This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

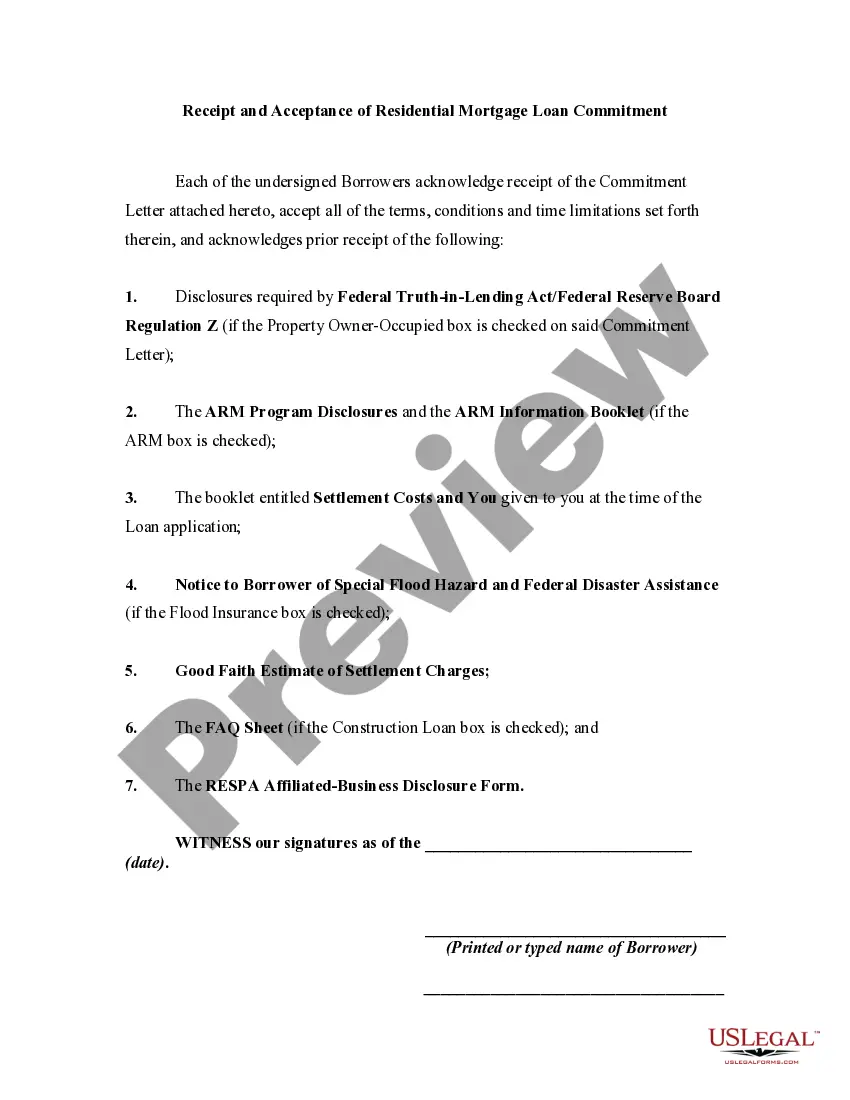

Arizona Receipt and Acceptance of Residential Mortgage Loan Commitment is a legal document used in the state of Arizona that verifies the borrower's receipt and acceptance of a mortgage loan commitment for a residential property. This document serves as a crucial step in the mortgage loan process and outlines the terms and conditions agreed upon by the borrower and the lender. The purpose of the Arizona Receipt and Acceptance of Residential Mortgage Loan Commitment is to establish a binding agreement between the borrower and the lender concerning the mortgage loan. By signing this document, the borrower acknowledges their understanding and acceptance of the loan commitment as well as their commitment to meet the specified terms and conditions. Keywords: Arizona, receipt, acceptance, residential mortgage loan commitment, legal document, borrower, lender, terms and conditions, binding agreement. Different types of Arizona Receipt and Acceptance of Residential Mortgage Loan Commitment include: 1. Fixed-rate mortgage loan commitment: This type of loan commitment offers a fixed interest rate over the life of the loan, providing borrowers with stability in their monthly payments. 2. Adjustable-rate mortgage loan commitment: With this type of loan commitment, the interest rate fluctuates over time based on market conditions, potentially resulting in varying monthly payments. 3. Government-backed mortgage loan commitment: These loan commitments are insured or guaranteed by government agencies such as the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA), offering favorable terms and requirements for eligible borrowers. 4. Jumbo mortgage loan commitment: This type of loan commitment is for loan amounts that exceed the conventional loan limits set by Fannie Mae and Freddie Mac. Jumbo loans typically have stricter requirements and higher interest rates due to their larger loan amounts. 5. Construction mortgage loan commitment: If a borrower intends to build a new residential property, they may require a construction loan commitment. This commitment ensures funding for the construction process and transitions into a regular mortgage once the property is complete. 6. Refinance mortgage loan commitment: When a borrower wants to replace their existing mortgage with a new loan, they may enter into a refinancing loan commitment. This commitment outlines the terms of the new loan, which may include a lower interest rate, different loan term, or cash-out options. It is essential for both borrowers and lenders to carefully review and understand the terms and conditions mentioned in the Arizona Receipt and Acceptance of Residential Mortgage Loan Commitment before signing. Consulting with a qualified mortgage professional or attorney may be advisable to ensure compliance