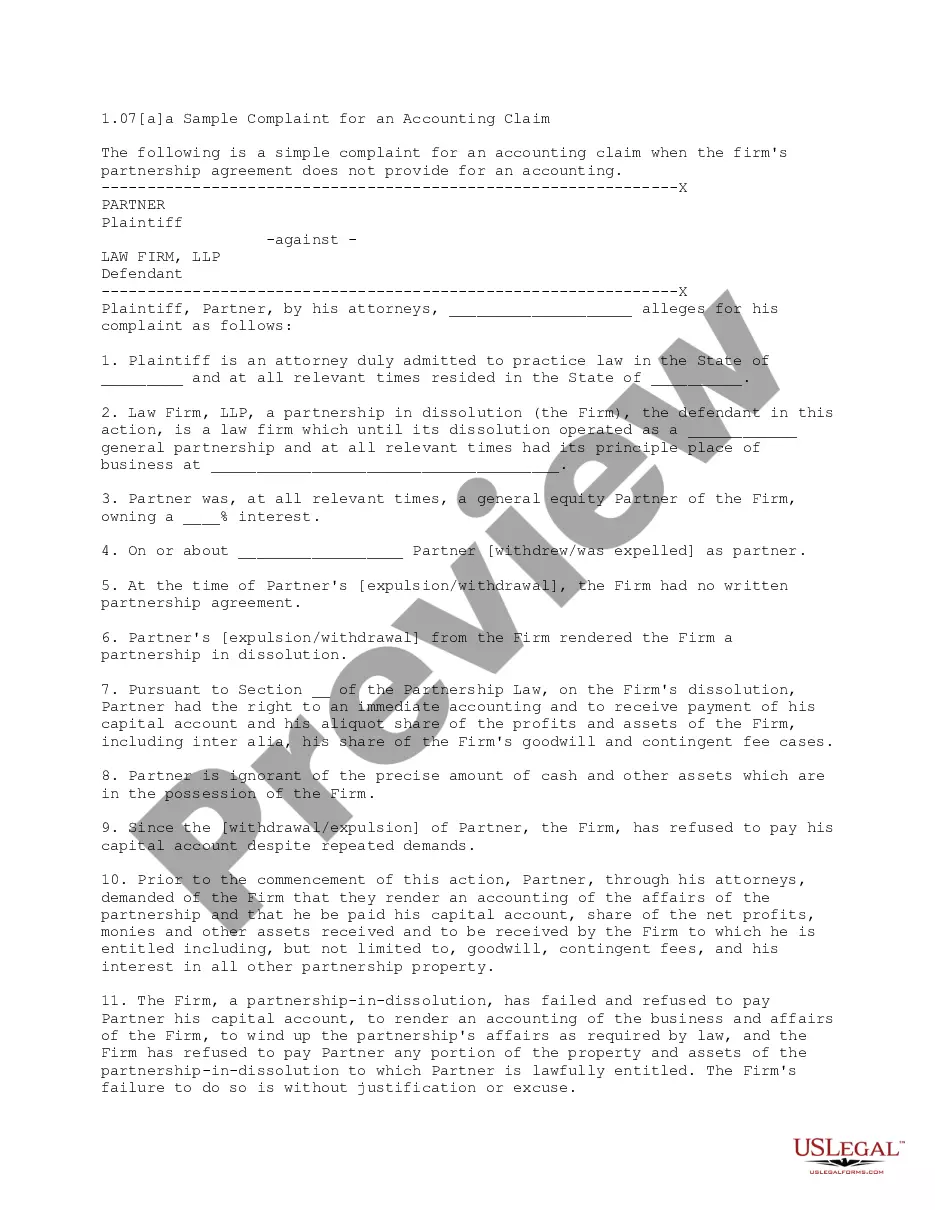

This complaint is for a plaintiff attorney who has been removed from the partnership of his former firm. The complaint requests an accounting of the former firm, stating that the plaintiff has been deprived of economic benefits rightfully due to him under the former partnership agreement, and also alleges egregious acts by his former partners.

Arkansas Alternative Complaint for an Accounting which includes Egregious Acts

Category:

State:

Multi-State

Control #:

US-L0107A

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Alternative Complaint For An Accounting Which Includes Egregious Acts?

Finding the right authorized file design might be a have a problem. Naturally, there are plenty of web templates available online, but how do you discover the authorized develop you want? Make use of the US Legal Forms web site. The services offers a large number of web templates, for example the Arkansas Alternative Complaint for an Accounting which includes Egregious Acts, that you can use for business and private requires. All the forms are examined by pros and fulfill state and federal needs.

When you are presently signed up, log in to the profile and click the Down load switch to get the Arkansas Alternative Complaint for an Accounting which includes Egregious Acts. Make use of your profile to appear through the authorized forms you may have acquired earlier. Proceed to the My Forms tab of the profile and have another version of the file you want.

When you are a whole new customer of US Legal Forms, listed here are straightforward instructions for you to adhere to:

- Very first, be sure you have selected the right develop to your city/state. You are able to look through the form utilizing the Preview switch and look at the form explanation to make certain this is basically the right one for you.

- When the develop is not going to fulfill your preferences, take advantage of the Seach discipline to discover the correct develop.

- When you are positive that the form is proper, click on the Acquire now switch to get the develop.

- Choose the prices prepare you would like and enter in the necessary details. Design your profile and purchase the order using your PayPal profile or bank card.

- Select the submit file format and download the authorized file design to the gadget.

- Complete, modify and print out and signal the attained Arkansas Alternative Complaint for an Accounting which includes Egregious Acts.

US Legal Forms may be the biggest library of authorized forms where you will find various file web templates. Make use of the company to download appropriately-made paperwork that adhere to express needs.

Form popularity

FAQ

By agreement with the six chartered accountancy bodies, the FRC has a non-statutory role for oversight of the regulation by the professional accountancy bodies of their members beyond those that are statutory auditors.

If your accountant is not responding to you and causing problems for your business, especially with your tax return, you may want to file an official complaint.

You may be able to sue your accountant for negligence but only in the following circumstances: If the accountant has admitted fault ? If your accountant has admitted to making the mistake that is all the proof you need to file a claim in court for compensation for the additional fees or interest you have incurred.

What should I do if I have a complaint about an accountant or actuary? You should complain to the accountant (or their firm) or actuary first. If you are unhappy with their response you should complain to their professional body, if they have one.

The following represent the most common allegations made against CPAs and accounting firms: Negligence and incompetence. Fraud, deceit, and misrepresentation in the practice of public accountancy. Failing to perform services in ance with professional standards. Criminal convictions.

Specific examples of accounting malpractice include: Giving incorrect tax advice or making tax return errors. Manipulating financial statements or providing incorrect reports to stockholders or partners. Wrongful certification or failure to properly audit financial statements.

What should I do if I have a complaint about an accountant or actuary? You should complain to the accountant (or their firm) or actuary first. If you are unhappy with their response you should complain to their professional body, if they have one.