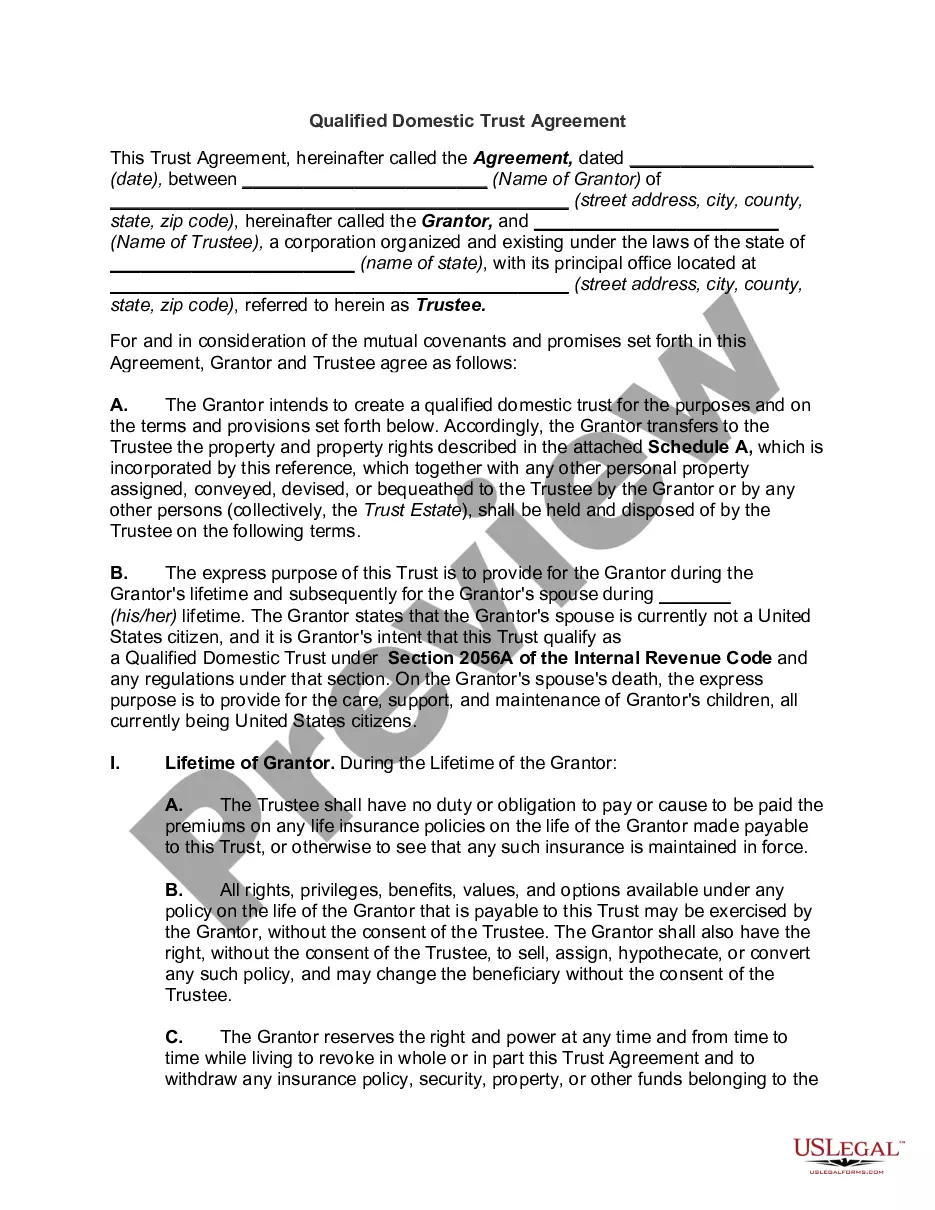

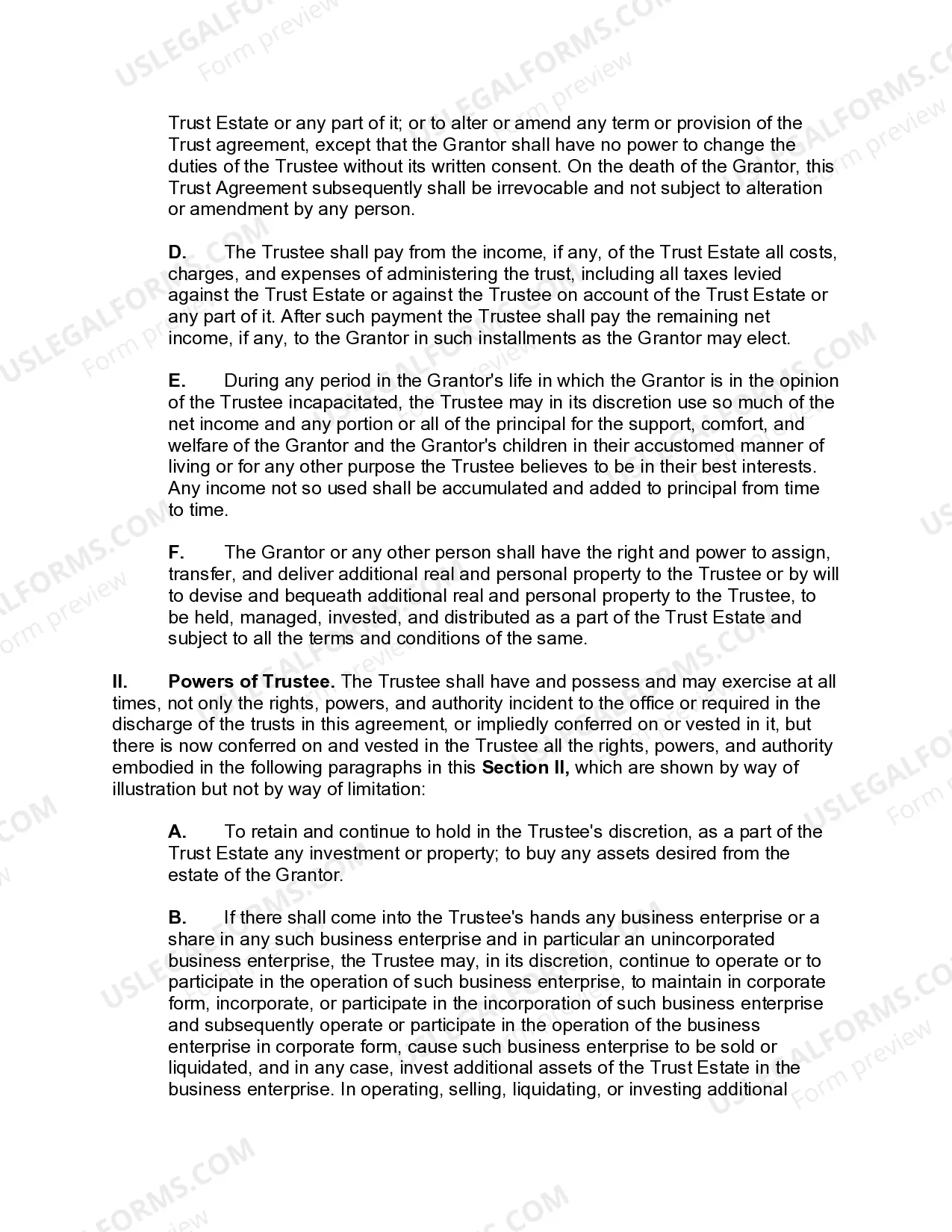

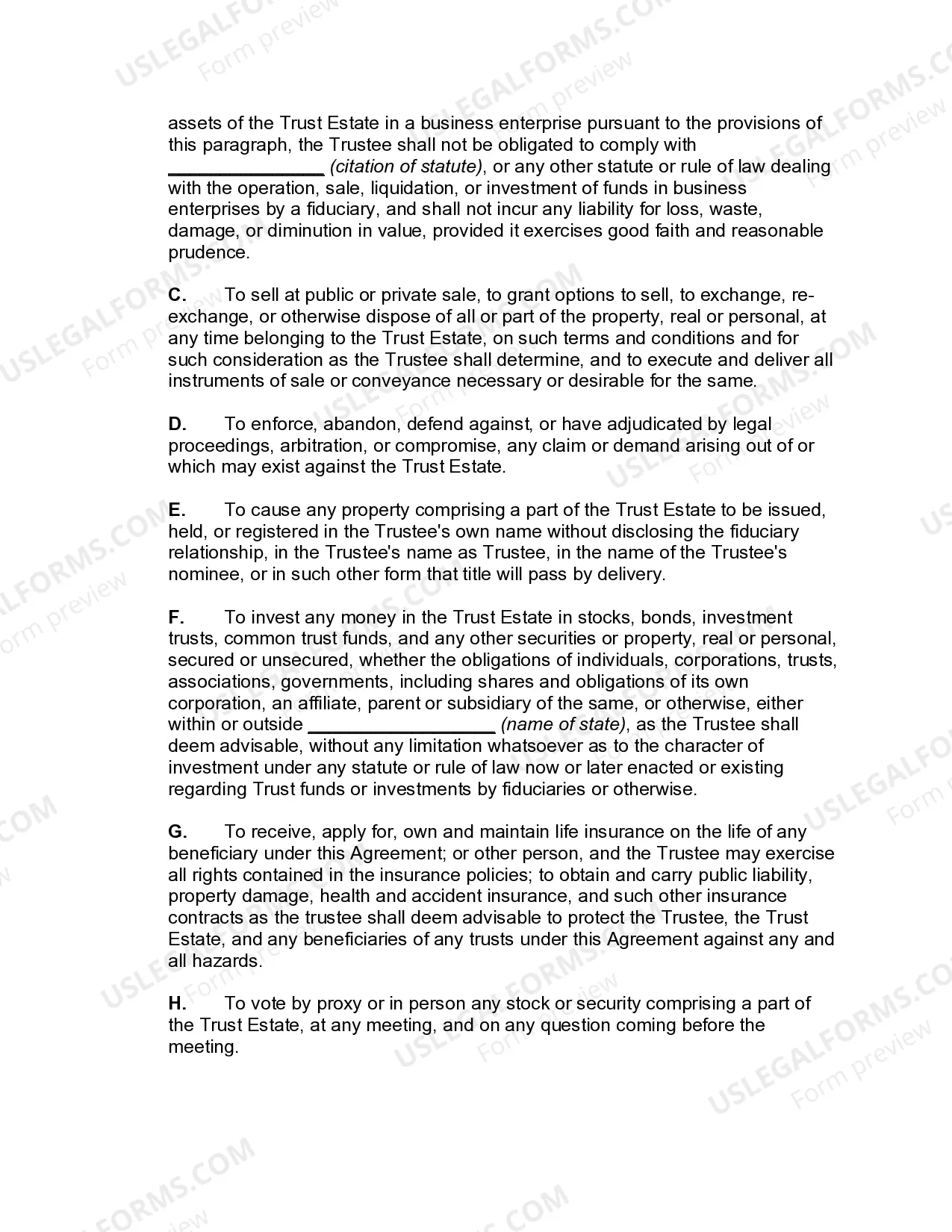

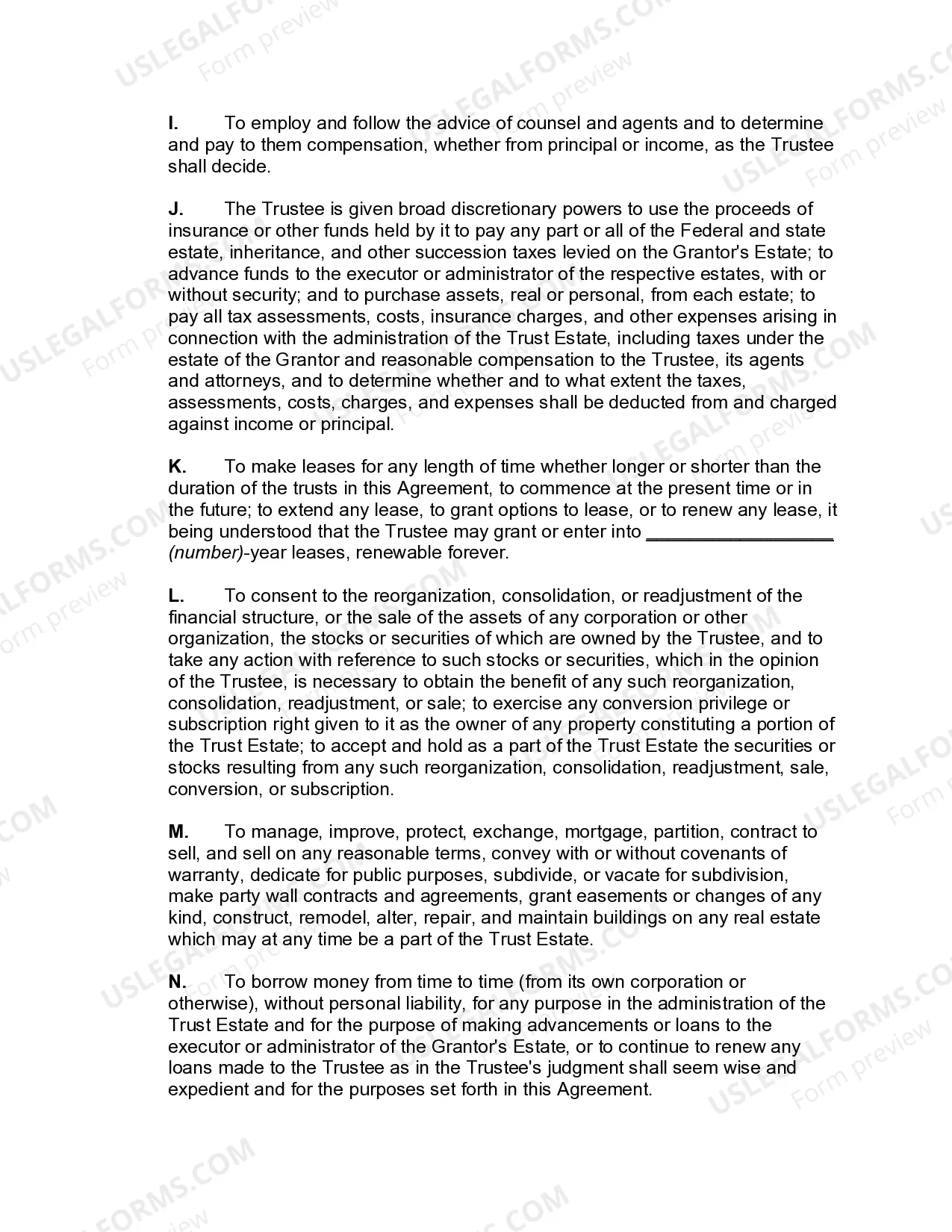

The Arkansas Qualified Domestic Trust Agreement is a legal document that allows non-U.S. citizen spouses to obtain certain tax benefits regarding their estate planning. Also known as an Arkansas DOT, this trust enables a non-citizen surviving spouse to qualify for minimum estate tax exemptions and defer tax payments until the distribution of the trust assets. Let's delve into the specifics of this trust agreement and explore its various types, if applicable. In Arkansas, a Qualified Domestic Trust Agreement is created to meet the requirements outlined in the Internal Revenue Code (IRC) Section 2056A. This provision allows estates with a non-U.S. citizen surviving spouse to defer estate tax payments until the death of the surviving spouse, thereby alleviating immediate financial burden during the estate administration process. By establishing an Arkansas DOT, a non-U.S. citizen spouse can receive distributions from the trust while preserving the estate tax deferral. The Arkansas DOT agreement is designed to ensure that estate taxes are eventually paid when assets are distributed from the trust to the surviving spouse. As per the IRC