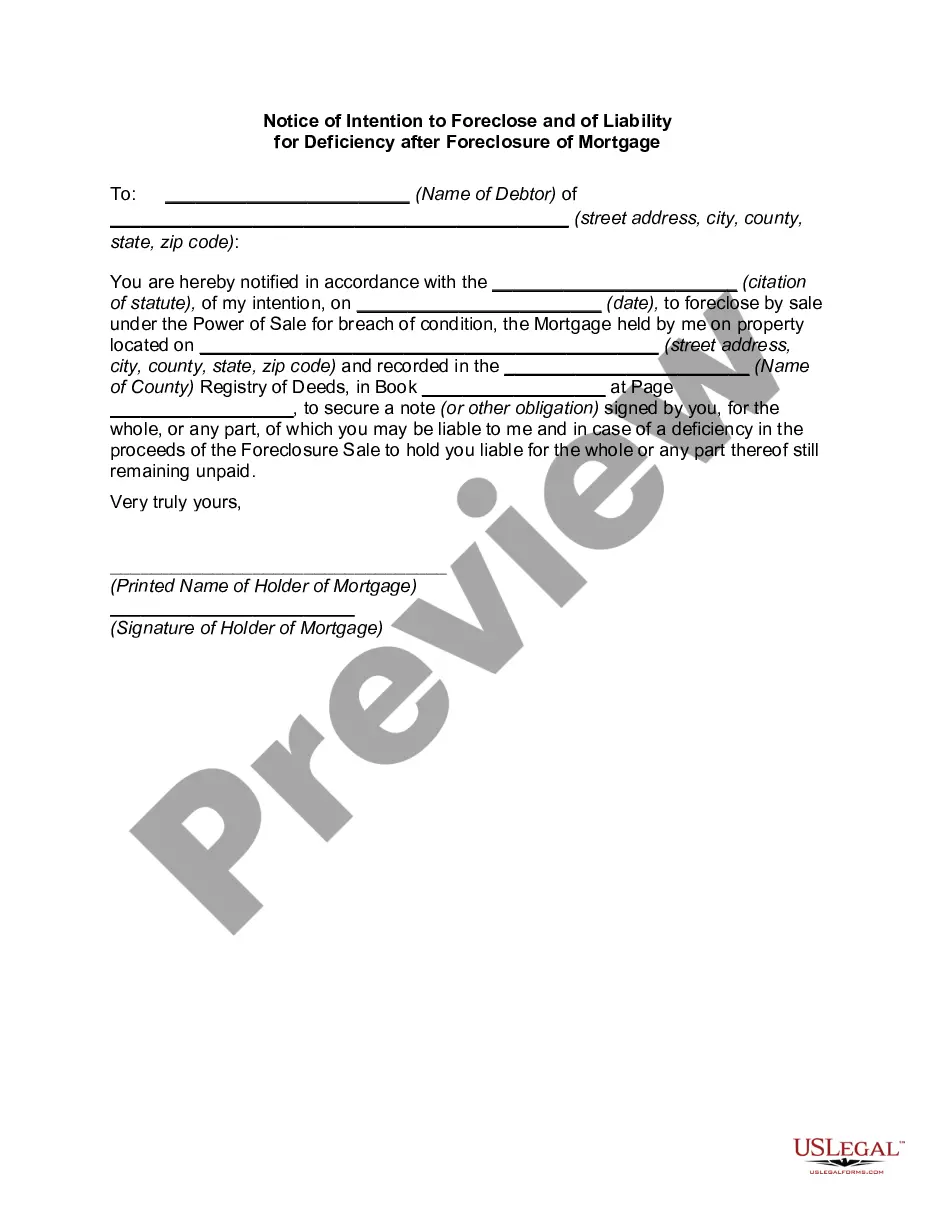

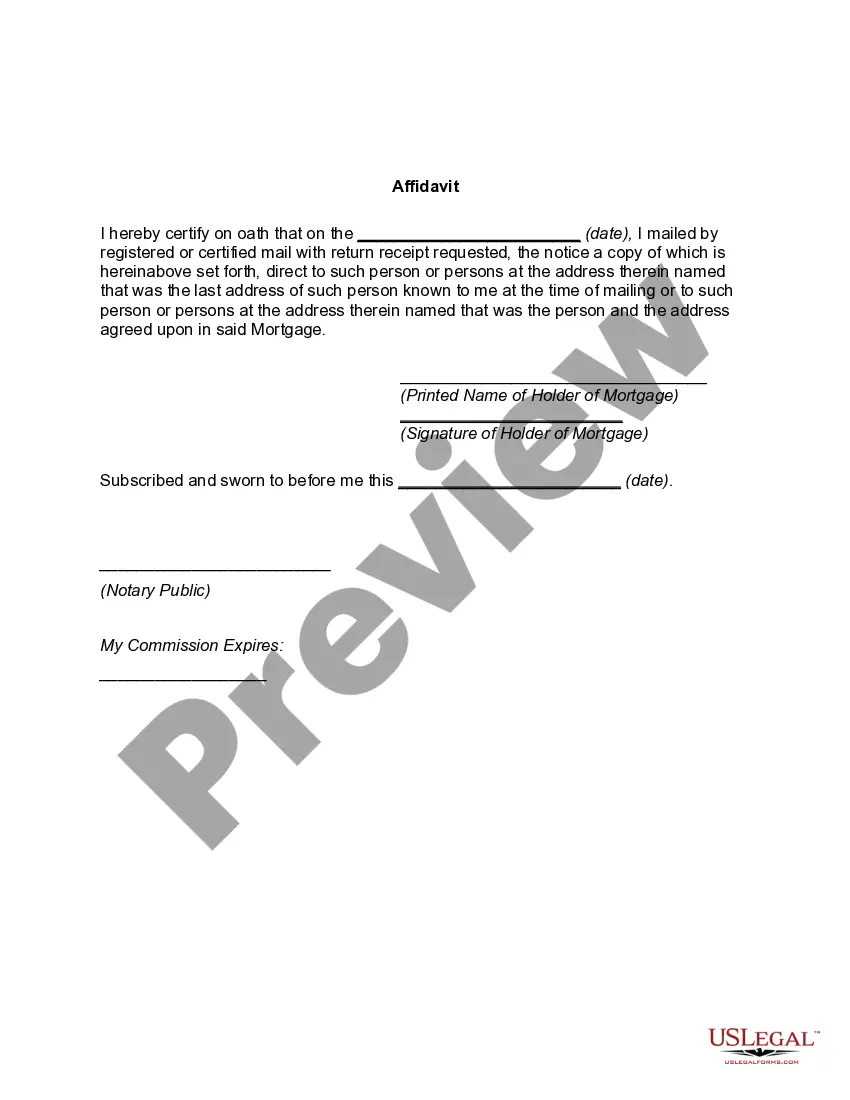

Title: Understanding the Arizona Notice of Intention to Foreclose and Liability for Deficiency after Mortgage Foreclosure Introduction: The legal process surrounding mortgage foreclosure can be complex and daunting for homeowners. In Arizona, the Notice of Intention to Foreclose (NOI) and Liability for Deficiency after Foreclosure are crucial documents that homeowners need to understand. This article aims to provide a detailed description of these notices, their implications, and any variations that may exist. 1. Arizona Notice of Intention to Foreclose: The Arizona Notice of Intention to Foreclose serves as an official notice to homeowners that their mortgage lender intends to initiate foreclosure proceedings against them. This document outlines the time frame within which the foreclosure process will commence. It typically includes important details such as the lender's contact information, the homeowner's loan details, and a statement of default. Types of Arizona Notice of Intention to Foreclose: a) Preliminary Notice of Intent to Foreclose: This notice is typically sent by the lender to the homeowner before filing an actual foreclosure action. It serves as a warning or an opportunity for the homeowner to take corrective actions before the process moves forward. b) Final Notice of Intent to Foreclose: If the homeowner fails to address the default or reach a resolution after receiving the preliminary notice, the lender will issue a final notice. This notice signifies the lender's intent to proceed with the foreclosure process unless the homeowner takes immediate action. 2. Liability for Deficiency after Foreclosure of Mortgage: After a mortgage foreclosure sale in Arizona, there may be a difference between the sale price of the property and the outstanding loan balance. The Liability for Deficiency refers to the homeowner's responsibility for this deficiency amount, which the lender can pursue through legal means if allowed by law. Types of Liability for Deficiency after Foreclosure: a) Recourse Mortgage: If the mortgage is classified as a recourse mortgage, the lender retains the right to pursue the homeowner for the deficiency, even after the property is foreclosed and sold at auction. b) Non-Recourse Mortgage: In the case of a non-recourse mortgage, Arizona law generally limits the lender's ability to pursue the homeowner for a deficiency. This means that once the property is sold, the lender cannot seek further compensation from the homeowner. Conclusion: Understanding the Arizona Notice of Intention to Foreclose and Liability for Deficiency after Foreclosure of Mortgage is crucial for homeowners facing foreclosure. It is important to receive legal guidance in interpreting and responding to these notices adequately. Homeowners should consult with an experienced real estate attorney to ensure they are aware of their rights, options, and potential liability amid the foreclosure process in Arizona.

