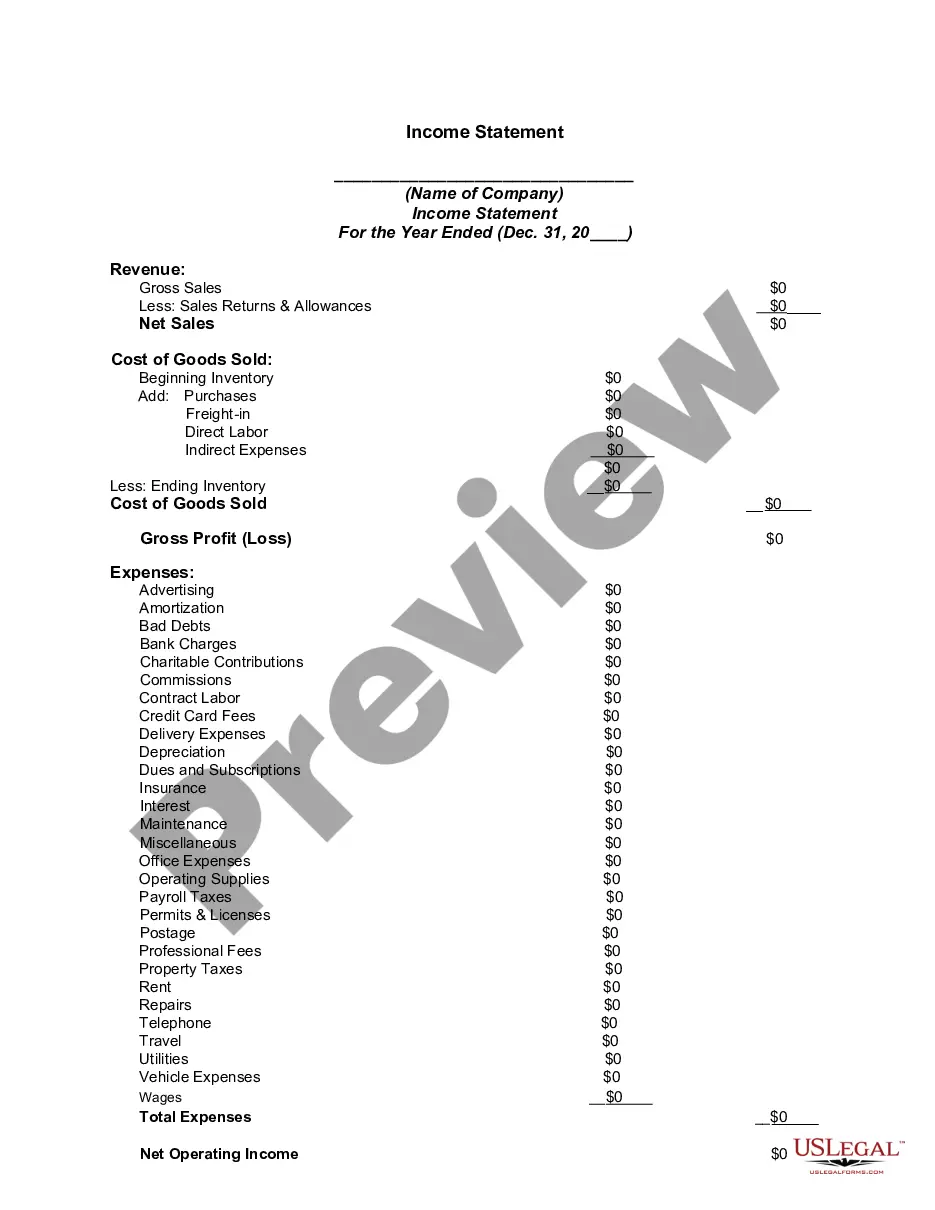

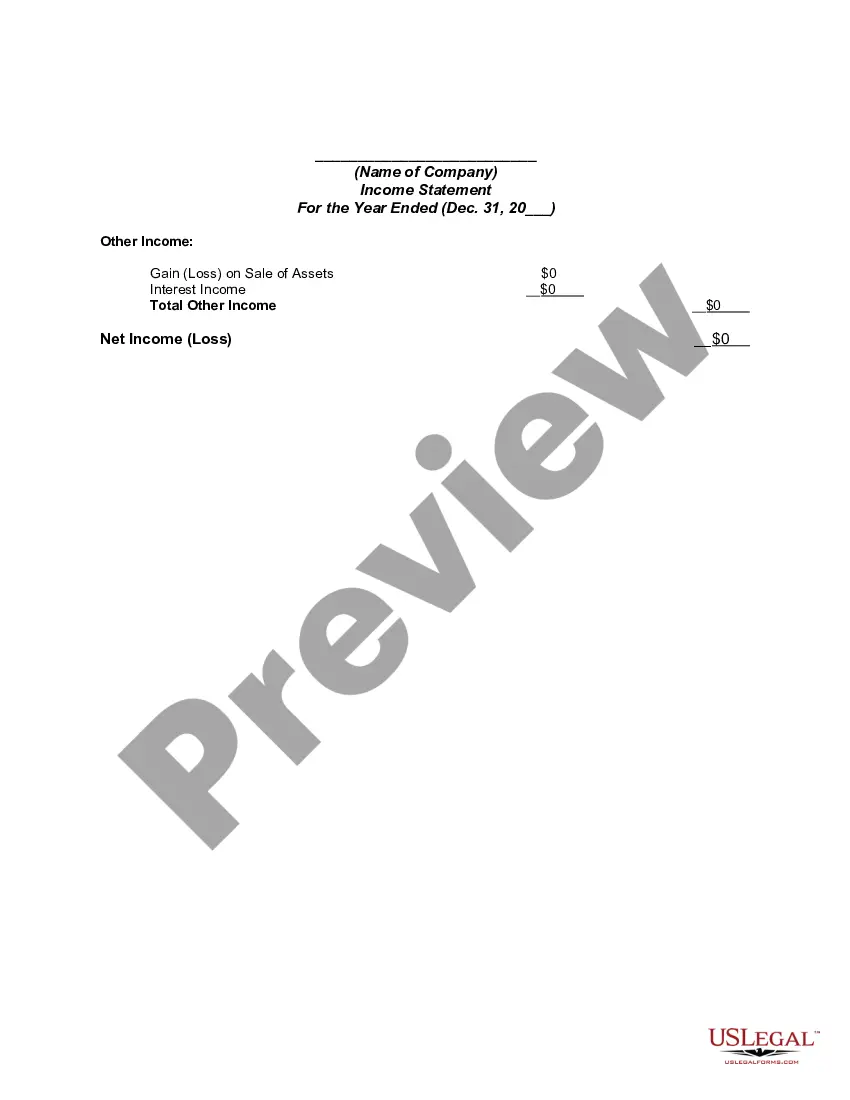

An income statement (sometimes called a profit and loss statement) lists your revenues and expenses, and tells you the profit or loss of your business for a given period of time. You can use this income statement form as a starting point to create one yourself.

