In real estate, a short sale occurs when a bank or mortgage lender agrees to discount a loan balance due to an economic hardship on the part of the mortgagor (i.e., the seller). Circumstances determine whether or not banks will discount a loan balance. These circumstances are usually related to the current real estate market climate and the individual borrower's financial situation. A short sale typically is executed to prevent a home foreclosure. Often a bank will choose to allow a short sale if they believe that it will result in a smaller financial loss than foreclosing.

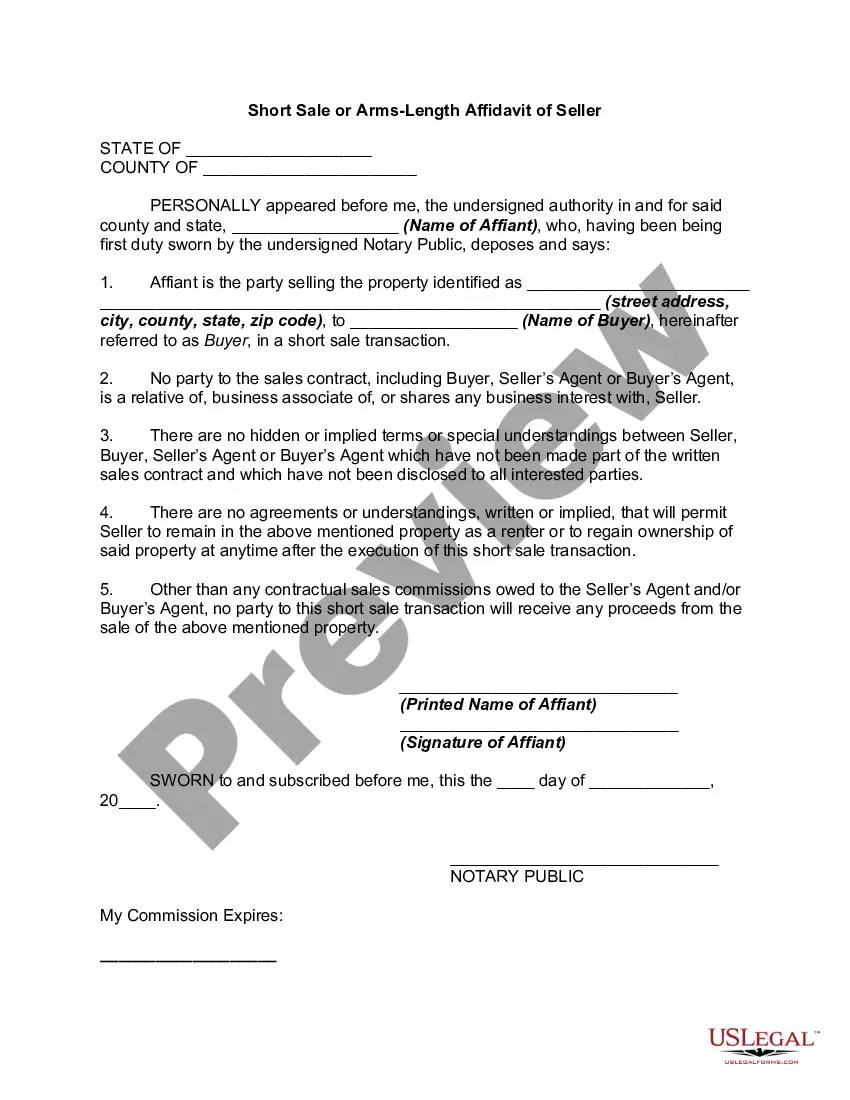

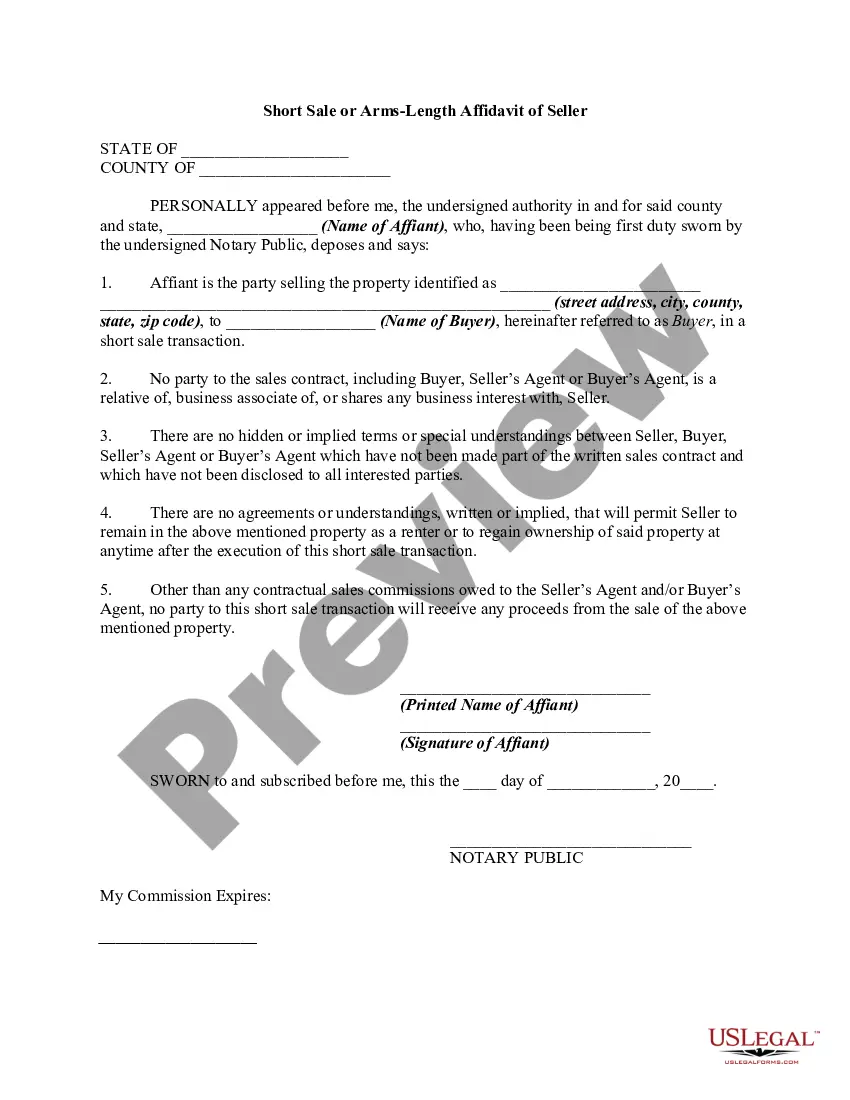

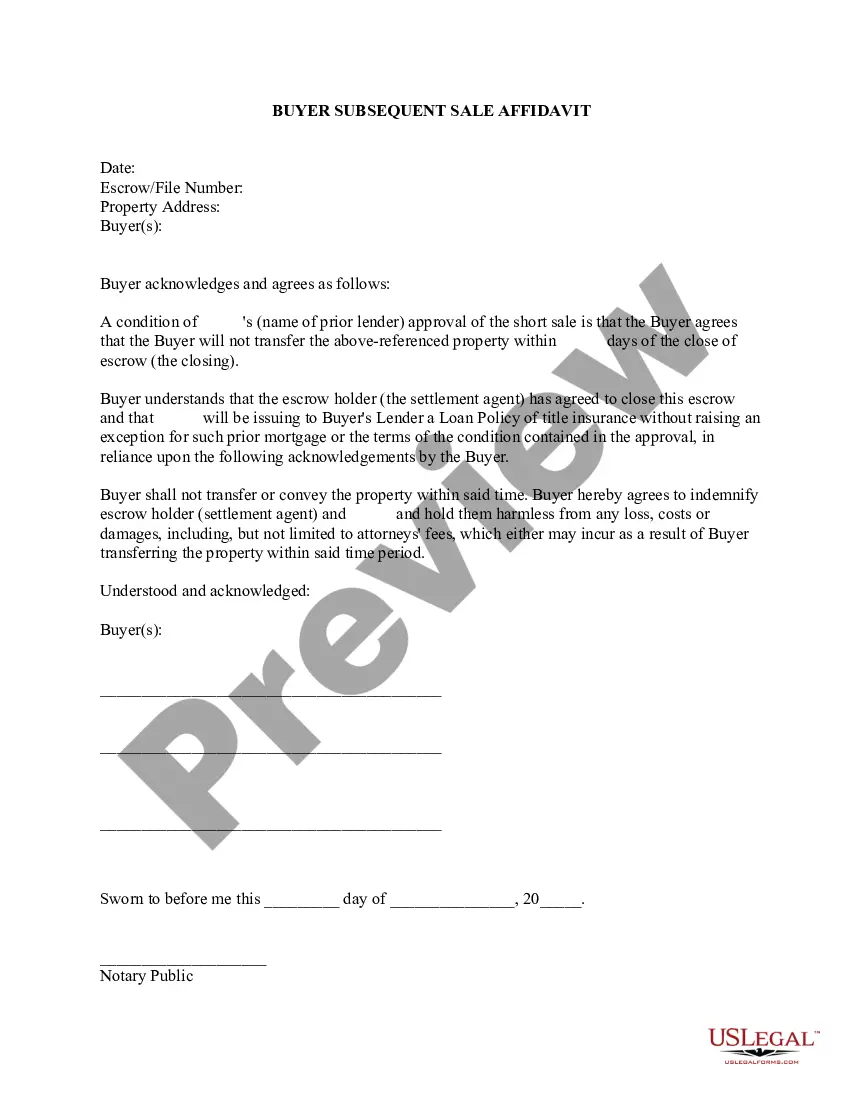

An arms-length or short sale affidavit is a document created by a bank in an attempt to prevent sellers from selling to relatives or friends to act as a straw buyer. Sometimes sellers make such side agreements. Then, after the transaction closes, the

