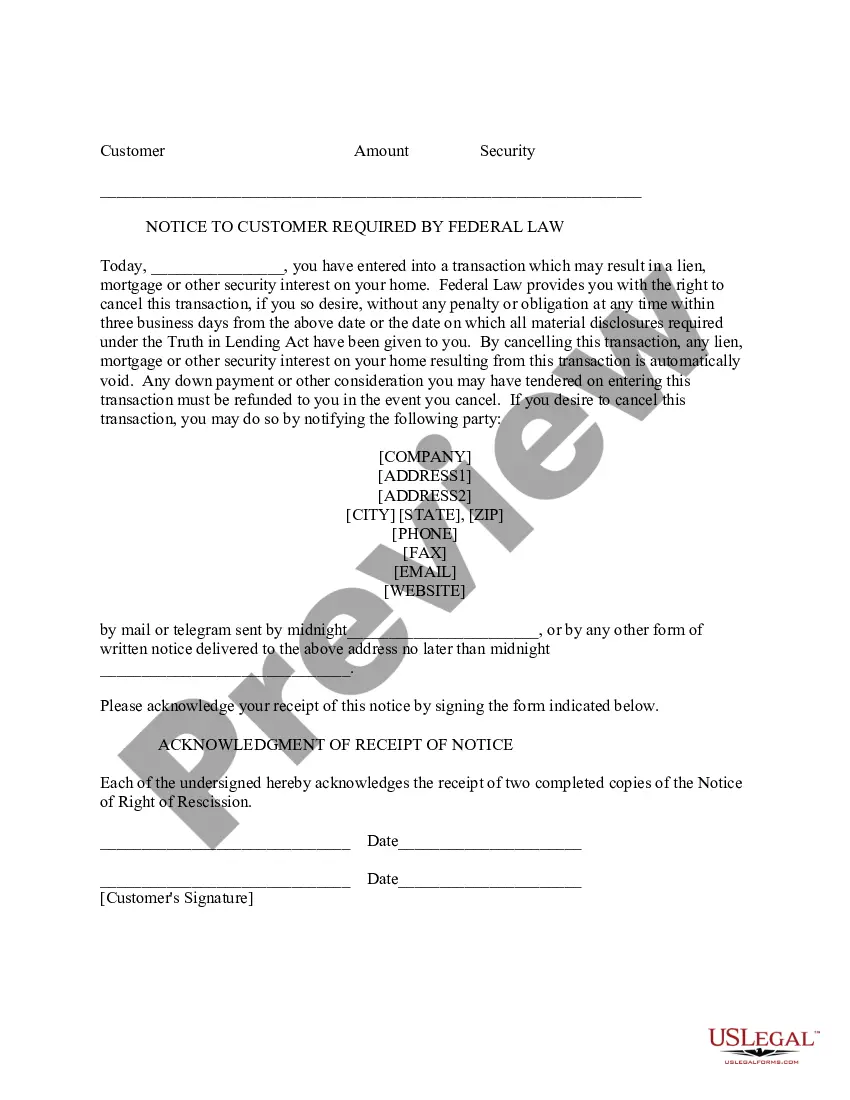

The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. TILA applies only to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use. This form was designed to cover an situation where the Seller is not a creditor as defined by the TILA.

Arizona Installment Sale not covered by Federal Consumer Credit Protection Act with Security Agreement refers to a type of lending agreement in Arizona that falls outside the purview of the Federal Consumer Credit Protection Act (CCPA) and involves the provision of a security agreement. The Federal Consumer Credit Protection Act (CCPA), including the Truth in Lending Act (TILL) and the Consumer Leasing Act (CLA), provides important protections to consumers engaging in various types of credit transactions. However, in Arizona, certain installment sale agreements are exempt from these federal regulations. One type of Arizona Installment Sale not covered by the Federal Consumer Credit Protection Act with Security Agreement is the sale of goods or services by a limited number of sellers that do not typically engage in consumer lending practices. These sellers may include small-scale local businesses that extend credit to their customers, commonly seen in transactions involving the sale of furniture, electronics, or household appliances. Given their limited scope and occasional lending practices, these sellers do not fall under the jurisdiction of federal consumer protection laws. Another type of Arizona Installment Sale not covered by the Federal Consumer Credit Protection Act with Security Agreement is the sale of real estate. When individuals or entities enter into installment sale agreements for the purchase of real estate properties in Arizona, these agreements are not bound by the federal consumer credit protection regulations. Instead, the transaction is governed by Arizona state laws and regulations relating to real estate transactions. In such Arizona Installment Sale agreements, the inclusion of a security agreement further protects the seller's interest in the event of default by the buyer. The security agreement allows the seller to take possession of the purchased goods or assets, such as the furniture, electronic devices, or real estate, should the buyer fail to meet the agreed-upon payment obligations. It is essential for both buyers and sellers engaging in Arizona Installment Sale agreements that are not covered by the Federal Consumer Credit Protection Act with Security Agreement to ensure they understand the specific terms and conditions of the agreement. This includes the repayment schedule, interest rates, late payment penalties, and the consequences of default specified in the security agreement. By being aware of the exemptions in place for these types of installment sale agreements in Arizona, buyers and sellers can engage in transactions with a clear understanding of their rights and obligations. Furthermore, it is advisable for parties involved to seek legal counsel or consult relevant state laws to ensure compliance and understand the nuances of such agreements.