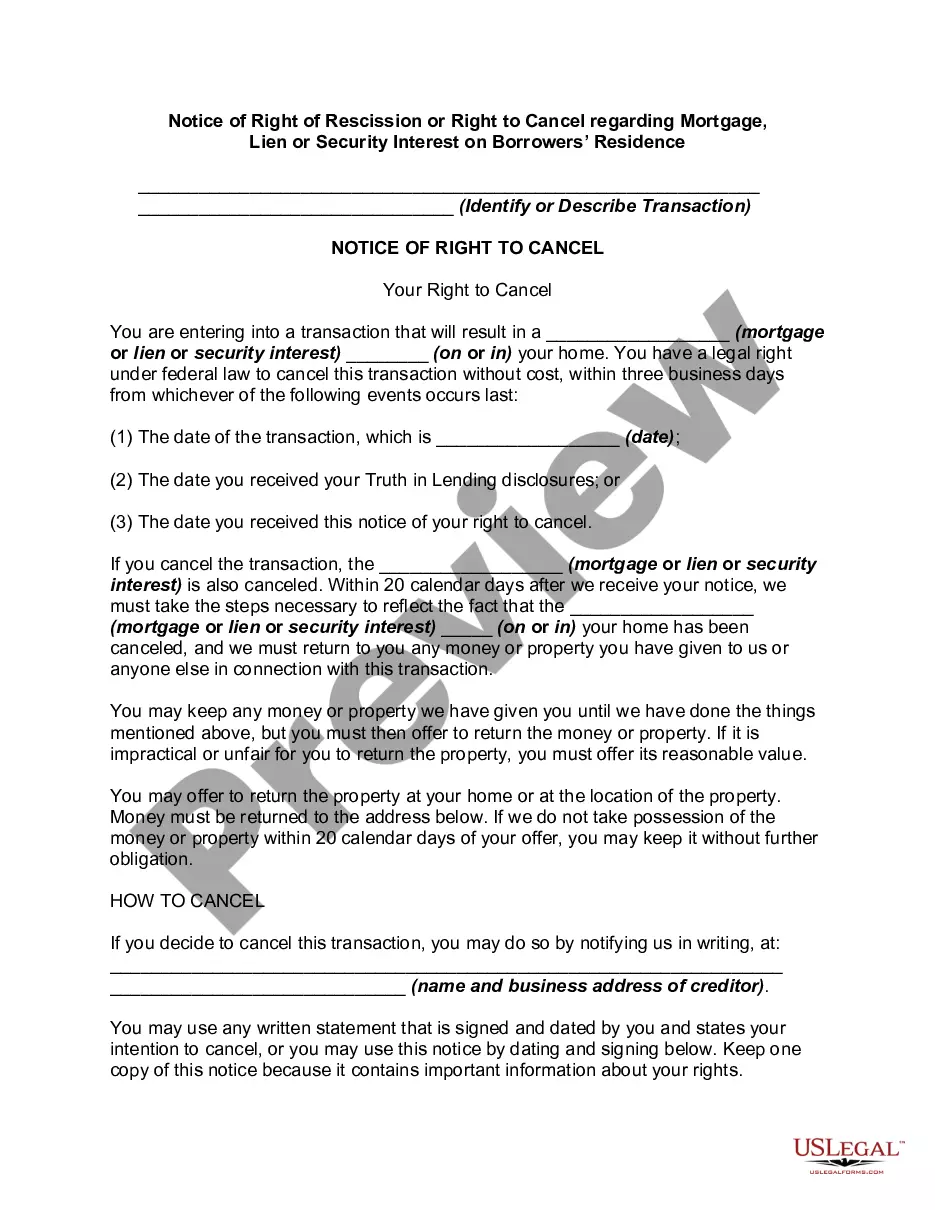

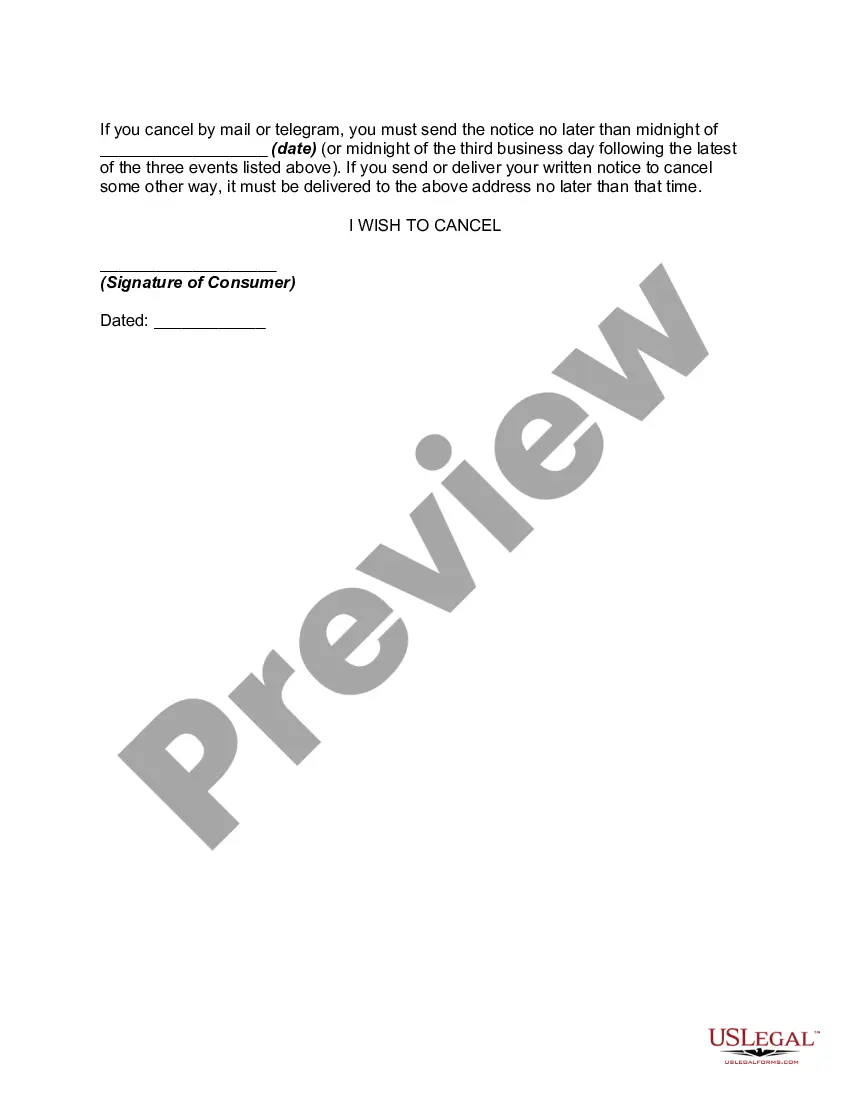

According to 12 CFR 226.23, in a credit transaction in which a security interest is or will be retained or acquired in a consumer's principal dwelling, each consumer whose ownership interest is or will be subject to the security interest shall have the right to rescind the transaction, with some exceptions. To exercise the right to rescind, the consumer shall notify the creditor of the rescission by mail, telegram or other means of written communication. Notice is considered given when mailed, when filed for telegraphic transmission or, if sent by other means, when delivered to the creditor's designated place of business. The consumer may exercise the right to rescind until midnight of the third business day following consummation, delivery of the notice required by paragraph (b) of this section, or delivery of all material disclosures, whichever occurs last.