Section 2056A, the trust creator or "granter" must appoint a U.S. citizen or domestic corporation as the trustee. The trustee assumes the responsibility of filing tax returns, overseeing the trust's management, and complying with all relevant tax laws. Different types of Arkansas Qualified Domestic Trust Agreements may include: 1. Testamentary DOT: This type of trust is established upon the death of the trust creator and is commonly included within their will or as a testamentary addition to an existing revocable living trust. Testamentary Dots can be beneficial when the trust creator owns assets solely in their name at the time of death. 2. Inter Vivos DOT: An inter vivos DOT is established during the lifetime of the trust creator, allowing them to transfer assets into the trust that qualify for DOT status. This type of DOT is typically useful for individuals who desire to ensure that their non-U.S. citizen spouse will have access to the estate's assets if the creator becomes incapacitated. 3. Marital Deduction DOT: This type of DOT is established to maximize the marital deduction. It allows the estate to claim an unlimited marital deduction for assets transferred to the trust, minimizing estate taxes and deferring them until the distribution of trust assets or the death of the surviving spouse. It is important to consult with experienced estate planning attorneys or tax professionals to fully understand the intricacies of the Arkansas DOT and its various types. Estate planning laws may vary, and seeking professional guidance can ensure compliance with all legal requirements and optimize the tax benefits for non-U.S. citizen surviving spouses in Arkansas.

Arkansas Qualified Domestic Trust Agreement

Description

How to fill out Arkansas Qualified Domestic Trust Agreement?

If you want to comprehensive, obtain, or print out lawful document templates, use US Legal Forms, the greatest variety of lawful types, that can be found on the Internet. Utilize the site`s easy and hassle-free look for to get the paperwork you require. Various templates for organization and personal reasons are sorted by classes and suggests, or key phrases. Use US Legal Forms to get the Arkansas Qualified Domestic Trust Agreement within a few clicks.

In case you are previously a US Legal Forms buyer, log in for your bank account and click the Down load option to have the Arkansas Qualified Domestic Trust Agreement. Also you can gain access to types you previously delivered electronically within the My Forms tab of your own bank account.

If you use US Legal Forms initially, follow the instructions beneath:

- Step 1. Be sure you have selected the shape to the right area/country.

- Step 2. Take advantage of the Preview option to look through the form`s information. Don`t forget to read through the explanation.

- Step 3. In case you are unsatisfied with all the form, use the Research area at the top of the monitor to get other versions from the lawful form format.

- Step 4. After you have discovered the shape you require, click the Buy now option. Opt for the pricing strategy you prefer and include your credentials to sign up to have an bank account.

- Step 5. Procedure the purchase. You can utilize your credit card or PayPal bank account to complete the purchase.

- Step 6. Pick the structure from the lawful form and obtain it on your own device.

- Step 7. Full, revise and print out or signal the Arkansas Qualified Domestic Trust Agreement.

Every single lawful document format you buy is your own property permanently. You might have acces to each and every form you delivered electronically in your acccount. Click the My Forms area and select a form to print out or obtain again.

Be competitive and obtain, and print out the Arkansas Qualified Domestic Trust Agreement with US Legal Forms. There are millions of specialist and status-certain types you can utilize to your organization or personal requirements.