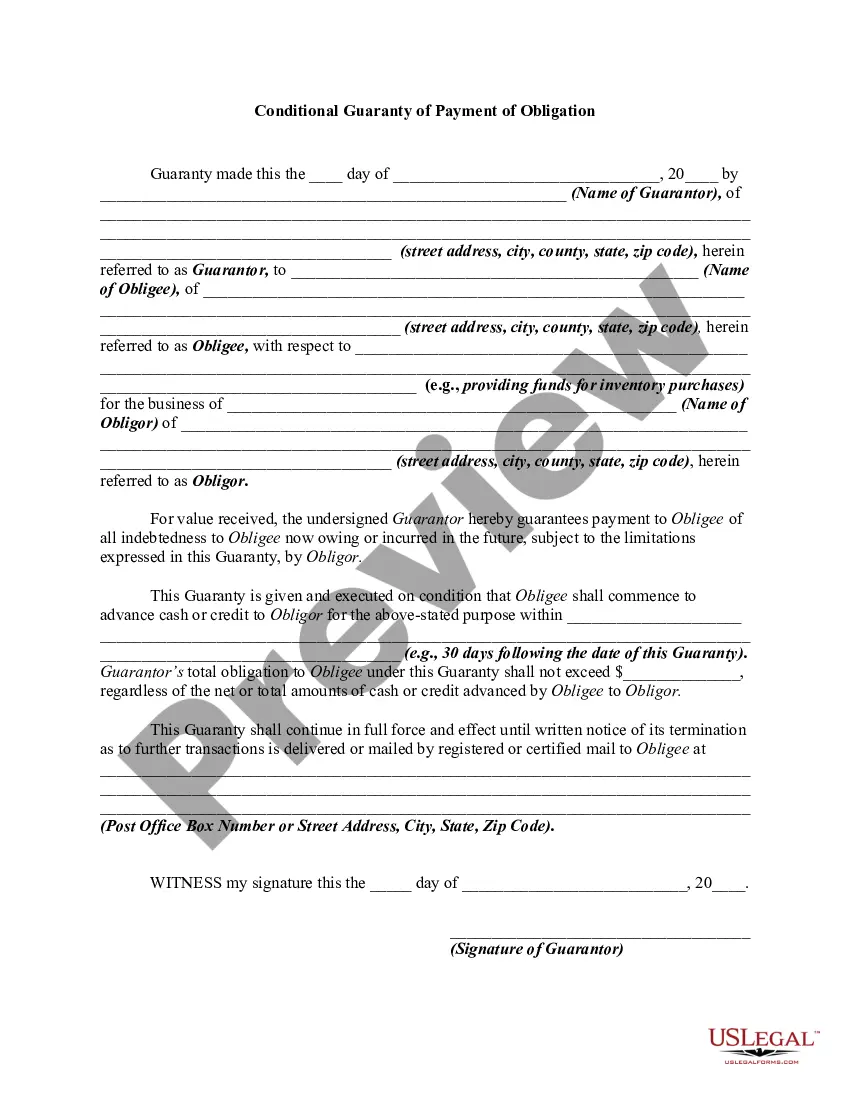

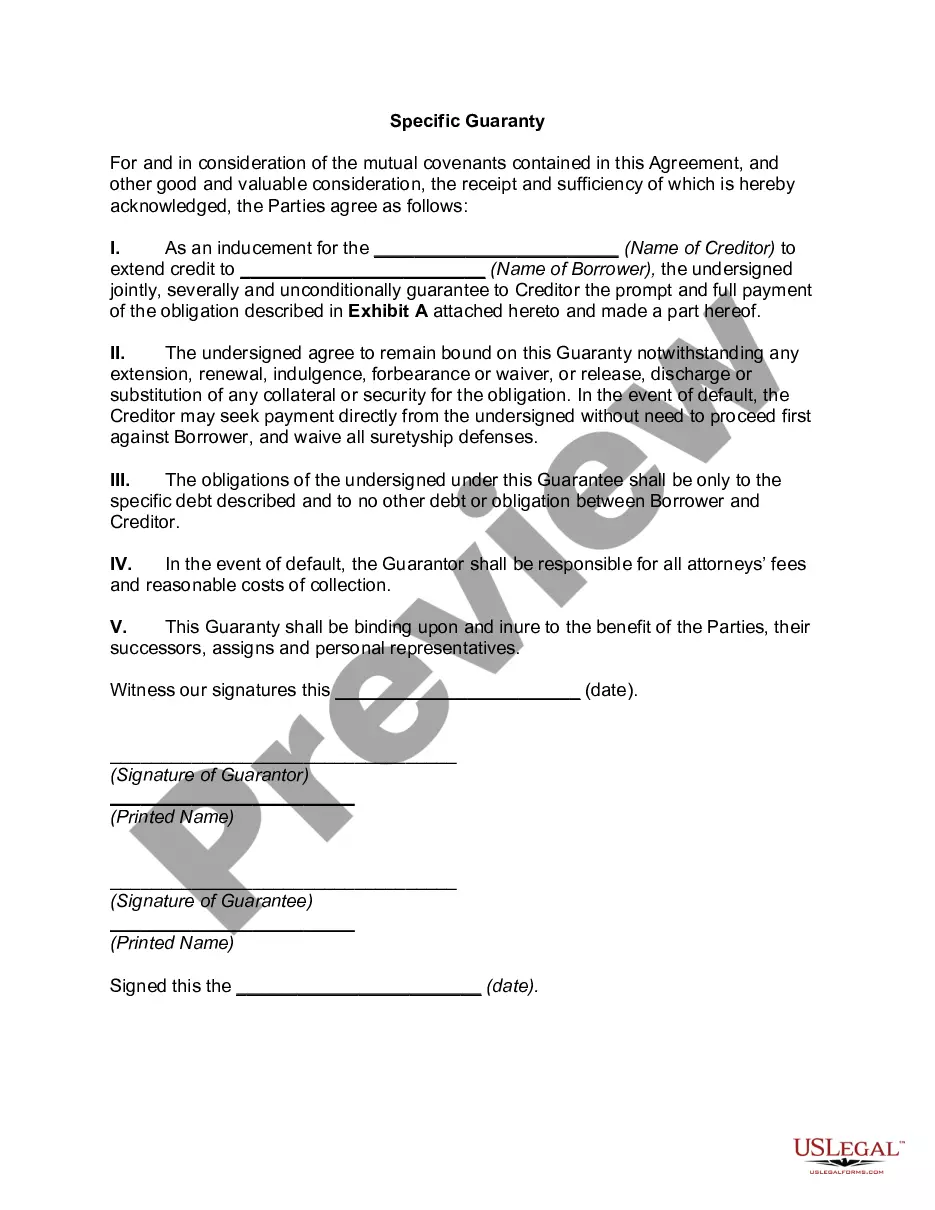

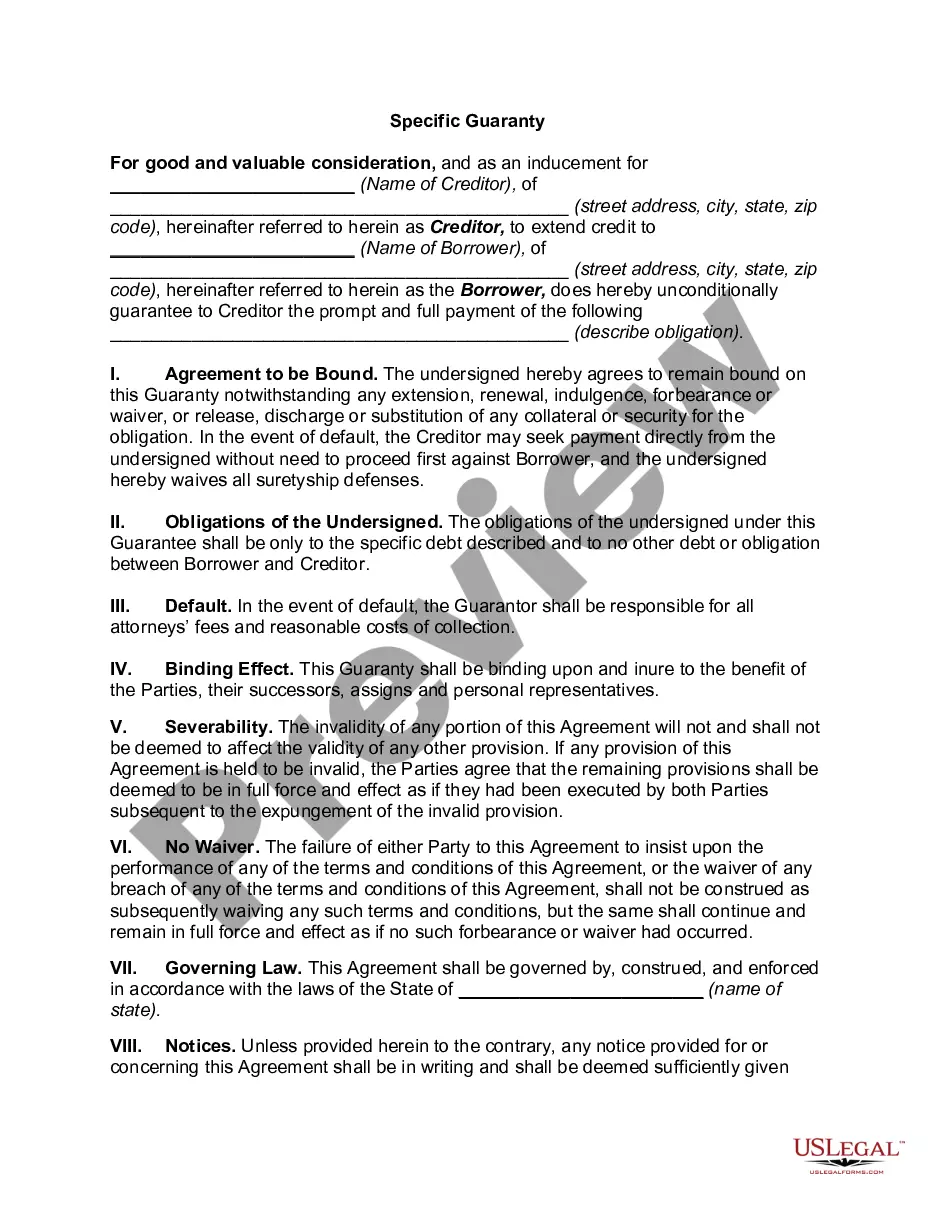

