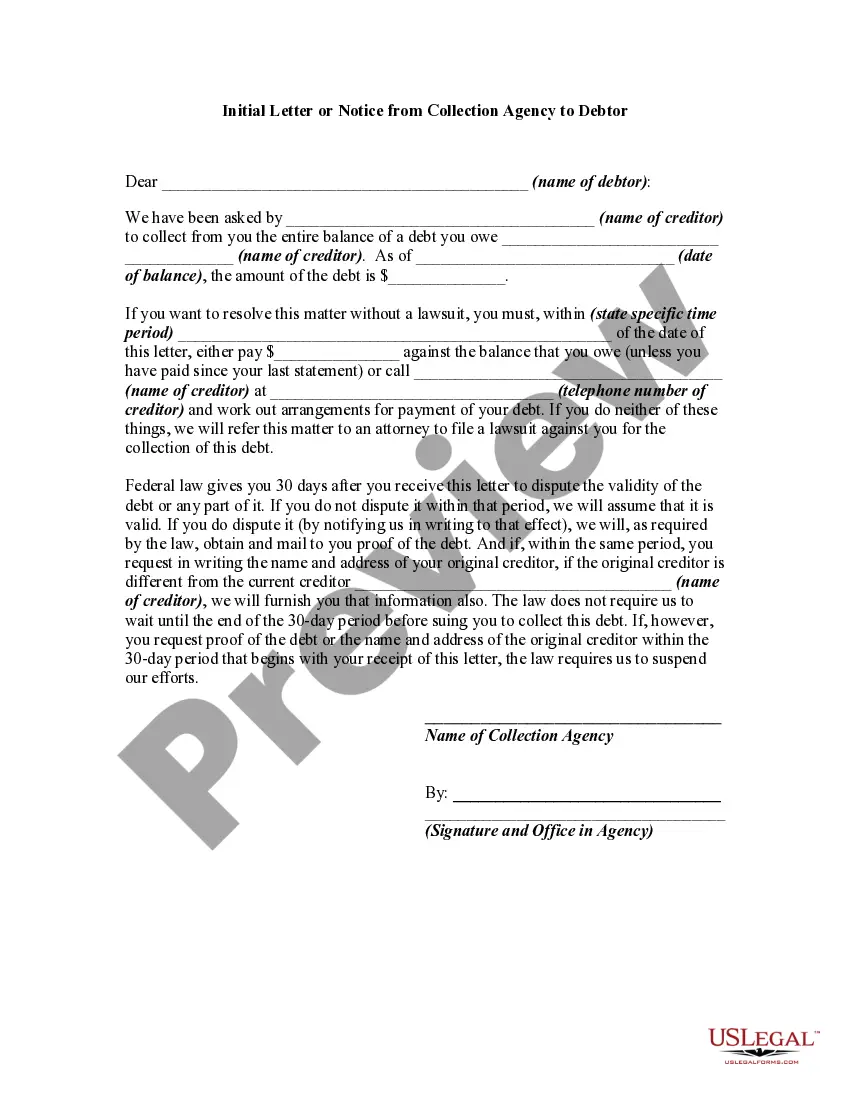

The Fair Debt Collection Practices Act (FDCPA) prohibits harassment or abuse in collecting a debt such as threatening violence, use of obscene or profane language, publishing lists of debtors who refuse to pay debts, or even harassing a debtor by repeatedly calling the debtor on the phone. Also, certain false or misleading representa?¬tions are forbidden, such as representing that the debt collector is associated with the state or federal government, or stating that the debtor will go to jail if he does not pay the debt. This Act also sets out strict rules regarding communicating with the debtor.

The FDCPA applies only to those who regularly engage in the business of collecting debts for others -- primarily to collection agencies. The Act does not apply when a creditor attempts to collect debts owed to it by directly contacting the debtors. It applies only to the collection of consumer debts and does not apply to the collection of commercial debts. Consumer debts are debts for personal, home, or family purposes.

In Arkansas, an Initial Letter or Notice from a Collection Agency to a Debtor serves as a formal communication sent by a collection agency to inform the debtor about an outstanding debt and their rights and obligations regarding such debt. This letter initiates the collection process and aims to establish communication between the debtor and the collection agency. Here are some types of Initial Letters or Notices commonly used by collection agencies in Arkansas: 1. Standard Initial Notice: This is a general letter sent to inform the debtor of the existence of a delinquent account and the need to resolve the outstanding balance. It includes information such as the creditor's name, the estimated amount owed, the current status of the debt, and various contact options to discuss repayment arrangements or dispute the debt. 2. Validation of Debt Notice: As per federal law (Fair Debt Collection Practices Act or FD CPA), this type of letter is sent to the debtor within five days of the initial communication. It provides detailed information about the debt, including the original creditor's name, the amount owed, and instructions on how the debtor can verify or challenge the debt's validity. This notice also highlights the debtor's rights to request additional information and clarifications. 3. Notice of Intent to Sue: When a debtor fails to respond to the initial notices or fails to arrange repayment, a collection agency may issue a Notice of Intent to Sue. This letter alerts the debtor that legal action may be pursued if the debt remains unresolved. It typically includes details about potential consequences, such as wage garnishment, bank account freeze, or property liens. 4. Cease and Desist Letter: Occasionally, debtors may dispute the validity of a debt or request the collection agency to cease further communication. In response, collection agencies may send a Cease and Desist Letter. This letter acknowledges the debtor's request and confirms that no further collection efforts will be made, except for specific legal actions like filing a lawsuit. Arkansas' law requires that these letters follow certain guidelines and include specific information as outlined in the Arkansas Fair Debt Collection Practices Act (AFD CPA) and other relevant federal regulations. Collection agencies must ensure compliance with these laws to protect the debtor's rights and maintain ethical practices in debt collection.