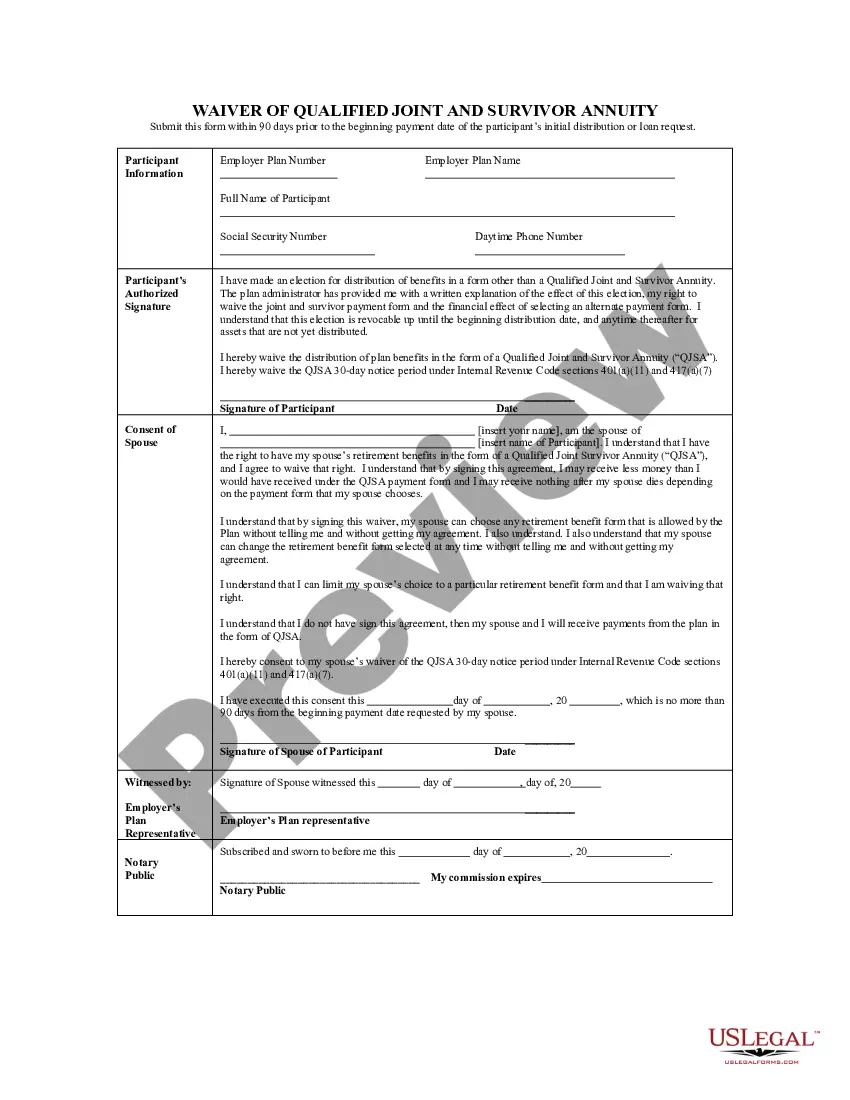

The Arizona Waiver of Qualified Joint and Survivor Annuity (JSA) is a legal provision that allows retirement plan participants to waive the required survivor benefits for their designated spouse or beneficiary. This waiver provides the participant with greater flexibility in managing their pension assets and allows them to receive higher pension payments during their lifetime. In Arizona, there are two main types of waivers related to the JSA: 1. Arizona Full Waiver of JSA: This type of waiver completely relinquishes the participant's obligation to provide any form of joint and survivor annuity for their spouse or beneficiary. By choosing this waiver, the participant ensures that they receive the maximum pension benefit available during their lifetime, but it also means that no survivor benefits will be payable upon their death. It is crucial to consider the implications of this type of waiver, as it effectively severs any future financial protection for the spouse or beneficiary. 2. Arizona Partial Waiver of JSA: Unlike the full waiver, the partial waiver allows the participant to provide a reduced survivor benefit for their spouse or beneficiary while maximizing their own pension payments. With this option, the participant can choose a specific percentage of the survivor benefit amount to be paid upon their death, such as 25% or 50%. The remaining portion of the pension benefit is retained by the participant to support their own retirement needs. It is important to note that the Arizona Waiver of Qualified Joint and Survivor Annuity JSASA applies to retirement plans governed by the Employee Retirement Income Security Act (ERICA), which includes most private-sector pension plans. This waiver ensures compliance with federal regulations and allows retirees to make informed decisions about their pension benefits. Retirement plan participants should carefully evaluate their financial situation, spouse's financial independence, and long-term goals before deciding whether to exercise a waiver of the JSA provision in Arizona. Consulting with a financial advisor or retirement specialist is highly recommended understanding the potential risks and advantages involved when making this significant retirement planning decision.

Arizona Waiver of Qualified Joint and Survivor Annuity - QJSA

Description

How to fill out Arizona Waiver Of Qualified Joint And Survivor Annuity - QJSA?

Are you presently within a situation that you will need documents for either enterprise or specific reasons just about every working day? There are a lot of legitimate document layouts available on the net, but discovering types you can trust is not straightforward. US Legal Forms offers a large number of kind layouts, like the Arizona Waiver of Qualified Joint and Survivor Annuity - QJSA, that are written to fulfill federal and state demands.

When you are previously familiar with US Legal Forms site and possess a free account, simply log in. Following that, you may obtain the Arizona Waiver of Qualified Joint and Survivor Annuity - QJSA design.

If you do not come with an account and want to start using US Legal Forms, follow these steps:

- Discover the kind you will need and ensure it is for that appropriate city/area.

- Utilize the Review key to examine the shape.

- See the information to actually have chosen the appropriate kind.

- In case the kind is not what you`re seeking, utilize the Look for field to find the kind that suits you and demands.

- When you discover the appropriate kind, click on Get now.

- Choose the rates program you would like, fill in the necessary info to make your bank account, and pay money for an order utilizing your PayPal or charge card.

- Decide on a hassle-free file file format and obtain your backup.

Discover every one of the document layouts you may have bought in the My Forms menu. You may get a additional backup of Arizona Waiver of Qualified Joint and Survivor Annuity - QJSA anytime, if necessary. Just go through the essential kind to obtain or print out the document design.

Use US Legal Forms, probably the most considerable variety of legitimate varieties, in order to save some time and prevent blunders. The support offers appropriately made legitimate document layouts that you can use for a range of reasons. Generate a free account on US Legal Forms and start creating your way of life a little easier.