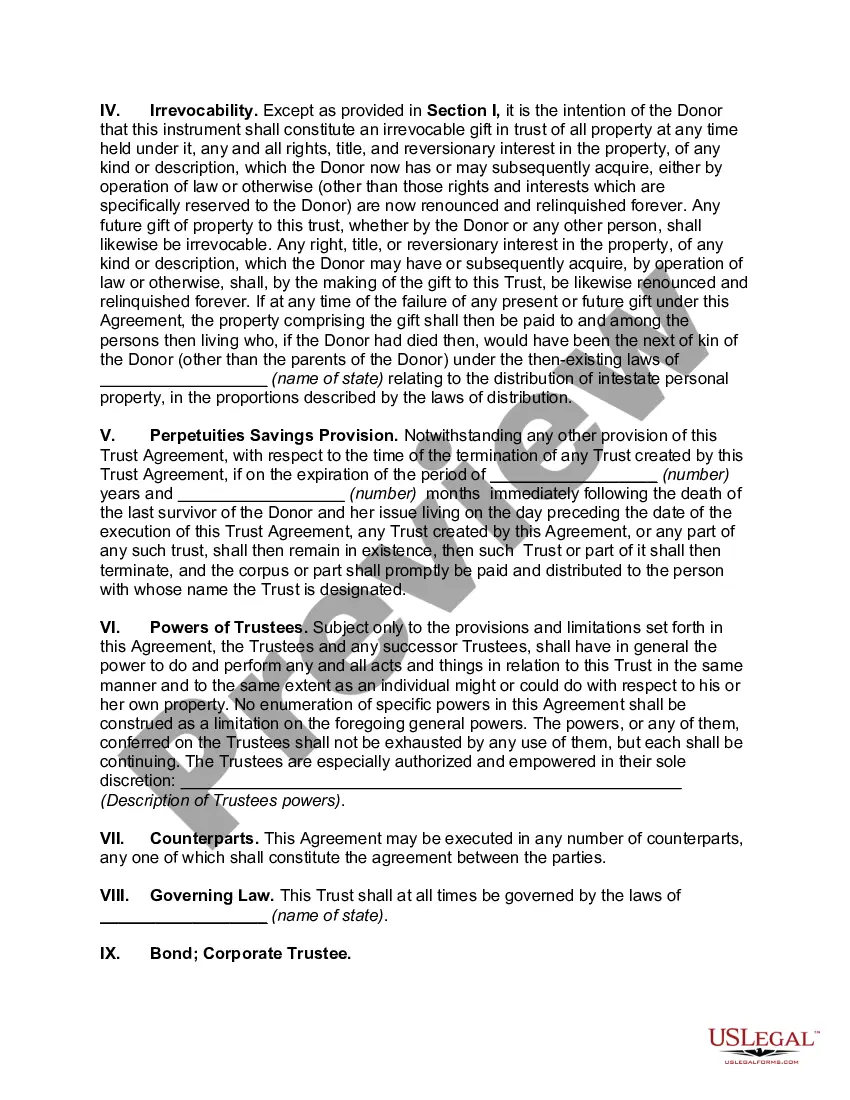

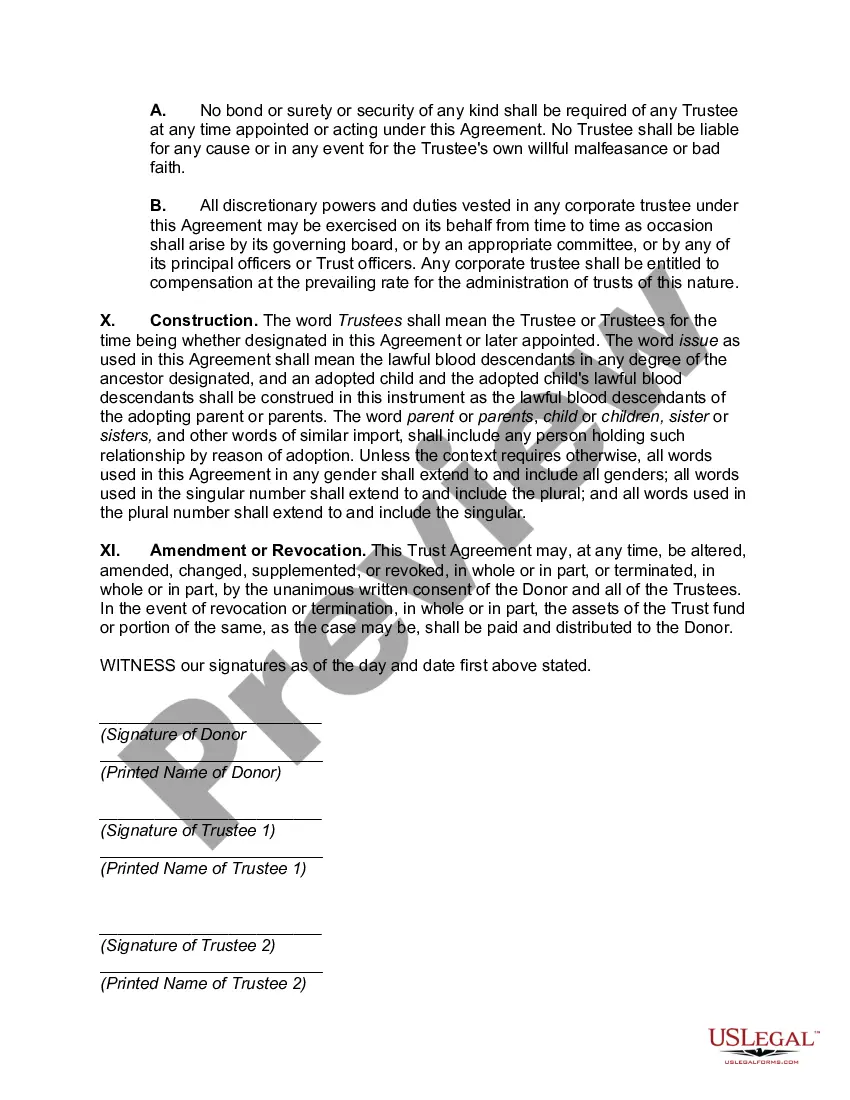

Arizona Granter Retained Income Trust with Division into Trusts for Issue after Term of Years is a legal instrument that allows individuals in Arizona to transfer assets to a trust while retaining an income interest for a specified number of years. This estate planning tool offers several advantages, including potential tax savings, asset protection, and the ability to provide for future generations. The Arizona Granter Retained Income Trust (GRIT) with Division into Trusts for Issue after Term of Years is structured in such a way that the granter transfers assets into the trust and receives income from those assets for a predetermined period. At the end of this term, the trust assets are distributed to named beneficiaries, typically the granter's children or other designated heirs. The income received by the granter during the initial term may be either a fixed percentage or a unit rust payment, which is calculated annually based on the trust's value. One key feature of the Arizona GRIT with Division into Trusts for Issue after Term of Years is its division into separate trusts upon the expiration of the initial term. This division allows the granter to distribute the trust assets among multiple descendants or heirs, each placed in a separate trust. By dividing the assets into individual trusts, the granter can ensure each beneficiary has control over their respective share, tailored to their specific needs and circumstances. The Arizona Granter Retained Income Trust with Division into Trusts for Issue after Term of Years provides several advantages for both the granter and the beneficiaries. As the granter, the trust allows one to remove assets from their estate, potentially minimizing estate taxes. It also provides a steady income stream during the initial term, while still allowing for asset appreciation within the trust. The division of the trust into separate trusts also offers flexibility in tailoring the distribution to meet the beneficiaries' individual needs, such as protecting assets from creditors or providing for special needs. Some variations and alternatives to the Arizona GRIT with Division into Trusts for Issue after Term of Years include the Delaware Incomplete Non-Grantor Trust (DING), the Nevada Dynasty Trust, and the Delaware Dynasty Trust. These trusts share similarities with Arizona Grits but may offer different advantages depending on the granter's specific goals and circumstances. It is crucial to seek professional advice from an attorney or financial advisor experienced in estate planning to determine which trust structure best suits individual needs. Overall, the Arizona Granter Retained Income Trust with Division into Trusts for Issue after Term of Years is a comprehensive estate planning tool that allows individuals to retain income from assets for a specific period while providing for their heirs and potentially minimizing estate taxes. It offers flexibility, protection, and tax advantages, making it a popular choice for those seeking a strategic approach to wealth transfer in Arizona.