with Arizona state laws and regulations.Arizona Receipt and Acceptance of Residential Mortgage Loan Commitment is a legal document used in the state of Arizona that verifies the borrower's receipt and acceptance of a mortgage loan commitment for a residential property. This document serves as a crucial step in the mortgage loan process and outlines the terms and conditions agreed upon by the borrower and the lender. The purpose of the Arizona Receipt and Acceptance of Residential Mortgage Loan Commitment is to establish a binding agreement between the borrower and the lender concerning the mortgage loan. By signing this document, the borrower acknowledges their understanding and acceptance of the loan commitment as well as their commitment to meet the specified terms and conditions. Keywords: Arizona, receipt, acceptance, residential mortgage loan commitment, legal document, borrower, lender, terms and conditions, binding agreement. Different types of Arizona Receipt and Acceptance of Residential Mortgage Loan Commitment include: 1. Fixed-rate mortgage loan commitment: This type of loan commitment offers a fixed interest rate over the life of the loan, providing borrowers with stability in their monthly payments. 2. Adjustable-rate mortgage loan commitment: With this type of loan commitment, the interest rate fluctuates over time based on market conditions, potentially resulting in varying monthly payments. 3. Government-backed mortgage loan commitment: These loan commitments are insured or guaranteed by government agencies such as the Federal Housing Administration (FHA) or the Department of Veterans Affairs (VA), offering favorable terms and requirements for eligible borrowers. 4. Jumbo mortgage loan commitment: This type of loan commitment is for loan amounts that exceed the conventional loan limits set by Fannie Mae and Freddie Mac. Jumbo loans typically have stricter requirements and higher interest rates due to their larger loan amounts. 5. Construction mortgage loan commitment: If a borrower intends to build a new residential property, they may require a construction loan commitment. This commitment ensures funding for the construction process and transitions into a regular mortgage once the property is complete. 6. Refinance mortgage loan commitment: When a borrower wants to replace their existing mortgage with a new loan, they may enter into a refinancing loan commitment. This commitment outlines the terms of the new loan, which may include a lower interest rate, different loan term, or cash-out options. It is essential for both borrowers and lenders to carefully review and understand the terms and conditions mentioned in the Arizona Receipt and Acceptance of Residential Mortgage Loan Commitment before signing. Consulting with a qualified mortgage professional or attorney may be advisable to ensure compliance with Arizona state laws and regulations.