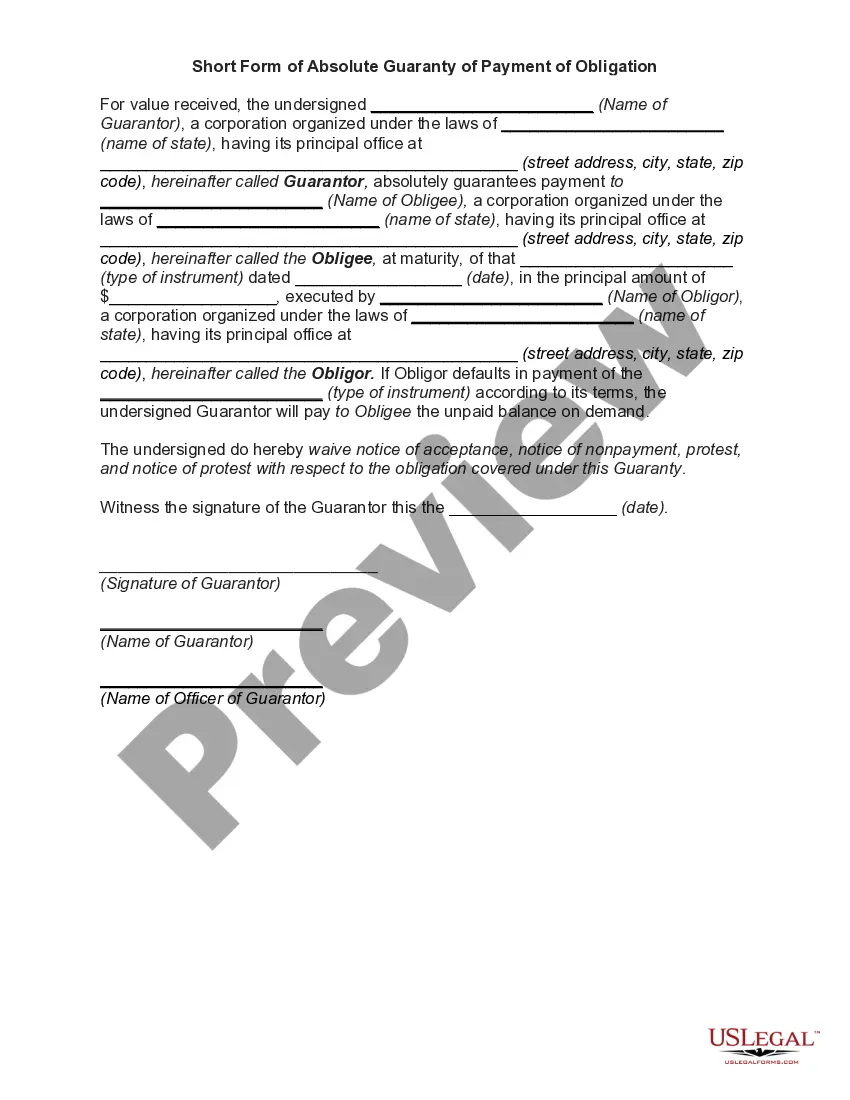

A guaranty is an undertaking on the part of one person (the guarantor) that is collateral to an obligation of another person (the debtor or obligor), and which binds the guarantor to performance of the obligation in the event of default by the debtor or obligor.