Arizona Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage

Description

How to fill out Arizona Notice Of Intention To Foreclose And Of Liability For Deficiency After Foreclosure Of Mortgage?

If you need to complete, obtain, or produce lawful file templates, use US Legal Forms, the greatest assortment of lawful varieties, which can be found on the web. Make use of the site`s basic and convenient search to find the paperwork you require. Numerous templates for business and personal purposes are sorted by groups and suggests, or keywords and phrases. Use US Legal Forms to find the Arizona Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage in a number of clicks.

If you are presently a US Legal Forms buyer, log in to your bank account and then click the Down load switch to get the Arizona Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage. You can even gain access to varieties you previously delivered electronically within the My Forms tab of your bank account.

Should you use US Legal Forms the first time, refer to the instructions listed below:

- Step 1. Be sure you have selected the form to the appropriate city/region.

- Step 2. Take advantage of the Review choice to look over the form`s articles. Never overlook to read the outline.

- Step 3. If you are not satisfied together with the develop, use the Lookup field on top of the display screen to get other models in the lawful develop format.

- Step 4. Upon having discovered the form you require, click the Acquire now switch. Opt for the rates prepare you choose and add your references to sign up for the bank account.

- Step 5. Procedure the purchase. You can use your charge card or PayPal bank account to complete the purchase.

- Step 6. Choose the structure in the lawful develop and obtain it on the product.

- Step 7. Total, change and produce or indicator the Arizona Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage.

Every lawful file format you purchase is the one you have for a long time. You might have acces to every develop you delivered electronically within your acccount. Click on the My Forms portion and select a develop to produce or obtain again.

Be competitive and obtain, and produce the Arizona Notice of Intention to Foreclose and of Liability for Deficiency after Foreclosure of Mortgage with US Legal Forms. There are millions of skilled and state-distinct varieties you may use for the business or personal needs.