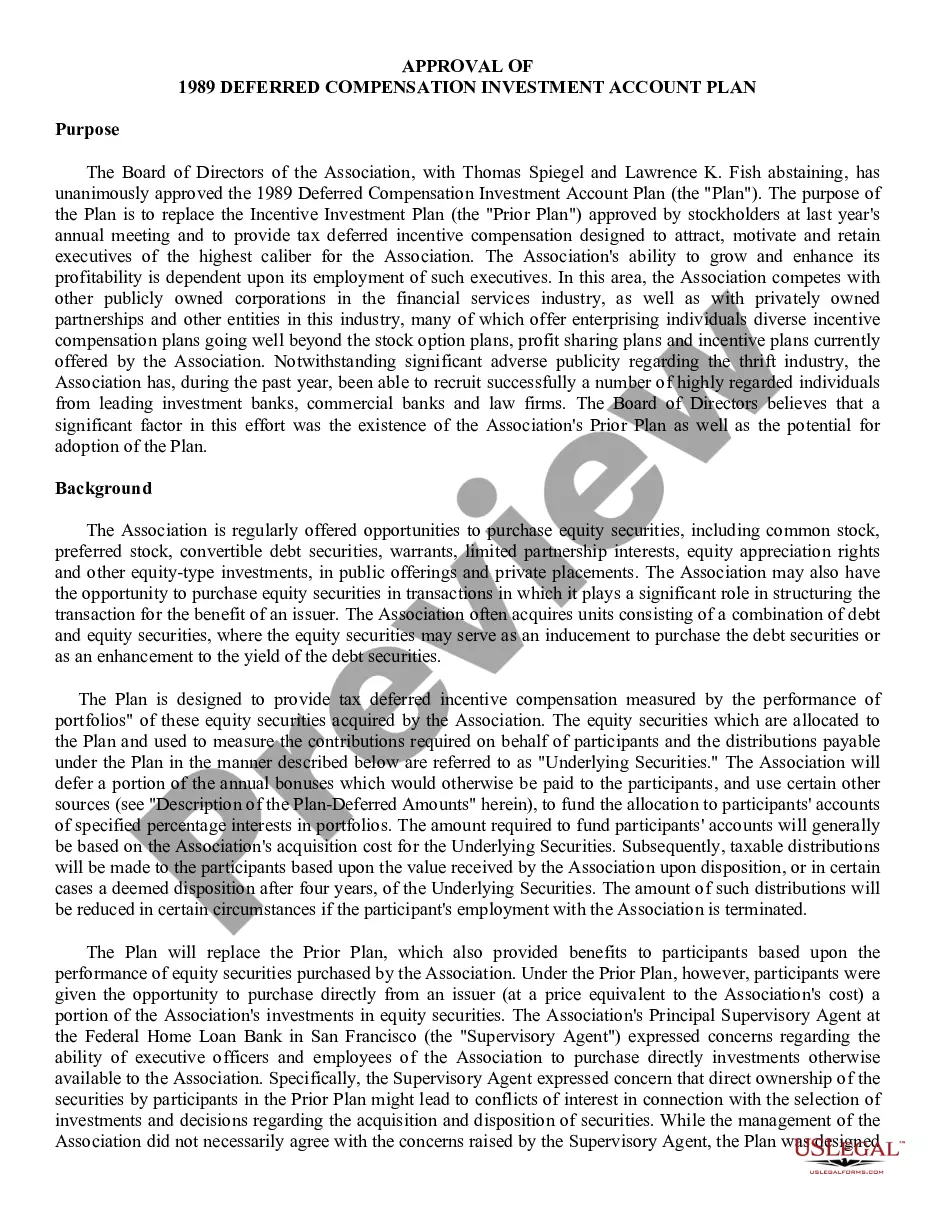

20-146 20-146 . . . Deferred Compensation Investment Account Plan under which Board of Directors of Savings and Loan Association allocates a portion of annual bonuses which would otherwise be paid to selected officers and employees to a separate account. The deferred compensation in such account is deemed, for purposes of Plan only, to represent specified percentages of Association's investments in certain portfolios of equity securities, and it is increased or decreased to same extent as performance of such securities

Arkansas Deferred Compensation Investment Account Plan

State:

Multi-State

Control #:

US-CC-20-146

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Deferred Compensation Investment Account Plan?

US Legal Forms - one of several biggest libraries of legal forms in the States - gives an array of legal file templates you can down load or print. Making use of the web site, you can get 1000s of forms for enterprise and personal purposes, categorized by classes, says, or keywords.You can get the most recent variations of forms like the Arkansas Deferred Compensation Investment Account Plan within minutes.

If you currently have a monthly subscription, log in and down load Arkansas Deferred Compensation Investment Account Plan through the US Legal Forms library. The Acquire button can look on every single kind you perspective. You have accessibility to all in the past saved forms within the My Forms tab of the accounts.

If you wish to use US Legal Forms the first time, here are basic instructions to help you get started:

- Ensure you have picked out the right kind to your metropolis/county. Go through the Preview button to examine the form`s content material. Look at the kind outline to actually have chosen the proper kind.

- If the kind doesn`t satisfy your demands, take advantage of the Lookup area towards the top of the display screen to get the one who does.

- If you are pleased with the form, verify your option by visiting the Acquire now button. Then, pick the rates plan you prefer and give your qualifications to sign up to have an accounts.

- Procedure the financial transaction. Use your bank card or PayPal accounts to perform the financial transaction.

- Choose the formatting and down load the form on your product.

- Make adjustments. Complete, revise and print and indicator the saved Arkansas Deferred Compensation Investment Account Plan.

Each and every web template you included with your money does not have an expiration particular date and it is the one you have forever. So, if you want to down load or print one more copy, just go to the My Forms section and click about the kind you want.

Obtain access to the Arkansas Deferred Compensation Investment Account Plan with US Legal Forms, one of the most considerable library of legal file templates. Use 1000s of professional and state-particular templates that meet your small business or personal needs and demands.

Form popularity

FAQ

The Bottom Line. If you have a qualified plan and have passed the vesting period, your deferred compensation is yours, even if you quit with no notice on very bad terms. If you have a non-qualified plan, you may have to forfeit all of your deferred compensation by quitting depending on your plan's specific terms.

You can take out small or large sums anytime, or you can set up automatic, periodic payments. If your plan allows it, you may be able to have direct deposit which allows for fast transfer of funds.

You can take out small or large sums anytime, or you can set up automatic, periodic payments. If your plan allows it, you may be able to have direct deposit which allows for fast transfer of funds. Unlike a check, direct deposit typically doesn't include a hold on the funds from your account.

You can request a loan by logging in to your DCP account, completing a Loan Application Form, or calling the Service Center at 844-523-2457.

A deferred compensation plan withholds a portion of an employee's pay until a specified date, usually retirement. The lump sum owed to an employee in this type of plan is paid out on that date. Examples of deferred compensation plans include pensions, 401(k) retirement plans, and employee stock options.

Investing your deferred compensation Your plan might offer you several options for the benchmark?often, major stock and bond indexes, the 10-year US Treasury note, the company's stock price, or the mutual fund choices in the company 401(k) plan.

The Plan is designed to help you save for retirement. But there are specific situations where you may be able to withdraw money from your account before retirement to help with certain financial hardships or you may even qualify for the low balance provision.

Deferred compensation plans don't have required minimum distributions, either. Based upon your plan options, generally, you may choose 1 of 2 ways to receive your deferred compensation: as a lump-sum payment or in installments.