Arizona Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years

Description

How to fill out Arizona Grantor Retained Income Trust With Division Into Trusts For Issue After Term Of Years?

Choosing the right legal papers web template could be a battle. Of course, there are plenty of layouts available on the net, but how can you discover the legal kind you want? Use the US Legal Forms internet site. The assistance gives a huge number of layouts, for example the Arizona Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years, that you can use for business and private needs. Every one of the forms are examined by specialists and fulfill federal and state demands.

In case you are presently signed up, log in in your bank account and then click the Acquire button to have the Arizona Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years. Make use of bank account to check from the legal forms you have purchased previously. Visit the My Forms tab of the bank account and have yet another backup in the papers you want.

In case you are a brand new consumer of US Legal Forms, here are simple recommendations for you to adhere to:

- Initial, be sure you have chosen the correct kind for your personal area/area. You are able to check out the shape making use of the Review button and read the shape description to make certain this is basically the best for you.

- In the event the kind is not going to fulfill your expectations, take advantage of the Seach area to discover the appropriate kind.

- When you are certain that the shape is acceptable, go through the Buy now button to have the kind.

- Select the prices strategy you want and type in the required info. Create your bank account and pay for the transaction utilizing your PayPal bank account or Visa or Mastercard.

- Choose the submit file format and acquire the legal papers web template in your device.

- Comprehensive, modify and print and signal the attained Arizona Grantor Retained Income Trust with Division into Trusts for Issue after Term of Years.

US Legal Forms is definitely the biggest local library of legal forms where you will find numerous papers layouts. Use the company to acquire expertly-made files that adhere to condition demands.

Form popularity

FAQ

Commonly referred to as the 21 year rule, the rule deems certain types of trusts to dispose of their capital property and recognize the accrued gains every 21 years. Without this rule, trusts could be used to defer the realization of a capital gain for more than 21 years (80 years in BC).

Key Takeaways. A 5 by 5 Power in Trust is a clause that lets the beneficiary make withdrawals from the trust on a yearly basis. The beneficiary can cash out $5,000 or 5% of the trust's fair market value each year, whichever is a higher amount.

You must agree with all of the other trustees when making trust decisions. So it's worth understanding who they are and deciding if you think the relationship will work.

Under Section 663(b) of the Internal Revenue Code, any distribution by an estate or trust within the first 65 days of the tax year can be treated as having been made on the last day of the preceding tax year.

Year Trust, also known as a Legacy Trust or Medicaid Asset Protection Trust, can be established to protect assets from being spent down on long term care in a nursing home. The assets you place in the Legacy Trust will become exempt from the Medicaid spend down requirements after a 5 year look back period.

The term partition is usually applied to a division of assets between the life tenant and the remaindermen beneficiaries (thus bringing the trust to an end). It can also refer to splitting a trust into separate funds, which then operate independently under new trusts (and may have different beneficiaries and trustees).

When a trust is irrevocable but some or all of the trust can be disbursed to or for the benefit of the individual, the look-back period applying to disbursements which could be made to or for the individual but are made to another person or persons is 36 months.

If the trust was divided into fractional shares, the trust allocation is updated by recalculating the fraction each time distributions are made, as well as each time income is allocated to principal.

A trust can remain open for up to 21 years after the death of anyone living at the time the trust is created, but most trusts end when the trustor dies and the assets are distributed immediately.

At the end of the initial term retained by the Grantor, if the Grantor is still living, the remainder beneficiaries (or a trust to be administered for the benefit of the remainder beneficiaries) receive $100,0000 plus all capital growth (which is the amount over and above the net income that was paid to the Grantor).