pretend

buyers quickly transfer title back to the seller. This practice, in affect, means the sellers have repurchased their home at maybe half the cost, which greatly benefits those sellers.

Arkansas Short Sale Affidavit of Buyer

Instant download

Description

How to fill out Short Sale Affidavit Of Buyer?

US Legal Forms - one of the most important collections of legal documents in the United States - offers a broad selection of legal paperwork templates that you can download or print.

By using the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords.

You can obtain the latest versions of forms like the Arkansas Short Sale Affidavit of Buyer in just a few minutes.

Review the form summary to confirm that you have selected the right document.

If the form doesn't meet your requirements, use the Search box at the top of the page to find one that does.

- If you have a subscription, sign in and download the Arkansas Short Sale Affidavit of Buyer from the US Legal Forms catalog.

- The Download button will be visible on each template you review.

- You can access all previously downloaded forms from the My documents section of your account.

- If you're using US Legal Forms for the first time, here are simple steps to get started.

- Ensure you have selected the correct form for your locality/state.

- Click the Preview button to review the form's content.

Form popularity

FAQ

An affidavit on a bill of sale is a legal document that verifies the authenticity of the transaction involving the transfer of ownership. It serves as important proof in cases of dispute regarding the sale. When dealing with an Arkansas Short Sale Affidavit of Buyer, this document can provide assurance that all parties agree to the terms stated. Utilizing valid affidavits strengthens your legal standing in any transaction.

A short sale affidavit is a legal document that outlines the buyer's agreement and intentions in purchasing a short sale property. It confirms the buyer's understanding of the sale terms and can help protect both the buyer and the lender during the transaction. This document often includes essential information related to the Arkansas Short Sale Affidavit of Buyer, making it critical for anyone involved in a short sale. Utilizing legal resources, such as uslegalforms, can guide you in preparing this affidavit properly.

A short sale occurs when a homeowner sells their property for less than the amount owed on the mortgage. This process involves the lender approving the sale and agreeing to accept the lower amount, usually to avoid foreclosure. Buyers should expect several steps, including negotiations and paperwork, making it vital to understand the Arkansas Short Sale Affidavit of Buyer for a smoother transaction. Working with legal forms can simplify the documentation needed.

One significant downside of a short sale is the potential for longer processing times, as lenders may take their time reviewing offers. Additionally, properties sold through short sales may be sold 'as-is,' leading to unexpected repair costs. However, utilizing tools like the Arkansas Short Sale Affidavit of Buyer can simplify the process and minimize misunderstandings. Understanding these factors can help you make informed decisions.

A downside of a short sale is the potential for a lengthy process that can leave both buyers and sellers feeling frustrated. Not only does this involve negotiations with the lender, but it often requires additional paperwork, such as the Arkansas Short Sale Affidavit of Buyer. Additionally, a short sale may negatively impact the seller's credit score, although not as severely as a foreclosure. Understanding these drawbacks can help buyers and sellers navigate the process more effectively.

arm's length transaction may also involve underpaying for a property's assessed value. For example, a seller sells a house to their friend for less than what it is worth but with no intention to commit fraud.

Arm's length transactions are commonly required for short sales, which are an alternative to foreclosure. In a short sale, a lender allows a homeowner to sell their home to pay off their mortgage, even if the sale doesn't net enough to pay off the balance of the homeowner's mortgage.

An example of an arm's-length transaction is a home buyer and a stranger who's selling a house. Each is offering what the other wants, but neither has any obligation to the other. They can try to reach a deal that serves them both. The opposite of an arm's-length transaction is an arm-in-arm transaction.

A short sale is when a mortgage lender agrees to accept a mortgage payoff amount less than what is owed in order to facilitate a sale of the property by a financially distressed owner. The lender forgives the remaining balance of the loan.

A short sale is the sale of a real estate property for which the lender is willing to accept less than the amount still owed on the mortgage. For a sale to be considered a short sale, these two things must be true: The homeowner must be so far behind on payments that they can't catch up.