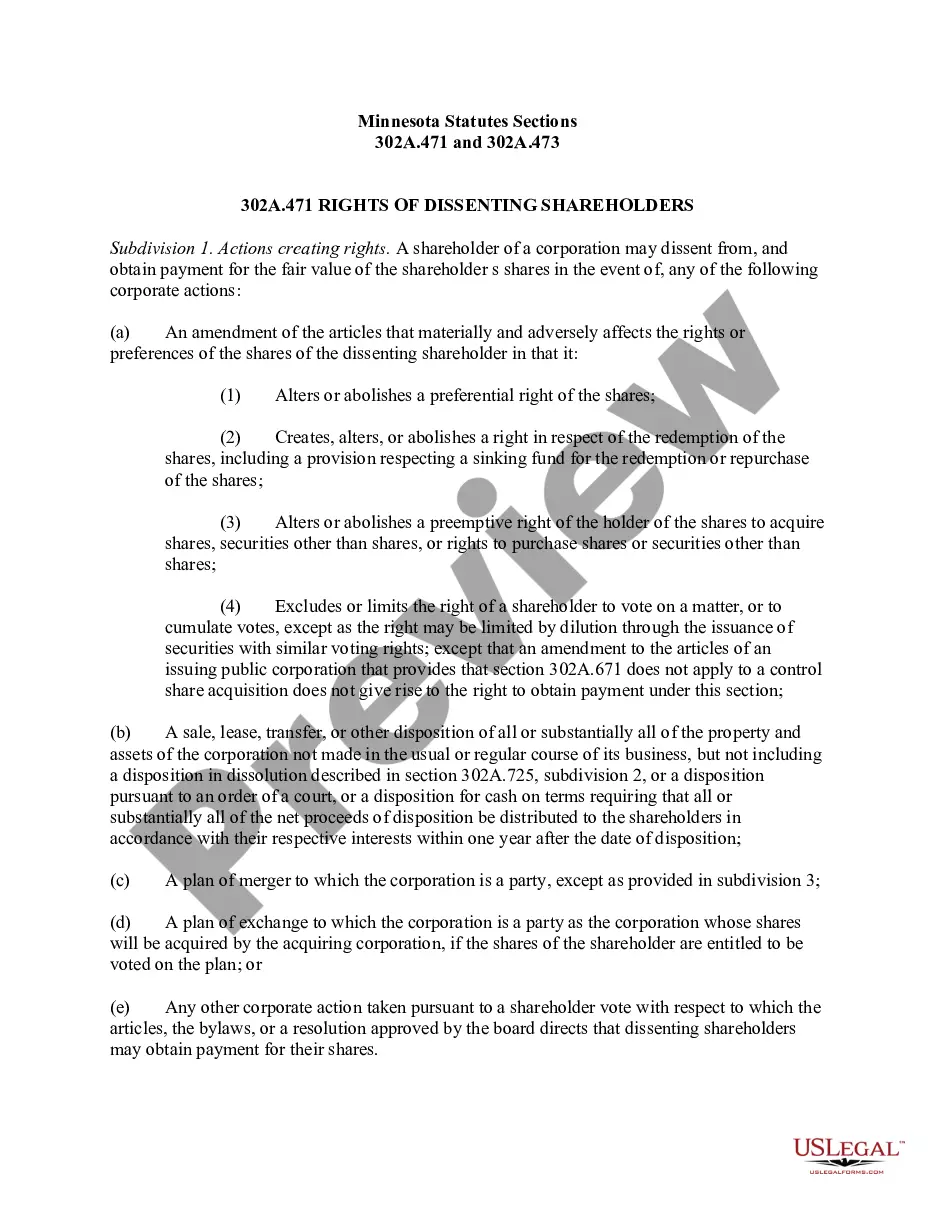

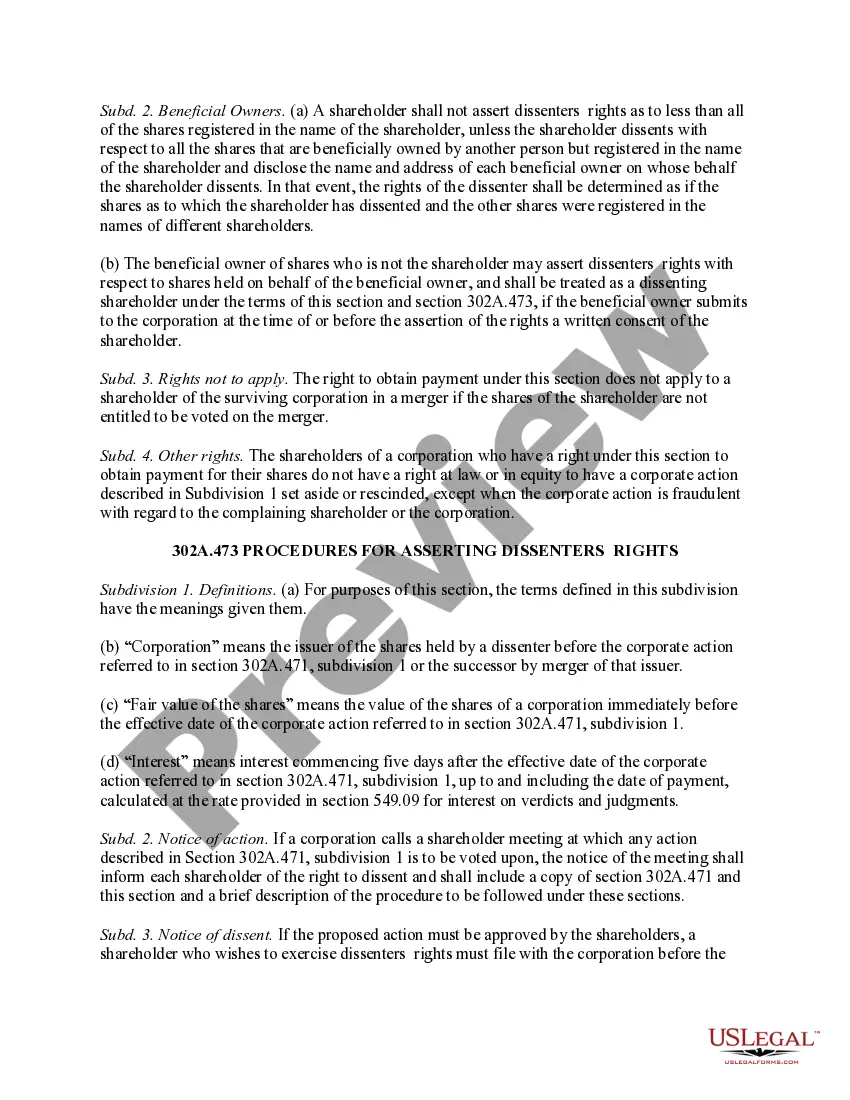

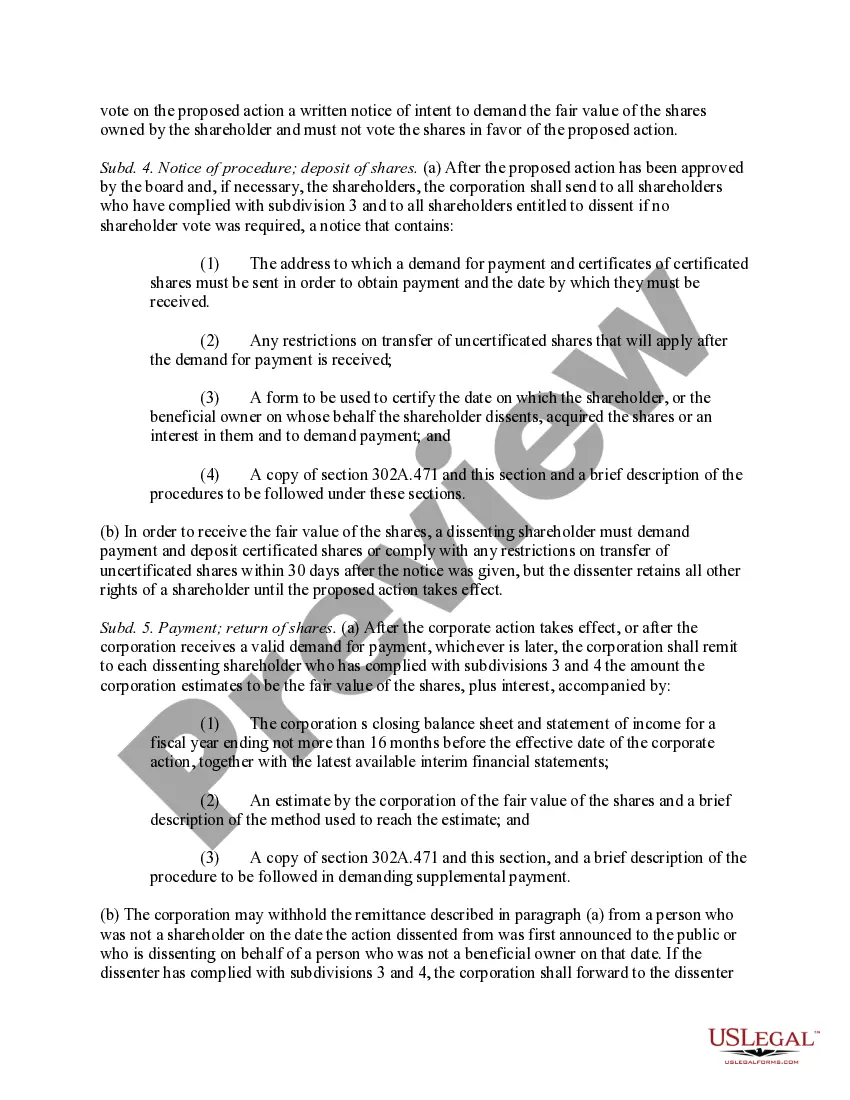

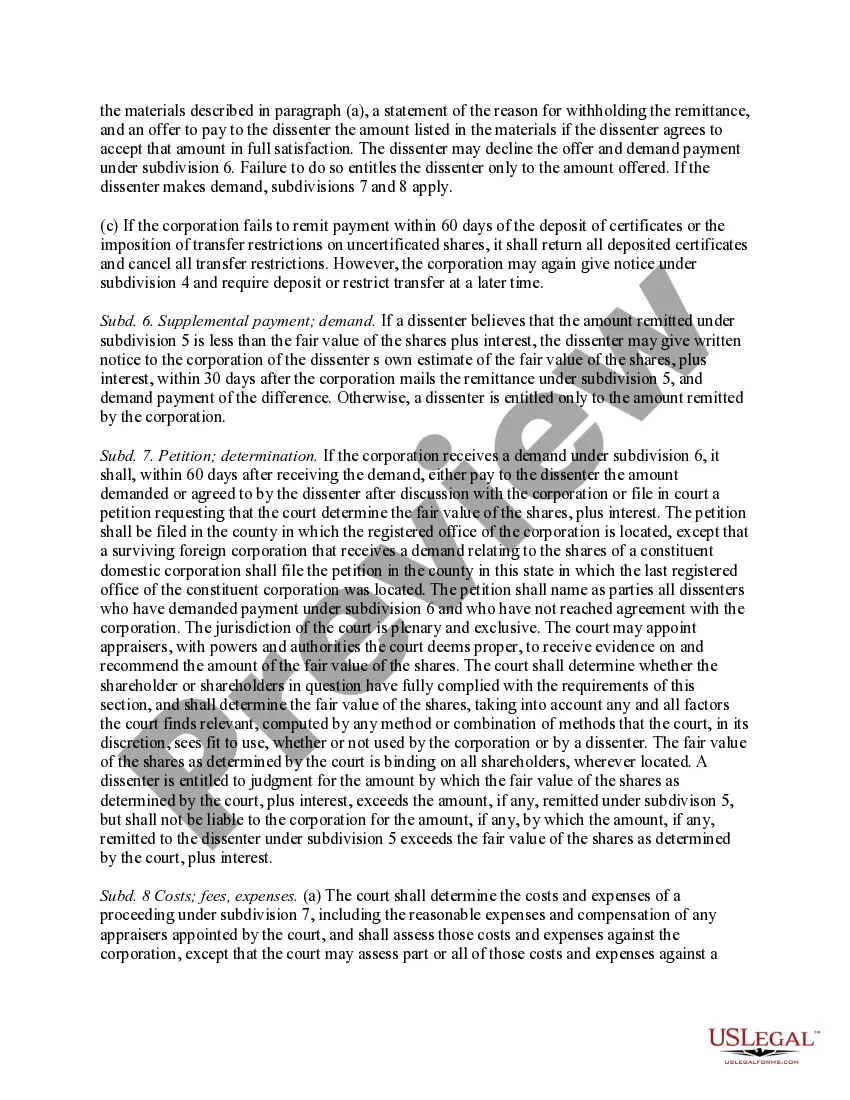

Arkansas Sections 302A.471 and 302A.473 of the Minnesota Business Corporation Act play a crucial role in governing the legal structure and operations of business corporations within the state. These sections outline essential provisions related to corporate distributions and dissenters' rights. Let's delve into the details of each section separately: 1. Arkansas Section 302A.471: Section 302A.471 of the Minnesota Business Corporation Act primarily addresses corporate distributions, specifying the rules and limitations for distributing profits among shareholders. Some relevant keywords associated with this section include "corporate distribution," "profits," "shareholders," and "dividends." Under this section, corporations must adhere to the following regulations regarding distributions: — Distributions can only be made out of surplus profits or in accordance with the company's articles of incorporation. — Corporations must consider their current and future financial standings before making distributions. — It prohibits distributions if the corporation would be insolvent, or if the distribution would render it unable to meet its obligations. Moreover, the section provides clarity on the consequences of improper distributions. It