucial for both accounting firms and auditors operating within the state. Whether in its general form or enhanced with non-disclosure or non-compete clauses, these agreements provide legal clarity, define roles and responsibilities, protect intellectual property, and mitigate liability risks. By having a strong contractual foundation, accounting firms and auditors can establish mutually beneficial relationships that promote professionalism, accuracy, and adherence to legal and ethical standards within the accounting industry.Title: Arkansas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: Exploring its Types and Importance Introduction: In the realm of accounting, businesses often hire auditors as self-employed independent contractors to ensure financial accuracy and compliance. The state of Arkansas recognizes this practice and offers an Arkansas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor. This detailed description will delve into the various types of such agreements and shed light on their significance for accounting firms and auditors alike. Types of Arkansas Agreements by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. General Arkansas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: This type of agreement serves as a basic framework, outlining the relationship between an accounting firm and an auditor working as a self-employed contractor within Arkansas. It encompasses key terms and conditions, responsibilities, compensation, and other important contractual aspects. 2. Arkansas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor with Non-Disclosure Clause: Where additional confidentiality measures are required, accounting firms may opt for this agreement type. Alongside the standard terms, it includes a comprehensive non-disclosure clause, safeguarding sensitive financial information and trade secrets of the firm and its clients. 3. Arkansas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor with Non-Compete Clause: To protect their business interests, accounting firms may utilize this agreement type. In addition to the regular provisions, it contains a non-compete clause, which restricts the auditor's ability to work for direct competitors within a specified geographical area for a given period after contract termination. Importance of Arkansas Agreements by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor: 1. Legal Clarity and Compliance: These agreements establish a solid legal foundation for the working relationship between an accounting firm and its auditor. They ensure compliance with federal and state laws governing independent contractors, thus reducing the risk of potential legal disputes or misclassification claims. 2. Clearly Defined Roles and Responsibilities: By outlining specific duties and responsibilities, these agreements eliminate confusion regarding the scope of work. They establish expectations on deliverables, working hours, and reporting mechanisms, ensuring a smooth workflow between the accounting firm and the auditor. 3. Protection of Intellectual Property and Confidentiality: With the inclusion of non-disclosure clauses, these agreements safeguard the confidentiality of sensitive financial information, proprietary data, and trade secrets, preventing unauthorized use or disclosure, and maintaining the integrity of the accounting firm's operations. 4. Mitigation of Liability Risks: These agreements may include clauses that allocate liability and indemnify parties involved, protecting the accounting firm from potential financial losses resulting from auditing errors or non-compliance issues. Conclusion: Utilizing an Arkansas Agreement by Accounting Firm to Employ Auditor as Self-Employed Independent Contractor is crucial for both accounting firms and auditors operating within the state. Whether in its general form or enhanced with non-disclosure or non-compete clauses, these agreements provide legal clarity, define roles and responsibilities, protect intellectual property, and mitigate liability risks. By having a strong contractual foundation, accounting firms and auditors can establish mutually beneficial relationships that promote professionalism, accuracy, and adherence to legal and ethical standards within the accounting industry.