The Arkansas Income Statement is a financial document that provides a detailed overview of the revenue, expenses, and net income of an individual or business entity in the state of Arkansas. It serves as a valuable tool in assessing the financial health and profitability of an organization by providing key information about its operational performance. Keywords: Arkansas, income statement, financial document, revenue, expenses, net income, financial health, profitability, operational performance. The income statement in Arkansas follows a standardized format adhering to Generally Accepted Accounting Principles (GAAP). It consists of several sections that provide a comprehensive picture of the financial performance. The primary components of the Arkansas Income Statement include: 1. Revenue: This section lists all the income generated by the entity during a specific accounting period. It encompasses sources such as sales revenue, service fees, rental income, interest income, and gains from investments or asset sales. 2. Cost of Goods Sold (COGS): In this section, the direct expenses associated with producing or acquiring the products or services sold by the entity are detailed. This may include the costs of raw materials, direct labor, manufacturing overhead, or inventory purchases. 3. Gross Profit: Gross profit is calculated by deducting the COGS from the total revenue. It represents the amount of money left after accounting for the direct costs of goods or services, providing an initial indication of profitability. 4. Operating Expenses: This section includes all the expenses incurred while conducting day-to-day operations. They consist of selling, general, and administrative expenses (SGA), research and development costs, marketing expenses, payroll expenses, rent, utilities, and other overheads. 5. Operating Income: Operating income is derived by subtracting the operating expenses from the gross profit. It reflects the profitability of the core business operations of the entity, excluding other non-operational factors. 6. Non-Operating Income and Expenses: This section accounts for income and expenses not directly related to core operations, usually including interest income, interest expenses, gains or losses from investments, and any extraordinary items. 7. Net Income: Net income, also known as the bottom line, is calculated by subtracting non-operating income and expenses from the operating income. It represents the final profit or loss earned during the accounting period, demonstrating the overall performance of the entity. Different types of Arkansas Income Statements may exist based on the organization's legal structure or reporting requirements. These can include income statements applicable to sole proprietorship, partnerships, corporations, or nonprofit entities. However, all variations serve the same purpose of presenting an accurate picture of financial performance. In conclusion, the Arkansas Income Statement is a crucial financial document that reflects the revenue, expenses, and net income of an individual or business in the state. It provides stakeholders with essential information to assess financial health, profitability, and operational efficiency. By analyzing the components of the income statement, one can gain insights into the financial performance of the organization and make informed decisions regarding its financial affairs.The Arkansas Income Statement is a financial document that provides a detailed overview of the revenue, expenses, and net income of an individual or business entity in the state of Arkansas. It serves as a valuable tool in assessing the financial health and profitability of an organization by providing key information about its operational performance. Keywords: Arkansas, income statement, financial document, revenue, expenses, net income, financial health, profitability, operational performance. The income statement in Arkansas follows a standardized format adhering to Generally Accepted Accounting Principles (GAAP). It consists of several sections that provide a comprehensive picture of the financial performance. The primary components of the Arkansas Income Statement include: 1. Revenue: This section lists all the income generated by the entity during a specific accounting period. It encompasses sources such as sales revenue, service fees, rental income, interest income, and gains from investments or asset sales. 2. Cost of Goods Sold (COGS): In this section, the direct expenses associated with producing or acquiring the products or services sold by the entity are detailed. This may include the costs of raw materials, direct labor, manufacturing overhead, or inventory purchases. 3. Gross Profit: Gross profit is calculated by deducting the COGS from the total revenue. It represents the amount of money left after accounting for the direct costs of goods or services, providing an initial indication of profitability. 4. Operating Expenses: This section includes all the expenses incurred while conducting day-to-day operations. They consist of selling, general, and administrative expenses (SGA), research and development costs, marketing expenses, payroll expenses, rent, utilities, and other overheads. 5. Operating Income: Operating income is derived by subtracting the operating expenses from the gross profit. It reflects the profitability of the core business operations of the entity, excluding other non-operational factors. 6. Non-Operating Income and Expenses: This section accounts for income and expenses not directly related to core operations, usually including interest income, interest expenses, gains or losses from investments, and any extraordinary items. 7. Net Income: Net income, also known as the bottom line, is calculated by subtracting non-operating income and expenses from the operating income. It represents the final profit or loss earned during the accounting period, demonstrating the overall performance of the entity. Different types of Arkansas Income Statements may exist based on the organization's legal structure or reporting requirements. These can include income statements applicable to sole proprietorship, partnerships, corporations, or nonprofit entities. However, all variations serve the same purpose of presenting an accurate picture of financial performance. In conclusion, the Arkansas Income Statement is a crucial financial document that reflects the revenue, expenses, and net income of an individual or business in the state. It provides stakeholders with essential information to assess financial health, profitability, and operational efficiency. By analyzing the components of the income statement, one can gain insights into the financial performance of the organization and make informed decisions regarding its financial affairs.