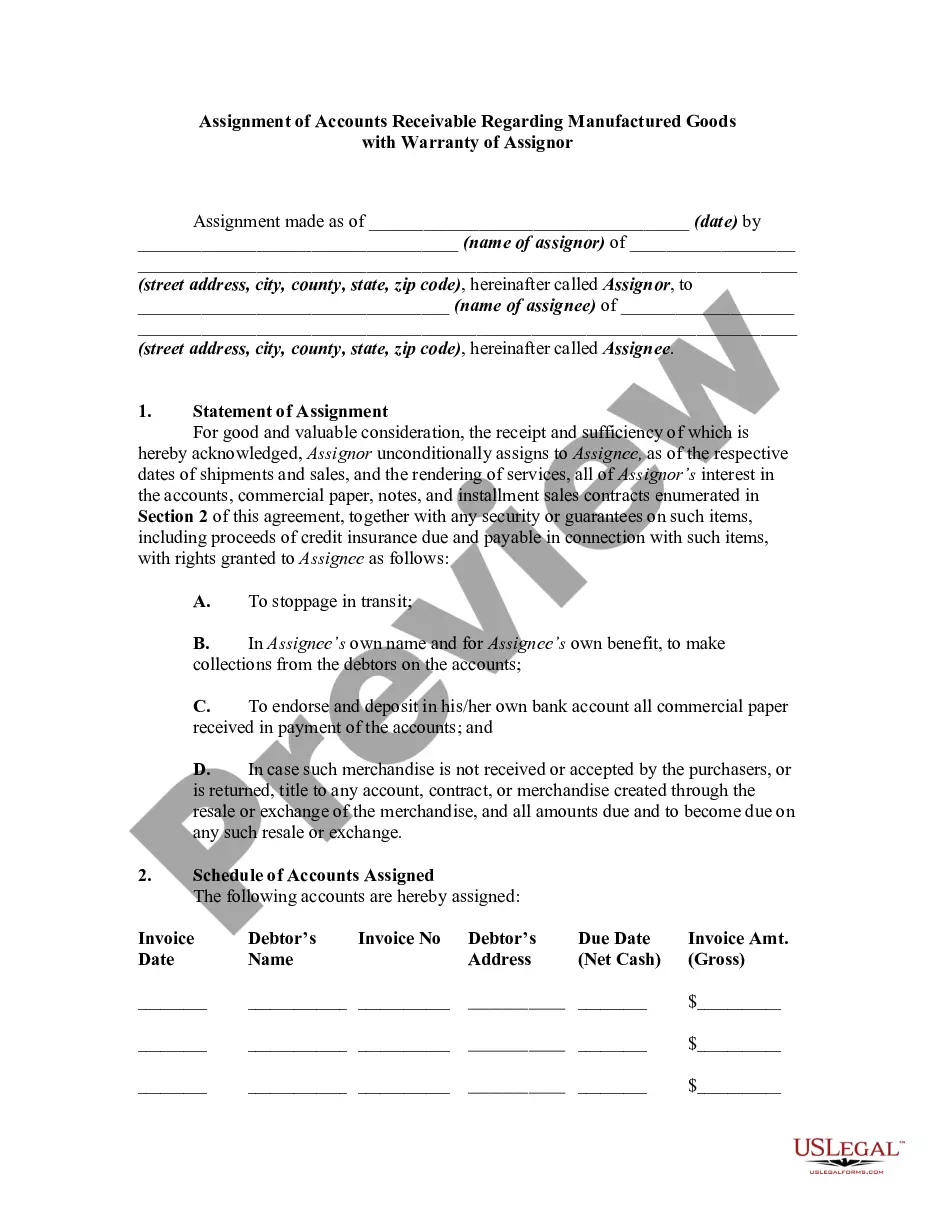

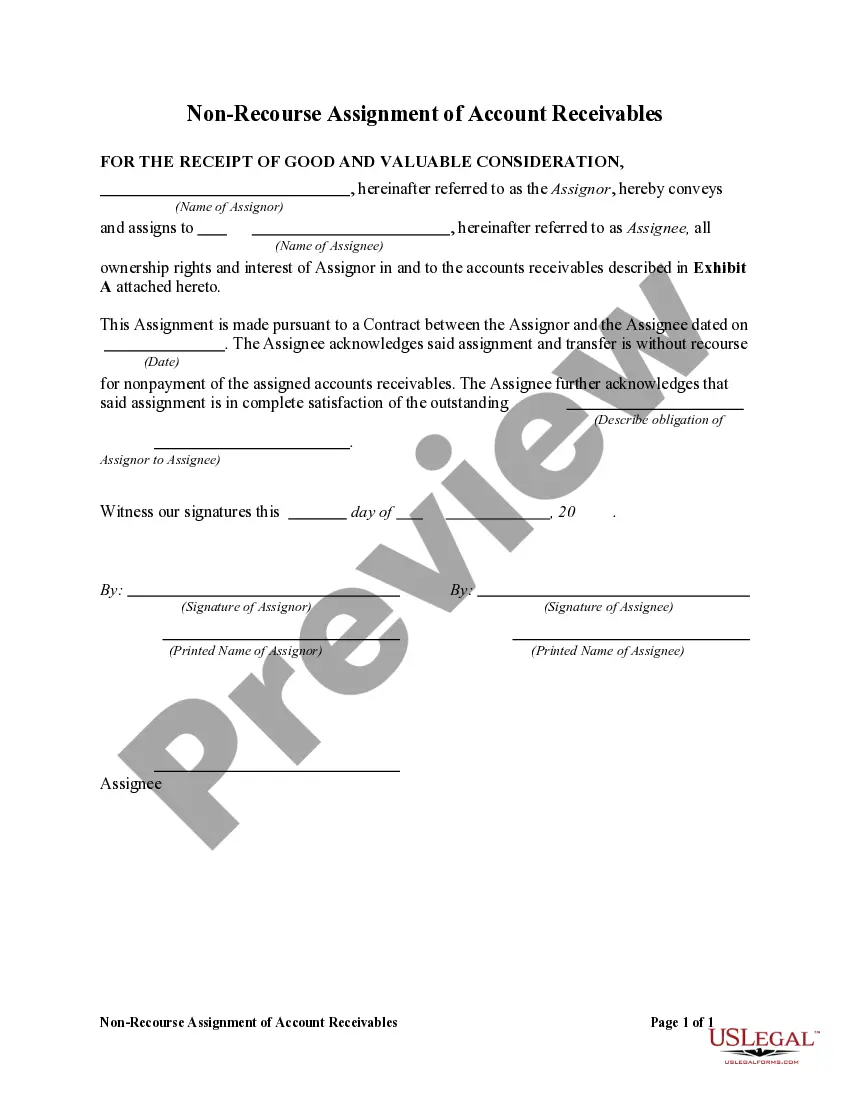

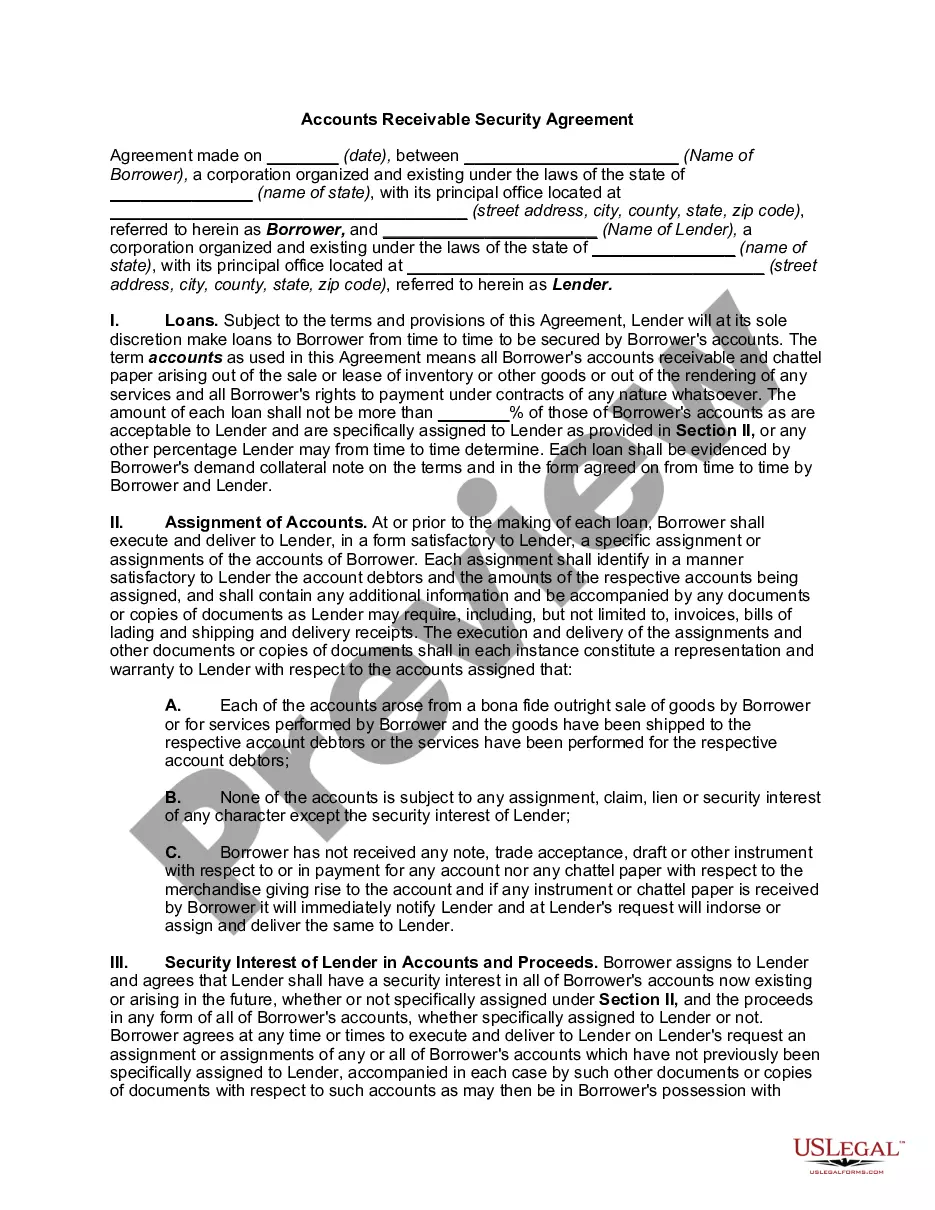

This form states that the guarantor unconditionally and absolutely guarantees to payee(s), jointly and severally, the full and prompt payment and performance of any and all account receivable charges by the customer incurred to the payee, including collections fees and reasonable attorneys' fees, up to a certain maximum amount.

Arizona Accounts Receivable - Guaranty

Category:

State:

Multi-State

Control #:

US-00401

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Accounts Receivable - Guaranty?

Are you in a situation where you require documents for both organizational or specific objectives almost every day.

There are numerous authentic document templates available online, but finding ones you can trust is not easy.

US Legal Forms offers a vast array of form templates, such as the Arizona Accounts Receivable - Guaranty, designed to meet state and federal requirements.

Once you find the right form, click Get now.

