The business typically owns the policy, pays the premiums, and is the beneficiary. Most businesses purchase key-person insurance as a permanent life insurance policy; however, term life insurance may be less expensive and can be bought to cover the key person until he or she retires. The policy can be then transferred to the departing employee as a retirement benefit or to a different key person, upon the retirement of the original key person.

Key-person insurance benefits are often used to buy out the insured person's shares or interest in the company. Buy-sell agreements, which require the deceased executive's estate to sell its stock to the remaining shareholders, legally facilitate this process. Proceeds from key-person insurance can also be used to recruit replacement management.

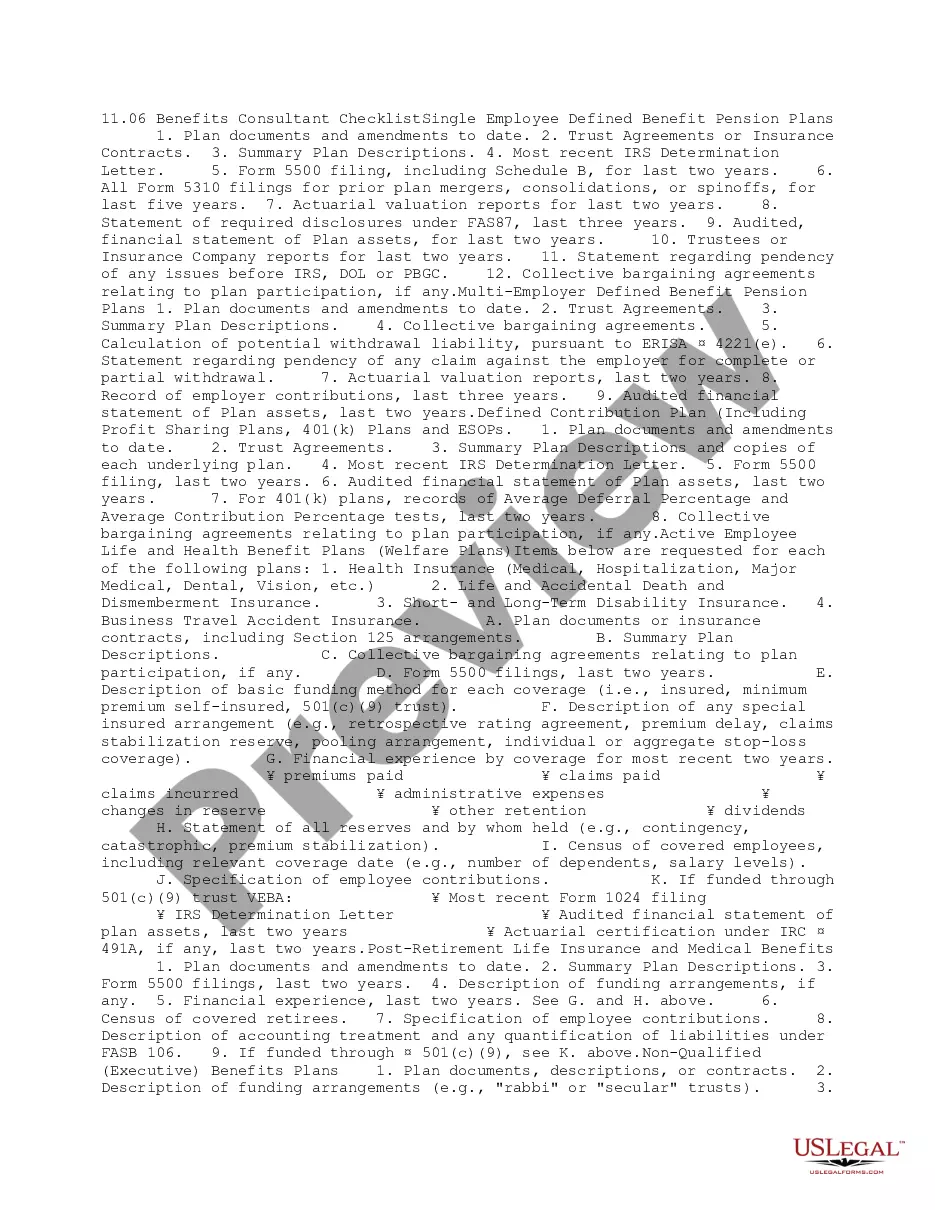

The following form contains some critical questions you should ask your agent or broker when considering this type of insurance.

