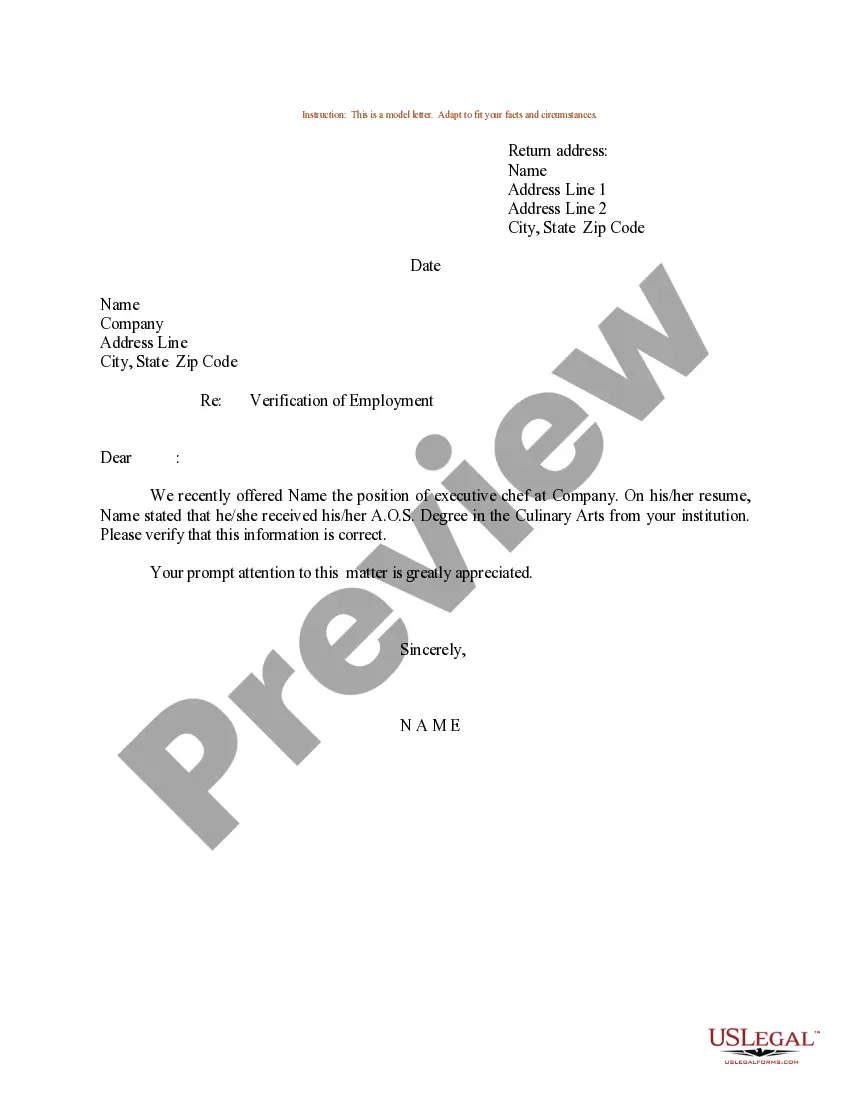

An Arkansas Employment Verification Letter for Mortgage is an official document that confirms an individual's employment status, income details, and other related information. This letter is commonly requested by mortgage lenders during the loan application process to verify the borrower's ability to repay the mortgage. The Arkansas Employment Verification Letter for Mortgage serves as evidence of a borrower's current employment and income level, providing the lender with confidence in the borrower's financial stability. This document is crucial for mortgage lenders to verify the borrower's ability to afford the loan, ensuring responsible lending practices. Keywords: Arkansas, Employment Verification Letter, Mortgage, detailed description, types of Arkansas Employment Verification Letters for Mortgage: 1. Standard Employment Verification Letter: This type of letter verifies the borrower's current employment details, including job title, employer name, employment start date, and regular income. It may also include information regarding the borrower's work schedule and employment status (full-time, part-time, contract). 2. Self-Employment Verification Letter: For self-employed individuals, this verification letter confirms the borrower's self-employment status, business name, type of business, and income details. It may require additional documentation, such as tax returns or profit and loss statements, to verify the borrower's income stability. 3. Additional Income Verification Letter: Sometimes, borrowers may have additional income sources apart from their primary employment. This verification letter is used to confirm any supplementary income, such as rental income, investment returns, or alimony. Lenders may require supporting documentation to verify the legitimacy and stability of these income sources. 4. Temporary Employment Verification Letter: In cases where the borrower is employed on a temporary or contract basis, lenders may require a specific verification letter that confirms the duration of employment, contract terms, and income stability during the loan term. This ensures that even with temporary employment, the borrower can afford the mortgage payments. 5. Pension or Retirement Verification Letter: For retirees or individuals receiving pension benefits, a verification letter is required to confirm the regular pension or retirement income. This letter typically includes details about the pension provider, amount of income, and recurrence. 6. Letter from Employer's HR Department: In some cases, lenders may require a verification letter issued directly by the borrower's employer's human resources (HR) department. This letter validates the borrower's employment details and income status, providing an authoritative confirmation of their financial stability. Overall, an Arkansas Employment Verification Letter for Mortgage is a vital document in the loan approval process. It ensures that borrowers' income claims are verified, minimizing the risk for lenders and promoting responsible lending practices.

