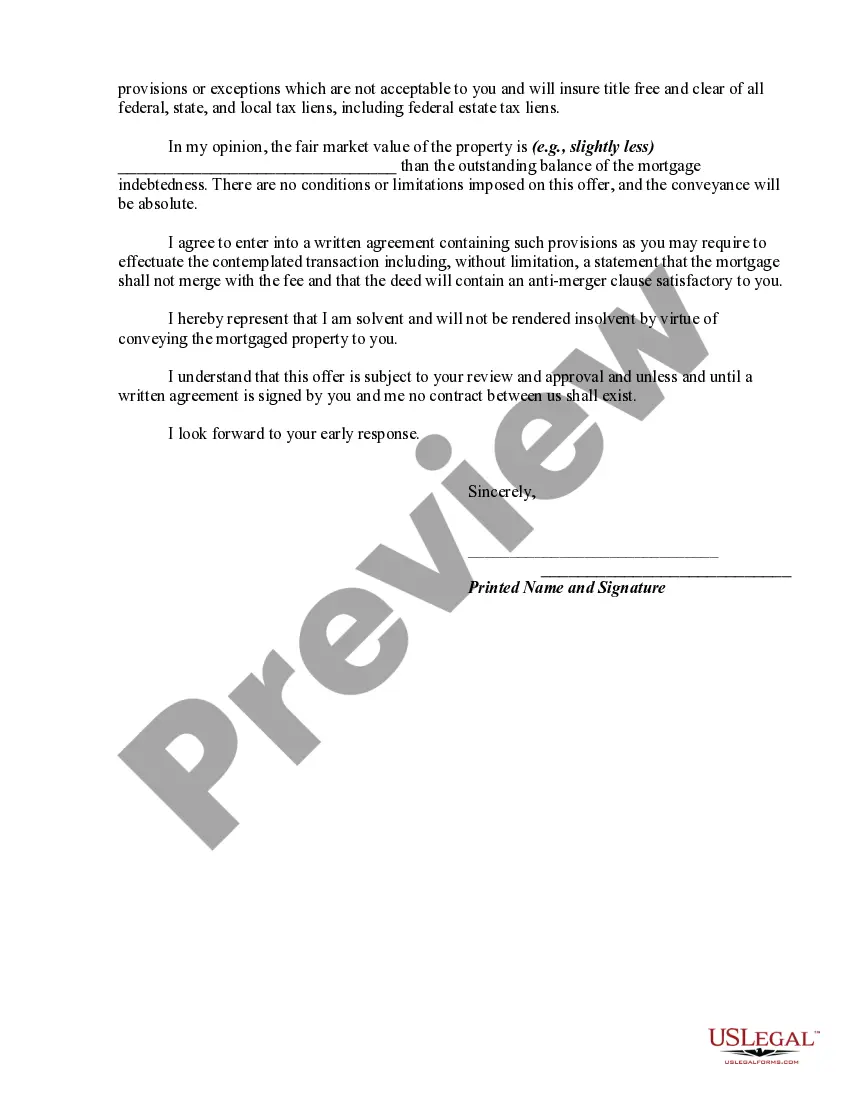

A deed in lieu of foreclosure is a method sometimes used by a lienholder on property to avoid a lengthy and expensive foreclosure process, with a deed in lieu of foreclosure a foreclosing lienholder agrees to have the ownership interest transferred to the bank/lienholder as payment in full. The debtor basically deeds the property to the bank instead of them paying for foreclosure proceedings. Therefore, if a debtor fails to make mortgage payments and the bank is about to foreclose on the property, the deed in lieu of foreclosure is an option that chooses to give the bank ownership of the property rather than having the bank use the legal process of foreclosure.