Arizona Checklist - Key Employee Life Insurance

Instant download

Description

How to fill out Checklist - Key Employee Life Insurance?

Are you currently situated in a location where you need documents for occasional business or personal activities every day.

There is a variety of legitimate document templates available online, but finding ones you can trust is not easy.

US Legal Forms offers a multitude of form templates, including the Arizona Checklist - Key Employee Life Insurance, that are designed to comply with state and federal regulations.

After you find the correct form, click Purchase now.

Choose your preferred pricing plan, fill in the required information to create your account, and complete the purchase using PayPal or a credit card.

- If you are already familiar with the US Legal Forms website and have an account, simply Log In.

- Then, you can download the Arizona Checklist - Key Employee Life Insurance template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Obtain the form you need and ensure it is for the correct city/state.

- Utilize the Review option to examine the form.

- Read the details to confirm you have selected the right form.

- If the form does not meet your expectations, use the Search box to find the form that suits your needs.

Form popularity

FAQ

An example of key person life insurance would be a policy taken out on a company founder or CEO, who plays a crucial role in the business's success. If this individual were to pass away, the insurance payout could help cover the transition period and any losses incurred. This practice helps ensure the organization remains on solid ground. For further guidance, review the Arizona Checklist - Key Employee Life Insurance.

Key employee life insurance is a policy that provides financial protection to a business in the event of the loss of a vital employee. This insurance helps cover financial losses and ensures business continuity. By holding this insurance, a business can safeguard its operations and maintain stability. For further insights, check the Arizona Checklist - Key Employee Life Insurance.

The three types of life insurance often provided to employees include term life insurance, whole life insurance, and universal life insurance. Each type caters to different financial needs and preferences. It's essential to evaluate which type best aligns with your company's goals and the well-being of your employees. Discover more in the Arizona Checklist - Key Employee Life Insurance.

Insurance for key employees is designed to protect a business from financial loss resulting from the death of essential personnel. This insurance can cover lost income, recruiting expenses, and other financial impacts. It gives business owners peace of mind, knowing they have a safety net in place. You can explore the Arizona Checklist - Key Employee Life Insurance for specifics.

The most common type of life insurance used for key employee indemnification is typically a term life insurance policy. This policy provides coverage for a specific period, which aligns with the business's needs. In doing so, the company can ensure that it has financial support in case of the untimely loss of a key employee. Consider referencing the Arizona Checklist - Key Employee Life Insurance for more details.

Accessing your life insurance policy typically involves contacting your insurance provider directly. They can guide you through the process of retrieving your policy documents. You may also have the option to access your policy through an online account if you registered one. For further steps, check out USLegalForms to streamline your experience with your Arizona Checklist - Key Employee Life Insurance.

To obtain Keyman insurance, businesses should first identify the key employees they want to insure and evaluate the coverage amount necessary for protecting their financial interests. After gathering this information, reach out to a trustworthy insurance agent or company offering Keyman insurance policies. Utilizing resources like USLegalForms can help simplify the process of obtaining your Arizona Checklist - Key Employee Life Insurance.

No, individuals cannot take out life insurance on someone else without their consent. The insured person must provide written approval, which indicates their understanding and agreement to the policy. It's important to be aware of this rule to avoid potential legal issues related to Arizona Checklist - Key Employee Life Insurance. Always ensure clear communication regarding any life insurance policies.

Typically, term life insurance and permanent life insurance, like whole life or universal life, are used for key employee needs. These policies provide financial protection to the business in case of a key employee's death, ensuring continuity. Understanding the differences helps businesses choose the right coverage for their Arizona Checklist - Key Employee Life Insurance. You can easily compare options through platforms like USLegalForms.

To access your life insurance policy, you should first contact your insurance provider. They may require your policy number and identification to verify your identity. Once confirmed, you can request copies of your policy documents or access them through their online portal. For more assistance, consider using the resources available on USLegalForms, which can guide you in managing your Arizona Checklist - Key Employee Life Insurance.