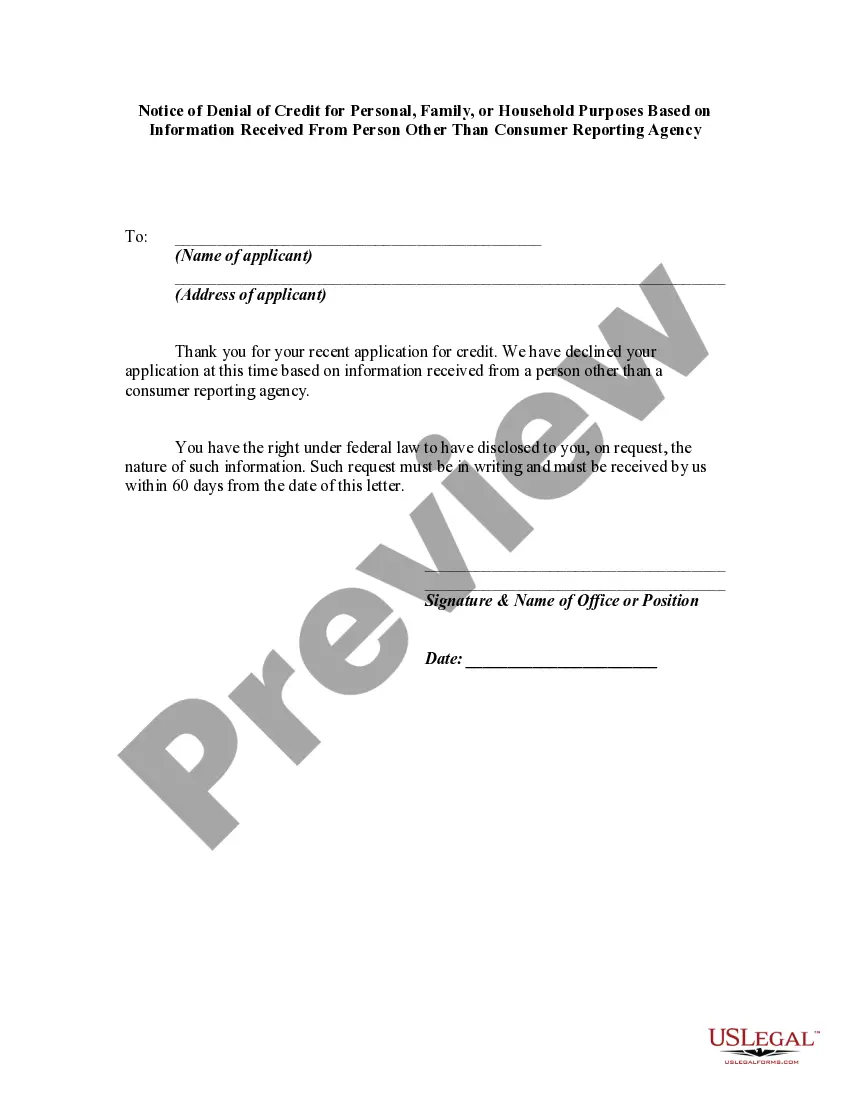

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information.

Arkansas Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency In Arkansas, consumers have certain rights and protections when it comes to obtaining credit for personal, family, or household purposes. One such protection is the requirement for lenders to provide a Notice of Denial of Credit based on information received from a person other than a consumer reporting agency. This notice serves as a means of informing the consumer of the reasons for their credit denial and provides necessary information for the consumer to understand why credit was not granted. Here are a few types of Arkansas Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency: 1. Standard Denial Notice: This notice is typically issued by lenders when they have received information that negates the consumer's eligibility for credit. It should include a detailed explanation of the reason(s) for the denial, such as negative references from personal or professional contacts, adverse financial information, or employment-related issues. 2. Incomplete Application Notice: If a consumer fails to provide all required information on their credit application, lenders may issue an incomplete application notice. This notice should outline the specific details that were missing or incomplete, leading to the denial of credit. 3. Unverifiable Information Notice: In some cases, lenders may be unable to verify the accuracy of the information provided by the consumer. This type of notice should explain the specific information that couldn't be verified and how it impacted the lender's decision to deny credit. 4. Fraud-Related Denial Notice: If the lender suspects fraudulent activity or a potential identity theft issue, they may issue a denial notice based on this concern. This notice should clearly state that the denial is due to suspected fraud and provide guidance on how the consumer can address the matter. These notice types aim to ensure transparency and fairness in the credit process, allowing consumers the opportunity to address any inaccuracies or issues that may have contributed to the denial. It's vital for consumers to carefully review the notice, understand the reasons for denial, and take appropriate action to rectify any incorrect information or improve their creditworthiness for future applications. Note: It's important to consult official sources or legal advisors to ensure accuracy and up-to-date information regarding Arkansas Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency.Arkansas Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency In Arkansas, consumers have certain rights and protections when it comes to obtaining credit for personal, family, or household purposes. One such protection is the requirement for lenders to provide a Notice of Denial of Credit based on information received from a person other than a consumer reporting agency. This notice serves as a means of informing the consumer of the reasons for their credit denial and provides necessary information for the consumer to understand why credit was not granted. Here are a few types of Arkansas Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency: 1. Standard Denial Notice: This notice is typically issued by lenders when they have received information that negates the consumer's eligibility for credit. It should include a detailed explanation of the reason(s) for the denial, such as negative references from personal or professional contacts, adverse financial information, or employment-related issues. 2. Incomplete Application Notice: If a consumer fails to provide all required information on their credit application, lenders may issue an incomplete application notice. This notice should outline the specific details that were missing or incomplete, leading to the denial of credit. 3. Unverifiable Information Notice: In some cases, lenders may be unable to verify the accuracy of the information provided by the consumer. This type of notice should explain the specific information that couldn't be verified and how it impacted the lender's decision to deny credit. 4. Fraud-Related Denial Notice: If the lender suspects fraudulent activity or a potential identity theft issue, they may issue a denial notice based on this concern. This notice should clearly state that the denial is due to suspected fraud and provide guidance on how the consumer can address the matter. These notice types aim to ensure transparency and fairness in the credit process, allowing consumers the opportunity to address any inaccuracies or issues that may have contributed to the denial. It's vital for consumers to carefully review the notice, understand the reasons for denial, and take appropriate action to rectify any incorrect information or improve their creditworthiness for future applications. Note: It's important to consult official sources or legal advisors to ensure accuracy and up-to-date information regarding Arkansas Notice of Denial of Credit for Personal, Family, or Household Purposes Based on Information Received From Person Other Than Consumer Reporting Agency.