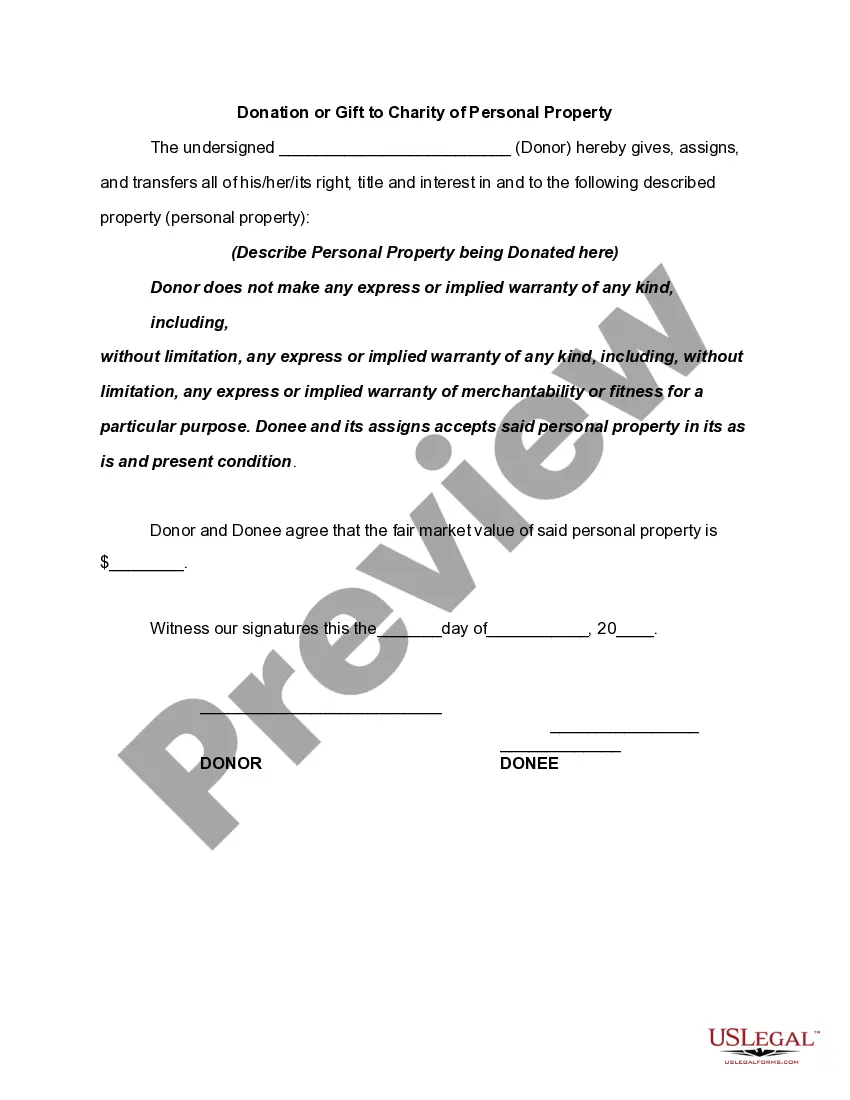

California Donation or Gift to Charity of Personal Property is a process in which an individual or entity voluntarily transfers their personal property to a nonprofit organization without receiving anything in return. It is a generous act undertaken by individuals, businesses, or estates to support charitable causes and make a positive impact on society. This type of donation encompasses a wide range of personal property, including but not limited to furniture, artwork, vehicles, clothing, electronics, and household goods. The donated items can be new or used, as long as they are in good condition and deemed usable by the receiving charity. Donations of personal property are different from monetary donations, as they involve transferring tangible assets to the charitable organization. The process of donating personal property to charity in California involves several steps. Firstly, the donor identifies a reputable nonprofit organization that aligns with their charitable goals and accepts personal property donations. It is important to select an organization that is tax-exempt under Section 501(c)(3) of the Internal Revenue Code, as this ensures that the donation qualifies for potential tax deductions. Once the recipient organization is chosen, the donor contacts them to express their intention to donate personal property. In some cases, the charity may have specific guidelines or restrictions on the types of items they accept. It is advisable to consult with the organization prior to making the donation to determine if the item meets their criteria. After confirming acceptance, the donor arranges for the delivery of the personal property to the charitable organization. If the donated items are cumbersome or voluminous, the donor may need to coordinate logistics with the organization to ensure a smooth transfer. In certain cases, the organization may offer pick-up services for larger donations, making it more convenient for the donor. Upon receipt of the donated personal property, the charity provides the donor with a receipt or acknowledgement letter that confirms the donation. This document serves as proof for the donor to claim a tax deduction for the fair market value of the donated items, as per the guidelines set by the Internal Revenue Service (IRS). It is important to note that California also provides additional benefits for donors who contribute to certain qualified charitable organizations, such as credits against state income tax liability. These credits can help offset the tax burden associated with the donation, further encouraging individuals to contribute to charitable causes. While there are no specific types of California Donation or Gift to Charity of Personal Property, the process remains consistent across various nonprofits and individuals. The main distinction lies in the specific charitable organizations chosen and the type of personal property donated, both of which vary greatly depending on the donor's preferences and the mission of the organization.

California Donation or Gift to Charity of Personal Property

Description

How to fill out California Donation Or Gift To Charity Of Personal Property?

Are you presently within a placement that you need paperwork for sometimes business or personal uses almost every day time? There are tons of legal record layouts accessible on the Internet, but discovering ones you can depend on isn`t easy. US Legal Forms offers a large number of type layouts, just like the California Donation or Gift to Charity of Personal Property, that are created to fulfill state and federal needs.

When you are currently informed about US Legal Forms web site and possess an account, just log in. Afterward, it is possible to download the California Donation or Gift to Charity of Personal Property format.

Unless you have an accounts and would like to begin to use US Legal Forms, follow these steps:

- Find the type you want and make sure it is to the appropriate city/state.

- Use the Review key to analyze the form.

- Browse the outline to actually have chosen the proper type.

- In the event the type isn`t what you are seeking, utilize the Research industry to obtain the type that suits you and needs.

- Once you find the appropriate type, just click Get now.

- Choose the pricing prepare you would like, submit the specified details to generate your account, and purchase the transaction making use of your PayPal or charge card.

- Select a practical document structure and download your backup.

Find all of the record layouts you might have bought in the My Forms menus. You may get a more backup of California Donation or Gift to Charity of Personal Property at any time, if required. Just click the needed type to download or produce the record format.

Use US Legal Forms, by far the most extensive assortment of legal kinds, to save lots of efforts and avoid faults. The service offers professionally created legal record layouts that can be used for an array of uses. Produce an account on US Legal Forms and begin creating your lifestyle a little easier.