states that directors approving unlawful distributions may be held personally liable for the debts of the corporation, and shareholders receiving such distributions may be required to return them. 2. Arkansas Section 302A.473: Section 302A.473 of the Minnesota Business Corporation Act pertains to dissenters' rights within business corporations. This section safeguards the interests of dissenting shareholders during specified corporate actions, such as mergers, sales of assets, or amendments to corporate articles. The inclusion of relevant keywords like "dissenters' rights," "shareholders," "mergers," and "sale of assets" is important for this section. Under this section, dissenting shareholders have the following rights: — They can dissent from certain corporate actions and demand payment of fair value for their shares. — The corporation must provide a dissenters' notice, outlining the required steps for dissenting shareholders to assert their rights. — Dissenting shareholders may need to follow specific procedures and deadlines defined by this section to exercise their rights effectively. Additionally, the section addresses the responsibilities of the corporation, such as payment of fair value to dissenting shareholders, the withdrawal of dissenting rights if shareholders fail to comply with requirements, and the procedures for settling disputes related to dissenters' rights. In conclusion, Arkansas Sections 302A.471 and 302A.473 within the Minnesota Business Corporation Act are vital components governing corporate distributions and dissenters' rights, respectively. Understanding the intricacies and implications of these sections is crucial for business corporations operating in Arkansas, as compliance ensures lawful and fair corporate practices.

Arkansas Sections 302A.471 and 302A.473 of Minnesota Business Corporation Act

Description

How to fill out Arkansas Sections 302A.471 And 302A.473 Of Minnesota Business Corporation Act?

US Legal Forms - one of many largest libraries of legal varieties in America - provides a wide range of legal file themes you are able to download or produce. Utilizing the internet site, you can get a large number of varieties for enterprise and specific reasons, categorized by classes, claims, or keywords.You will discover the most recent models of varieties much like the Arkansas Sections 302A.471 and 302A.473 of Minnesota Business Corporation Act in seconds.

If you already possess a membership, log in and download Arkansas Sections 302A.471 and 302A.473 of Minnesota Business Corporation Act from the US Legal Forms catalogue. The Down load option can look on each form you perspective. You have access to all previously downloaded varieties from the My Forms tab of your own account.

If you would like use US Legal Forms the first time, here are easy recommendations to obtain started:

- Be sure you have picked out the right form to your area/state. Click on the Preview option to review the form`s content. See the form information to actually have chosen the proper form.

- In case the form doesn`t match your demands, use the Search field near the top of the monitor to discover the one which does.

- When you are satisfied with the shape, confirm your selection by clicking on the Buy now option. Then, choose the rates program you prefer and give your qualifications to register to have an account.

- Method the transaction. Use your Visa or Mastercard or PayPal account to accomplish the transaction.

- Select the formatting and download the shape on the product.

- Make changes. Fill out, modify and produce and indicator the downloaded Arkansas Sections 302A.471 and 302A.473 of Minnesota Business Corporation Act.

Every design you put into your money lacks an expiry day and is the one you have eternally. So, in order to download or produce one more version, just proceed to the My Forms portion and click around the form you will need.

Get access to the Arkansas Sections 302A.471 and 302A.473 of Minnesota Business Corporation Act with US Legal Forms, by far the most extensive catalogue of legal file themes. Use a large number of specialist and state-specific themes that satisfy your company or specific demands and demands.