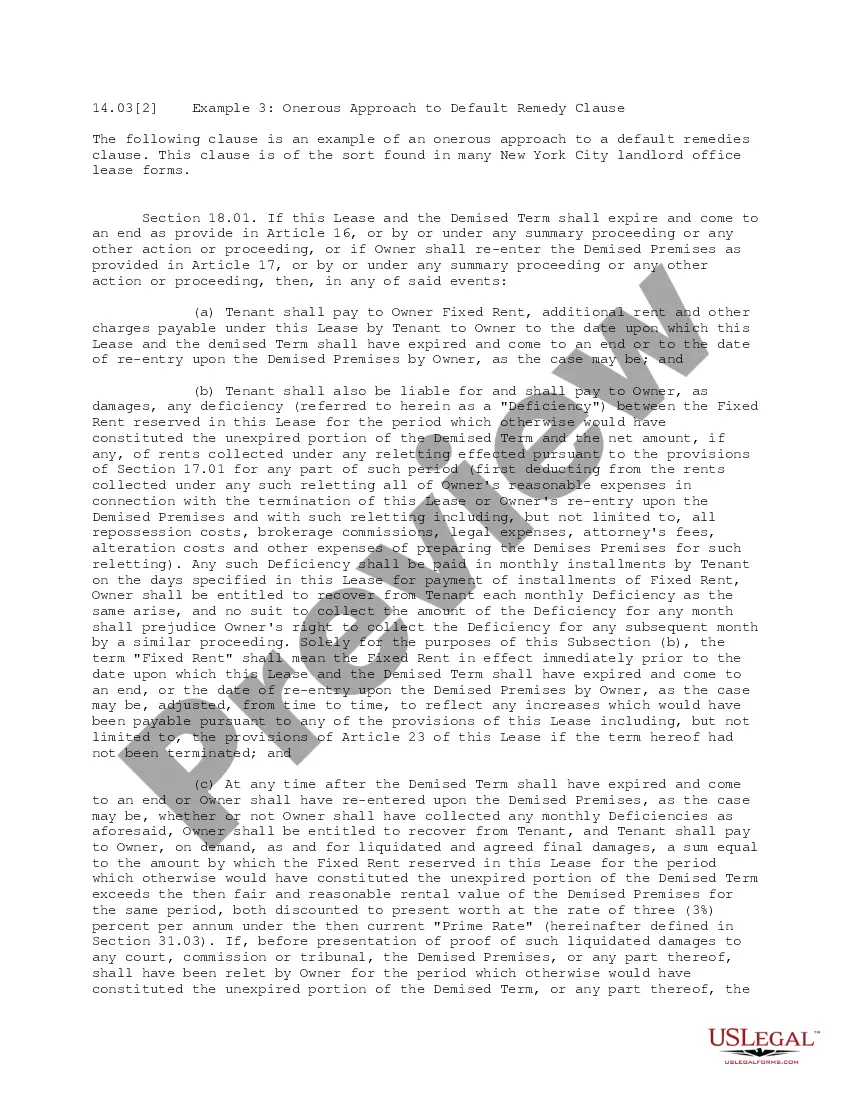

This office lease form is a standard default remedy clause, providing for the collection of the difference between the rent due and owing under the lease and the rents collected in the event of mitigation.

Arizona Default Remedy Clause

Category:

State:

Multi-State

Control #:

US-OL14031

Format:

Word;

PDF

Instant download

Description

How to fill out Default Remedy Clause?

If you want to full, download, or print out lawful document layouts, use US Legal Forms, the largest variety of lawful forms, which can be found on the web. Make use of the site`s basic and handy search to find the documents you want. Numerous layouts for enterprise and person purposes are categorized by categories and says, or keywords and phrases. Use US Legal Forms to find the Arizona Default Remedy Clause with a few click throughs.

Should you be already a US Legal Forms consumer, log in to your accounts and click the Download option to get the Arizona Default Remedy Clause. You can also entry forms you previously acquired from the My Forms tab of the accounts.

If you use US Legal Forms for the first time, refer to the instructions below:

- Step 1. Be sure you have selected the shape to the proper city/nation.

- Step 2. Make use of the Preview solution to look through the form`s content material. Never forget to read through the information.

- Step 3. Should you be not happy with the type, take advantage of the Look for area on top of the display to get other variations from the lawful type format.

- Step 4. Once you have identified the shape you want, click the Get now option. Select the costs program you like and include your qualifications to sign up for the accounts.

- Step 5. Process the purchase. You can use your bank card or PayPal accounts to accomplish the purchase.

- Step 6. Choose the file format from the lawful type and download it in your device.

- Step 7. Complete, modify and print out or sign the Arizona Default Remedy Clause.

Every lawful document format you purchase is the one you have eternally. You possess acces to every single type you acquired within your acccount. Go through the My Forms portion and select a type to print out or download again.

Be competitive and download, and print out the Arizona Default Remedy Clause with US Legal Forms. There are many specialist and status-distinct forms you may use for your enterprise or person requirements.

Form popularity

FAQ

Remedies for Breach of Contract If a breach of contract occurs, then the injured party may be offered a remedy in the form of legal remedies, or money damages, equitable remedies, or restitution by Arizona courts.

B. The landlord or the tenant may terminate a month-to-month tenancy by a written notice given to the other at least thirty days prior to the periodic rental date specified in the notice.

Unless there is a three-day right of rescission written expressly into the contract, there is no three-day right of rescission or ?cooling-off? period under Arizona law.

47-2725 - Statute of limitations in contracts for sale. A. An action for breach of any contract for sale must be commenced within four years after the cause of action has accrued. By the original agreement the parties may reduce the period of limitation to not less than one year but may not extend it.

5 Common Remedies for a Breach of Contract #1. Compensatory Damages. Compensatory damages are the most common damages awarded in breach of contract cases. ... #2. Liquidated Damages. ... #3. Rescission. ... #4. Specific Performance. ... #5. Injunction. ... Have a Contract that has Been Breached? We Are Here to Help.

This includes payment for monetary losses, property damage, lost revenue, reputation tarnishment, and more. Arizona law, specifically ARS 12-341.01 allows a plaintiff to collect attorney's fees related to a breach of contract claim. However, it also allows the defendant to collect attorney's fees if they win the case.

§ 33-1324(A)(1)); Maintain all appliances must be in working order (A.R.S. § 33-1324(A)(4)); and. Provide running water, reasonable amounts of hot water, and heating and air-conditioning when required by the weather (A.R.S.

Defenses that may excuse a breach of contract include duress, fraud and misrepresentation, mistake, lack of consideration and the statute of frauds.