Arkansas Employment Verification Letter for Mortgage

Description

How to fill out Arkansas Employment Verification Letter For Mortgage?

You may spend time online looking for the lawful papers template that suits the federal and state needs you want. US Legal Forms supplies thousands of lawful varieties that happen to be reviewed by experts. You can actually acquire or produce the Arkansas Employment Verification Letter for Mortgage from my support.

If you already have a US Legal Forms accounts, you can log in and then click the Down load switch. Afterward, you can comprehensive, modify, produce, or indication the Arkansas Employment Verification Letter for Mortgage. Every lawful papers template you purchase is your own property for a long time. To get another copy of any acquired form, check out the My Forms tab and then click the related switch.

If you work with the US Legal Forms website the first time, keep to the basic instructions under:

- Initial, ensure that you have chosen the right papers template for your state/metropolis of your choosing. Look at the form information to make sure you have selected the proper form. If accessible, utilize the Preview switch to appear from the papers template too.

- If you would like discover another edition of the form, utilize the Look for field to discover the template that meets your needs and needs.

- After you have discovered the template you would like, click Buy now to carry on.

- Select the prices program you would like, type your references, and register for your account on US Legal Forms.

- Comprehensive the transaction. You can use your credit card or PayPal accounts to pay for the lawful form.

- Select the file format of the papers and acquire it to your device.

- Make changes to your papers if required. You may comprehensive, modify and indication and produce Arkansas Employment Verification Letter for Mortgage.

Down load and produce thousands of papers templates while using US Legal Forms Internet site, which offers the most important selection of lawful varieties. Use professional and status-distinct templates to handle your company or personal demands.

Form popularity

FAQ

How To Write a Letter of Employment Employer Details. ... Details of the Organisation Requesting the Information. ... Necessary Information of the Employee. ... Stick to a Business Letter Format. ... Express the Purpose of Your Letter. ... Incorporate Details Requested by the Employee. ... Give Contact Details and Sign Off.

Here's how to write an employment verification letter, and the information to include: Employee name. Job title. Job description. Employment dates. Salary (current or past) Reason for termination (if applicable)

What should be included in employment verification letters? Employer address. Name and address of the company requesting verification. Employee name. Employment dates. Employee job title. Employee job description. Employee current salary. Reason for termination (If applicable)

All requests must be submitted in writing via US mail to the address below, via fax to 501.682. 6553 or via email to emp.verifications@dhs.arkansas.gov.

Employment Verification Request written verification be faxed to (916) 376-5393 or sent to DGS - HR, 7th Floor, P.O. Box 989052, MS 402, West Sacramento, CA 95798-9052. Information that can be provided includes: Dates of employment, Title (job classification), ... Written verification has a five-day turn-around.

Kristi Putnam serves as the Arkansas Department of Human Services (DHS) Secretary. She is responsible for leadership and oversight of the department's efforts, which support the health and well-being of all Arkansans, especially those who are most in need.

The DCO-702 is used by facilities to report to the DHS county office all Medicaid-related admissions, discharges, and transfers.

1-800 482-8988 or 501-682-8233 ? Available Monday-Friday 8- p.m. Call center hours are Monday through Friday 8 a.m. until 5 p.m.