Title: Understanding Arizona's Notice of Right of Rescission or Right to Cancel: A Comprehensive Guide for Borrowers Introduction: In Arizona, the Notice of Right of Rescission or Right to Cancel plays a crucial role in protecting borrowers who have secured a mortgage, lien, or security interest on their residence. This notice grants borrowers the opportunity to rescind or cancel their loan agreement within a specific timeframe, allowing them to reconsider their borrowing decision without penalty. This article aims to provide a detailed description of the Arizona Notice of Right of Rescission or Right to Cancel, its purpose, and any relevant variations that may apply. Keywords: Arizona, Notice of Right of Rescission, Right to Cancel, Mortgage, Lien, Security Interest, Borrowers, Residence, Loan Agreement, Reconsider, Penalties. 1. Purpose and Importance of the Notice: The Notice of Right of Rescission or Right to Cancel is designed to protect borrowers and provide them with a cooling-off period to reconsider their mortgage, lien, or security interest on their residence. This notice ensures that borrowers are well-informed about their rights and the potential consequences of their financial commitments. 2. Default Arizona Notice of Right of Rescission or Right to Cancel: The default Notice of Right of Rescission or Right to Cancel period in Arizona is typically three business days, excluding Sundays and legal holidays. This timeframe allows borrowers to review their loan agreement and make an informed decision concerning their obligations. 3. Special Situations: a) Extended Right to Cancel: Under certain circumstances, borrowers may be entitled to an extended period beyond the default three-day window. This extension often occurs when the lender fails to provide the necessary disclosures or notifications required by law. b) Customization by Lenders: Some lenders may choose to provide borrowers with an extended right to cancel, exceeding the default period. It is essential for borrowers to carefully review their loan agreement to understand if any such provisions apply. c) Non-Purchase Money Mortgages: The Notice of Right of Rescission or Right to Cancel also applies to non-purchase money mortgages, such as refinancing or home equity loans. It is crucial for borrowers to understand that the right to cancel still exists in these types of mortgage transactions. 4. Compliance and Penalties: Lenders are legally obligated to provide borrowers with the Notice of Right of Rescission or Right to Cancel in a timely and accurate manner. Failure to comply with these requirements may result in penalties for the lender, potentially allowing the borrower to rescind the loan agreement beyond the initial cancellation period. Conclusion: The Arizona Notice of Right of Rescission or Right to Cancel plays a vital role in safeguarding borrowers' interests when securing a mortgage, lien, or security interest on their residence. Being aware of this notice empowers borrowers to make well-informed decisions concerning their financial commitments. It is crucial for borrowers to thoroughly read and understand their loan agreement, seeking professional legal advice if necessary, to ensure their rights are protected throughout the borrowing process.Title: Understanding Arizona's Notice of Right of Rescission or Right to Cancel: A Comprehensive Guide for Borrowers Introduction: In Arizona, the Notice of Right of Rescission or Right to Cancel plays a crucial role in protecting borrowers who have secured a mortgage, lien, or security interest on their residence. This notice grants borrowers the opportunity to rescind or cancel their loan agreement within a specific timeframe, allowing them to reconsider their borrowing decision without penalty. This article aims to provide a detailed description of the Arizona Notice of Right of Rescission or Right to Cancel, its purpose, and any relevant variations that may apply. Keywords: Arizona, Notice of Right of Rescission, Right to Cancel, Mortgage, Lien, Security Interest, Borrowers, Residence, Loan Agreement, Reconsider, Penalties. 1. Purpose and Importance of the Notice: The Notice of Right of Rescission or Right to Cancel is designed to protect borrowers and provide them with a cooling-off period to reconsider their mortgage, lien, or security interest on their residence. This notice ensures that borrowers are well-informed about their rights and the potential consequences of their financial commitments. 2. Default Arizona Notice of Right of Rescission or Right to Cancel: The default Notice of Right of Rescission or Right to Cancel period in Arizona is typically three business days, excluding Sundays and legal holidays. This timeframe allows borrowers to review their loan agreement and make an informed decision concerning their obligations. 3. Special Situations: a) Extended Right to Cancel: Under certain circumstances, borrowers may be entitled to an extended period beyond the default three-day window. This extension often occurs when the lender fails to provide the necessary disclosures or notifications required by law. b) Customization by Lenders: Some lenders may choose to provide borrowers with an extended right to cancel, exceeding the default period. It is essential for borrowers to carefully review their loan agreement to understand if any such provisions apply. c) Non-Purchase Money Mortgages: The Notice of Right of Rescission or Right to Cancel also applies to non-purchase money mortgages, such as refinancing or home equity loans. It is crucial for borrowers to understand that the right to cancel still exists in these types of mortgage transactions. 4. Compliance and Penalties: Lenders are legally obligated to provide borrowers with the Notice of Right of Rescission or Right to Cancel in a timely and accurate manner. Failure to comply with these requirements may result in penalties for the lender, potentially allowing the borrower to rescind the loan agreement beyond the initial cancellation period. Conclusion: The Arizona Notice of Right of Rescission or Right to Cancel plays a vital role in safeguarding borrowers' interests when securing a mortgage, lien, or security interest on their residence. Being aware of this notice empowers borrowers to make well-informed decisions concerning their financial commitments. It is crucial for borrowers to thoroughly read and understand their loan agreement, seeking professional legal advice if necessary, to ensure their rights are protected throughout the borrowing process.