Arizona Offer by Borrower of Deed in Lieu of Foreclosure: A Comprehensive Guide When homeowners find themselves facing financial difficulties and are unable to meet their mortgage obligations, one of the options available to them in Arizona is to offer a deed in lieu of foreclosure to their lender. This alternative provides an opportunity for borrowers to avoid the lengthy and often daunting foreclosure process while also mitigating the potential damage to their credit. What is a Deed in Lieu of Foreclosure? A Deed in Lieu of Foreclosure (DIL) is a legal agreement in which the borrower voluntarily transfers the title of their property to the lender in exchange for the release of their mortgage debt. Essentially, the borrower conveys ownership of the property to the lender to satisfy the outstanding loan rather than going through the foreclosure process. A DIL is an option to be explored when other alternatives, such as loan modifications or short sales, have not been successful. Benefits of an Arizona Offer by Borrower of Deed in Lieu of Foreclosure: 1. Avoid Foreclosure: By choosing a DIL, homeowners can prevent the formal foreclosure process, which can be time-consuming, emotionally challenging, and come with significant costs. 2. Protect Credit Score: While a deed in lieu will still have an impact on the borrower's credit score, it is generally less severe than the damage caused by foreclosure. This allows homeowners to recover financially more quickly. 3. Relieve Debt: A successful DIL relieves the borrower of their mortgage debt obligation, putting an end to months or even years of financial strain. Types of Arizona Offers by Borrower of Deed in Lieu of Foreclosure: 1. Traditional Deed in Lieu: This involves the homeowner voluntarily surrendering the property to the lender without receiving any compensation. The lender gains ownership of the property, and the borrower is released from further mortgage obligations. 2. Cash for Keys: In some cases, lenders may offer financial incentives to borrowers in exchange for a deed in lieu. These incentives can help homeowners with relocation costs or finding alternative housing options. 3. Deficiency Waiver: In Arizona, lenders have the option to waive deficiency judgments against borrowers who opt for a DIL. A deficiency judgment is a court order that allows lenders to pursue borrowers for the remaining mortgage balance after the property is sold through foreclosure. 4. Agreement Modifications: Borrowers can negotiate specific terms with their lenders during the DIL process, such as the time frame in which they must vacate the property or any potential tax implications associated with the transfer of ownership. In conclusion, an Arizona Offer by Borrower of Deed in Lieu of Foreclosure provides homeowners with a viable alternative to foreclosure, allowing them to alleviate their financial burden while mitigating some damage to their credit. By understanding the various types of DIL arrangements available and consulting with legal and financial advisors, borrowers can make informed decisions to best suit their individual circumstances.Arizona Offer by Borrower of Deed in Lieu of Foreclosure: A Comprehensive Guide When homeowners find themselves facing financial difficulties and are unable to meet their mortgage obligations, one of the options available to them in Arizona is to offer a deed in lieu of foreclosure to their lender. This alternative provides an opportunity for borrowers to avoid the lengthy and often daunting foreclosure process while also mitigating the potential damage to their credit. What is a Deed in Lieu of Foreclosure? A Deed in Lieu of Foreclosure (DIL) is a legal agreement in which the borrower voluntarily transfers the title of their property to the lender in exchange for the release of their mortgage debt. Essentially, the borrower conveys ownership of the property to the lender to satisfy the outstanding loan rather than going through the foreclosure process. A DIL is an option to be explored when other alternatives, such as loan modifications or short sales, have not been successful. Benefits of an Arizona Offer by Borrower of Deed in Lieu of Foreclosure: 1. Avoid Foreclosure: By choosing a DIL, homeowners can prevent the formal foreclosure process, which can be time-consuming, emotionally challenging, and come with significant costs. 2. Protect Credit Score: While a deed in lieu will still have an impact on the borrower's credit score, it is generally less severe than the damage caused by foreclosure. This allows homeowners to recover financially more quickly. 3. Relieve Debt: A successful DIL relieves the borrower of their mortgage debt obligation, putting an end to months or even years of financial strain. Types of Arizona Offers by Borrower of Deed in Lieu of Foreclosure: 1. Traditional Deed in Lieu: This involves the homeowner voluntarily surrendering the property to the lender without receiving any compensation. The lender gains ownership of the property, and the borrower is released from further mortgage obligations. 2. Cash for Keys: In some cases, lenders may offer financial incentives to borrowers in exchange for a deed in lieu. These incentives can help homeowners with relocation costs or finding alternative housing options. 3. Deficiency Waiver: In Arizona, lenders have the option to waive deficiency judgments against borrowers who opt for a DIL. A deficiency judgment is a court order that allows lenders to pursue borrowers for the remaining mortgage balance after the property is sold through foreclosure. 4. Agreement Modifications: Borrowers can negotiate specific terms with their lenders during the DIL process, such as the time frame in which they must vacate the property or any potential tax implications associated with the transfer of ownership. In conclusion, an Arizona Offer by Borrower of Deed in Lieu of Foreclosure provides homeowners with a viable alternative to foreclosure, allowing them to alleviate their financial burden while mitigating some damage to their credit. By understanding the various types of DIL arrangements available and consulting with legal and financial advisors, borrowers can make informed decisions to best suit their individual circumstances.