This lease rider form may be used when you are involved in a lease transaction, and have made the decision to utilize the form of Oil and Gas Lease presented to you by the Lessee, and you want to include additional provisions to that Lease form to address specific concerns you may have, or place limitations on the rights granted the Lessee in the “standard” lease form.

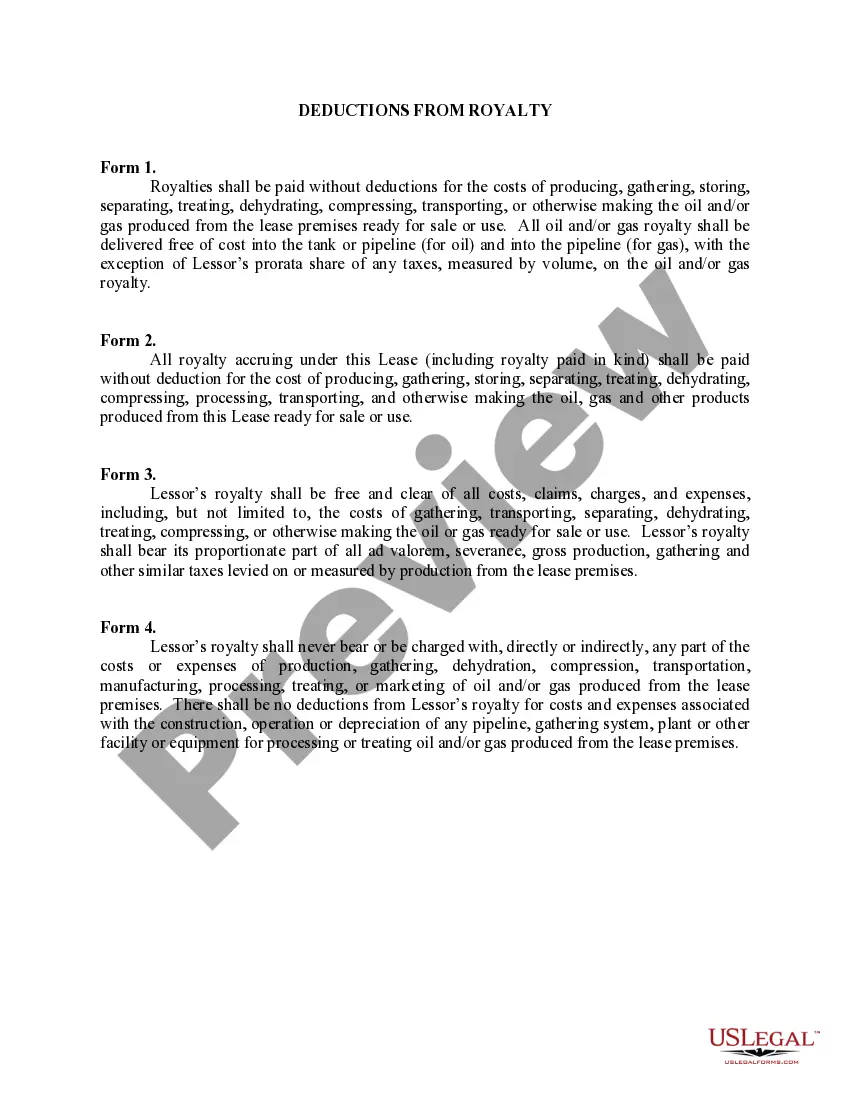

Arkansas Deductions from Royalty refers to the allowable deductions that can be claimed by royalty owners in the state of Arkansas. These deductions are applicable to individuals or entities who own and receive royalty payments from oil, gas, mineral, or other natural resource extraction activities in Arkansas. These deductions aim to reduce the tax burden on royalty owners and encourage continued investment and production in the state. The deductions from royalty in Arkansas can be classified into several categories: 1. Ordinary and Necessary Expenses: This category includes all ordinary and necessary expenses incurred by the royalty owner in the production, exploration, and development of the mineral extraction activities. It encompasses costs such as labor, equipment, materials, and supplies used in extracting, gathering, storing, and transporting the resources. 2. Depletion Allowance: Arkansas allows a depletion deduction equal to a percentage of the gross income received as royalty payments. The depletion deduction accounts for the gradual reduction or depletion of the natural resource reserves over time. The specific percentage may vary depending on the type of resource being extracted. 3. Lease Operating Expenses: These expenses cover the costs associated with operating the leased property, including repairs, maintenance, taxes, insurance premiums, and other relevant expenses incurred during the production process. Lease operating expenses may also cover administrative and professional fees, such as legal and accounting services. 4. Transportation and Marketing Expenses: Royalty owners may deduct expenses related to transporting and marketing the extracted resources. This includes costs incurred for pipelines, shipping, storage facilities, and marketing activities, such as advertising and promotion. 5. Severance Taxes: In some cases, Arkansas allows royalty owners to deduct the amount of severance taxes paid to the state or other governmental entities. These taxes are typically based on the value or volume of the resources extracted and play a role in funding various public services and infrastructure projects. It is important for royalty owners in Arkansas to keep accurate records and documentation of all relevant expenses to support their claimed deductions. These deductions ultimately help reduce the taxable income from royalty payments, allowing individuals and businesses to retain a larger portion of their earnings from natural resource extraction activities in the state. By incentivizing investment and production, Arkansas promotes economic growth and sustainability in its resource-rich regions.Arkansas Deductions from Royalty refers to the allowable deductions that can be claimed by royalty owners in the state of Arkansas. These deductions are applicable to individuals or entities who own and receive royalty payments from oil, gas, mineral, or other natural resource extraction activities in Arkansas. These deductions aim to reduce the tax burden on royalty owners and encourage continued investment and production in the state. The deductions from royalty in Arkansas can be classified into several categories: 1. Ordinary and Necessary Expenses: This category includes all ordinary and necessary expenses incurred by the royalty owner in the production, exploration, and development of the mineral extraction activities. It encompasses costs such as labor, equipment, materials, and supplies used in extracting, gathering, storing, and transporting the resources. 2. Depletion Allowance: Arkansas allows a depletion deduction equal to a percentage of the gross income received as royalty payments. The depletion deduction accounts for the gradual reduction or depletion of the natural resource reserves over time. The specific percentage may vary depending on the type of resource being extracted. 3. Lease Operating Expenses: These expenses cover the costs associated with operating the leased property, including repairs, maintenance, taxes, insurance premiums, and other relevant expenses incurred during the production process. Lease operating expenses may also cover administrative and professional fees, such as legal and accounting services. 4. Transportation and Marketing Expenses: Royalty owners may deduct expenses related to transporting and marketing the extracted resources. This includes costs incurred for pipelines, shipping, storage facilities, and marketing activities, such as advertising and promotion. 5. Severance Taxes: In some cases, Arkansas allows royalty owners to deduct the amount of severance taxes paid to the state or other governmental entities. These taxes are typically based on the value or volume of the resources extracted and play a role in funding various public services and infrastructure projects. It is important for royalty owners in Arkansas to keep accurate records and documentation of all relevant expenses to support their claimed deductions. These deductions ultimately help reduce the taxable income from royalty payments, allowing individuals and businesses to retain a larger portion of their earnings from natural resource extraction activities in the state. By incentivizing investment and production, Arkansas promotes economic growth and sustainability in its resource-rich regions.