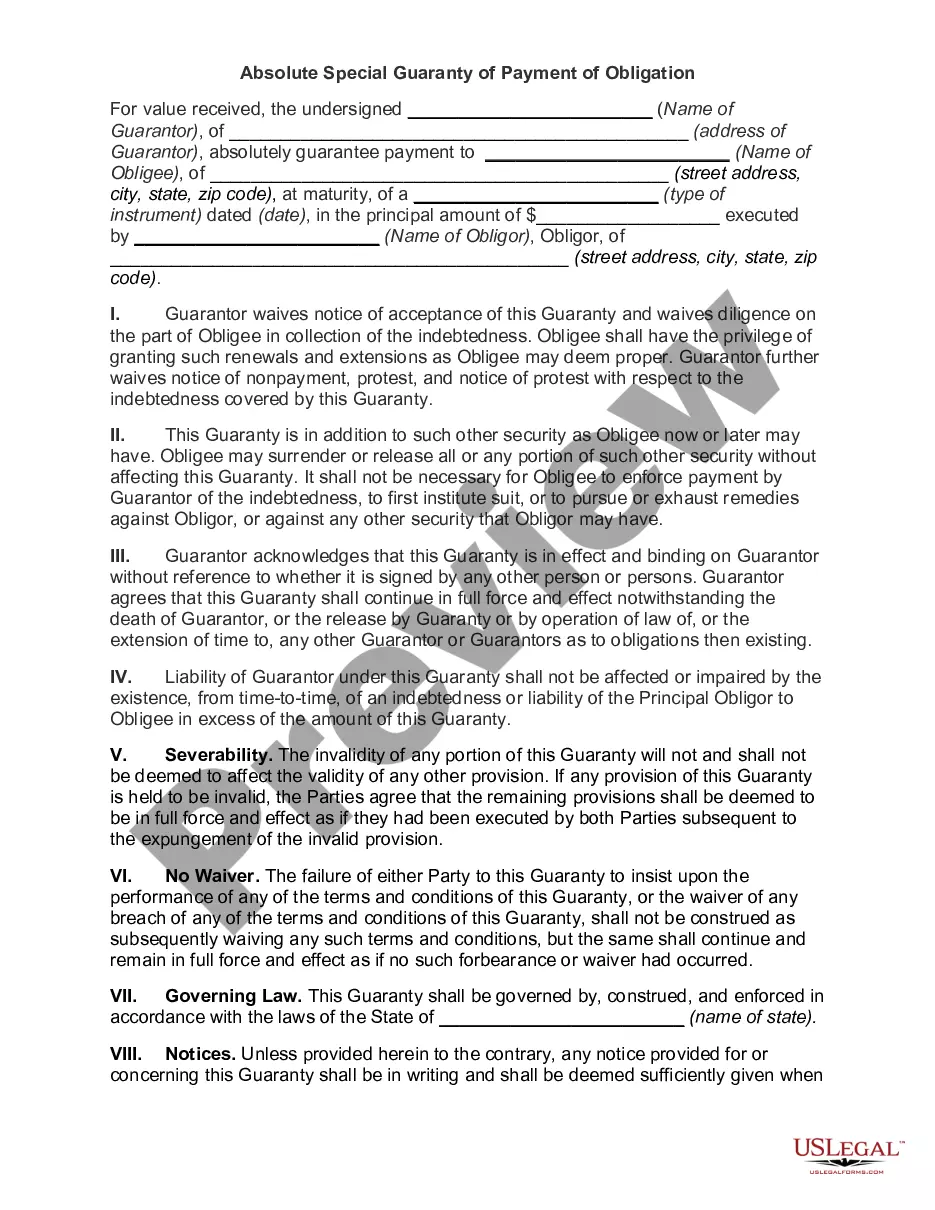

The contract of guaranty may be absolute or it may be conditional. An absolute guaranty is a contract by which the guarantor has promised that if the debtor does not perform the obligation or obligations, the guarantor will perform some act (such as the payment of money) to or for the benefit of the creditor.

A line of credit is an arrangement in which a lender extends a specified amount of credit to borrower for a specified time period.