A California Subordination Agreement for Existing Loan is a legal document that is used to allow a new loan to take precedence over an existing loan. It is a common practice for a lender or bank to require this type of agreement when they are providing a new loan that is of greater value or amount than an existing loan. This agreement states that the lender of the existing loan agrees to subordinate their loan to the new loan, meaning that in the event of default, the lender of the new loan will be paid back first. This agreement is typically used in situations where a borrower is taking out a second loan to pay off or refinance an existing loan. There are two types of California Subordination Agreement for Existing Loan: 1) Full Subordination Agreement and 2) Partial Subordination Agreement. A Full Subordination Agreement is used when a borrower wants to fully refinance or pay off an existing loan with a new loan. In this agreement, the lender of the existing loan agrees to subordinate their loan to the new loan and will not receive any money until the new loan is paid in full. A Partial Subordination Agreement is used when a borrower wants to pay off only part of the existing loan with the new loan. In this agreement, the lender of the existing loan agrees to subordinate their loan to the new loan, but will receive a portion of the proceeds from the new loan in order to pay off the remaining balance of the existing loan.

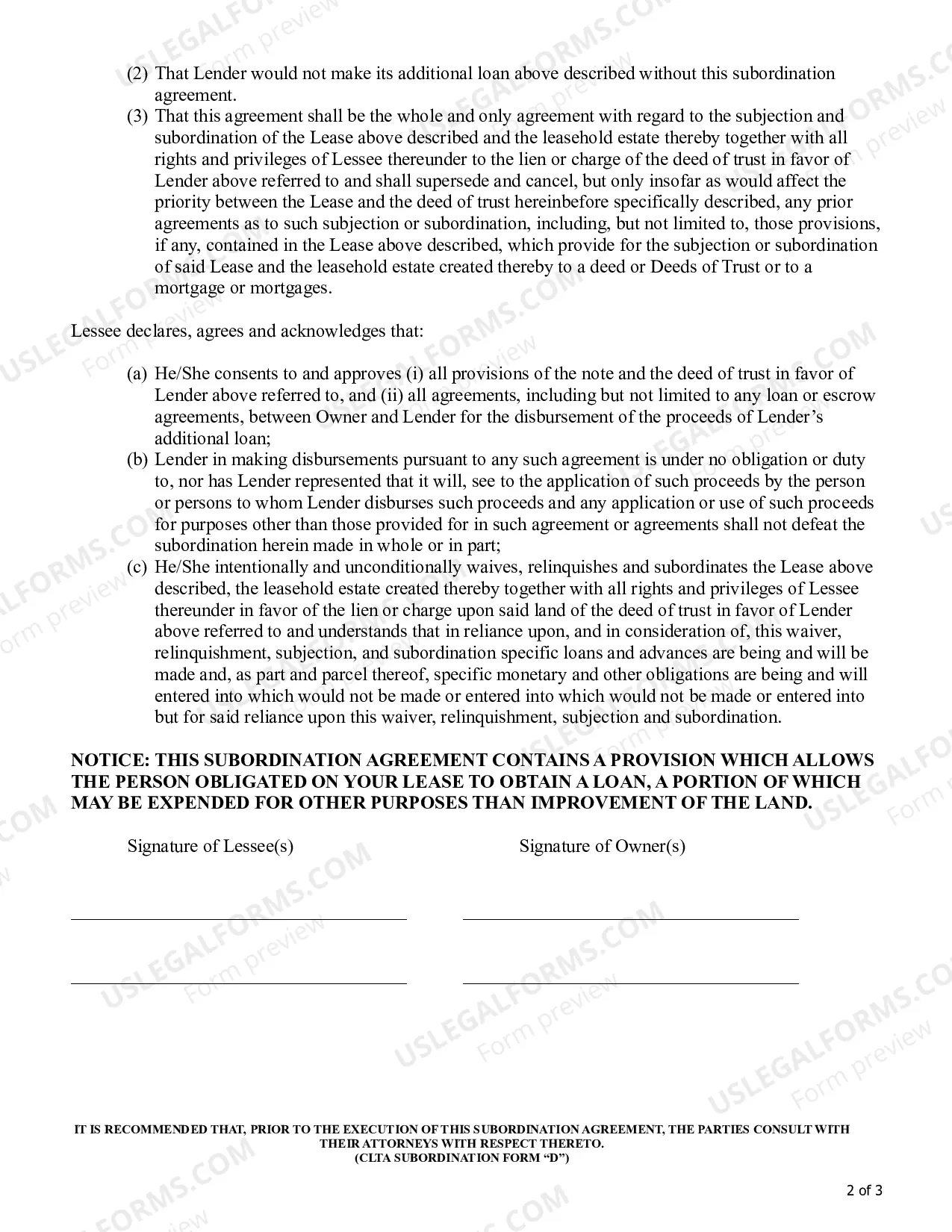

A California Subordination Agreement for Existing Loan is a legal document that is used to allow a new loan to take precedence over an existing loan. It is a common practice for a lender or bank to require this type of agreement when they are providing a new loan that is of greater value or amount than an existing loan. This agreement states that the lender of the existing loan agrees to subordinate their loan to the new loan, meaning that in the event of default, the lender of the new loan will be paid back first. This agreement is typically used in situations where a borrower is taking out a second loan to pay off or refinance an existing loan. There are two types of California Subordination Agreement for Existing Loan: 1) Full Subordination Agreement and 2) Partial Subordination Agreement. A Full Subordination Agreement is used when a borrower wants to fully refinance or pay off an existing loan with a new loan. In this agreement, the lender of the existing loan agrees to subordinate their loan to the new loan and will not receive any money until the new loan is paid in full. A Partial Subordination Agreement is used when a borrower wants to pay off only part of the existing loan with the new loan. In this agreement, the lender of the existing loan agrees to subordinate their loan to the new loan, but will receive a portion of the proceeds from the new loan in order to pay off the remaining balance of the existing loan.