Choose the payment plan you prefer, fill in the necessary details to create your account, and complete your purchase using your PayPal or credit card.

- If you are already familiar with the US Legal Forms website and possess an account, simply Log In.

- Then, you can download the Arizona Accounts Receivable - Guaranty template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Find the form you need and ensure it is for the correct city/region.

- Use the Review button to examine the form.

- Read the description to ensure you have selected the correct template.

- If the form isn’t what you are looking for, use the Search field to find the form that suits your requirements.

Form popularity

FAQ

The 7 7 7 rule for collections refers to a structured approach to managing overdue accounts, particularly relevant for Arizona Accounts Receivable - Guaranty. This rule suggests that you should attempt to contact the debtor seven days after the due date, followed by another attempt seven days later, and finally, a third contact seven days after that. By spacing your communications this way, you increase the chances of receiving payment while maintaining a professional relationship. For businesses navigating collections in Arizona, utilizing a platform like uslegalforms can help streamline this process and ensure compliance with local regulations.

In Arizona, certain income is exempt from garnishment, which helps protect individuals from losing essential funds. For example, wages below a specific threshold, Social Security benefits, and certain pensions are typically exempt. This exemption allows individuals to maintain a minimum standard of living while dealing with debts. Knowing these exemptions is essential for anyone managing Arizona Accounts Receivable - Guaranty.

In Arizona, a creditor typically has six years to collect a debt. This time frame starts from the date of the last payment or the last activity related to the debt. After this period, the debt becomes unenforceable in court, which means the creditor cannot pursue legal action. Understanding the timeline for debt collection is crucial for managing your Arizona Accounts Receivable - Guaranty effectively.