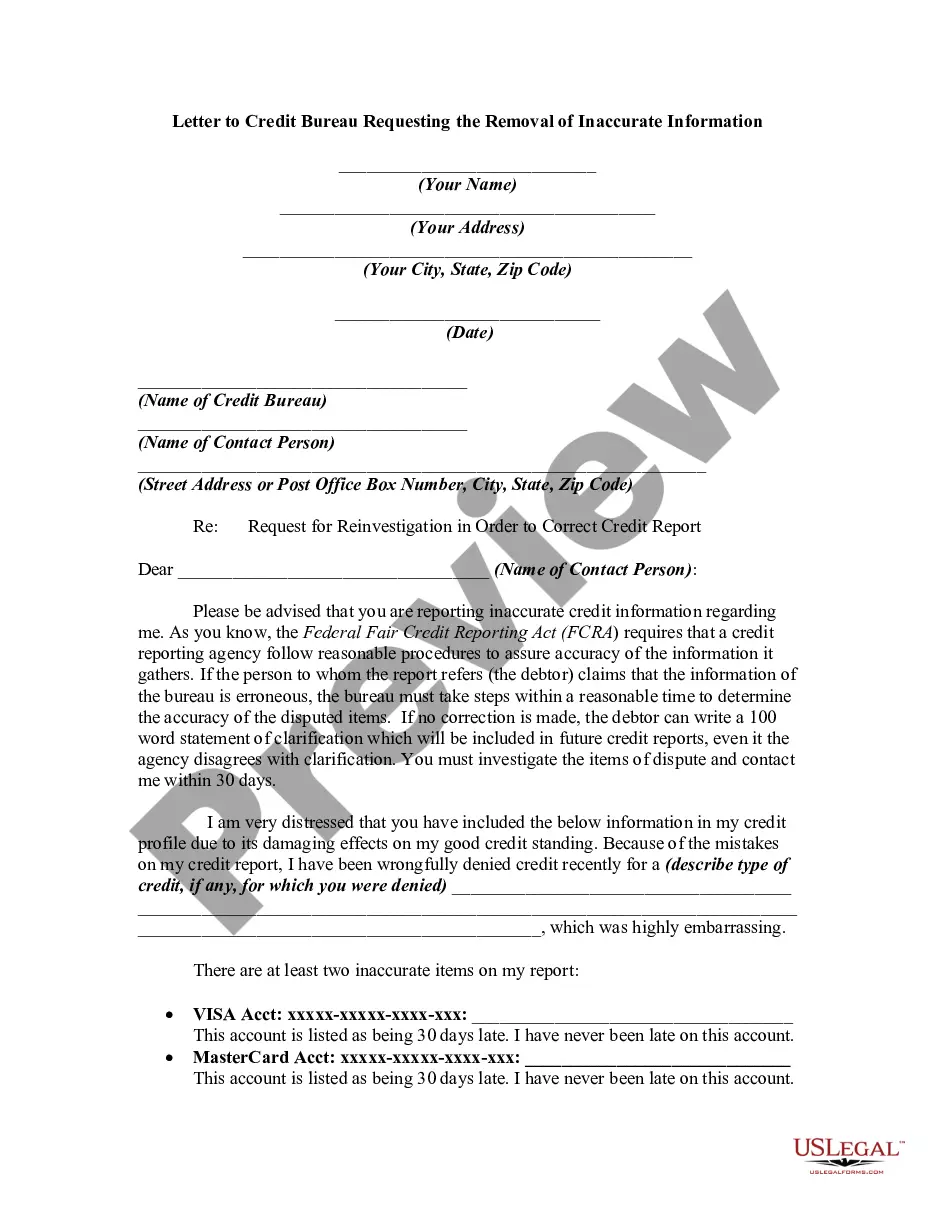

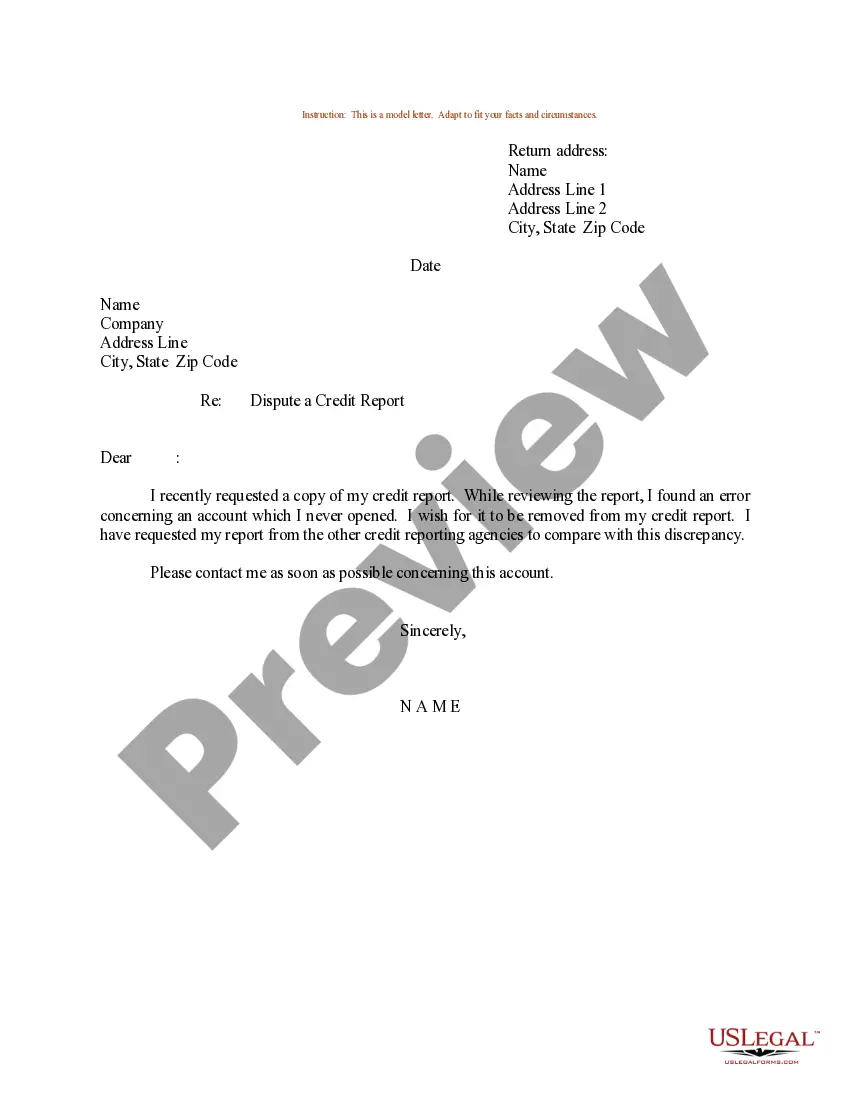

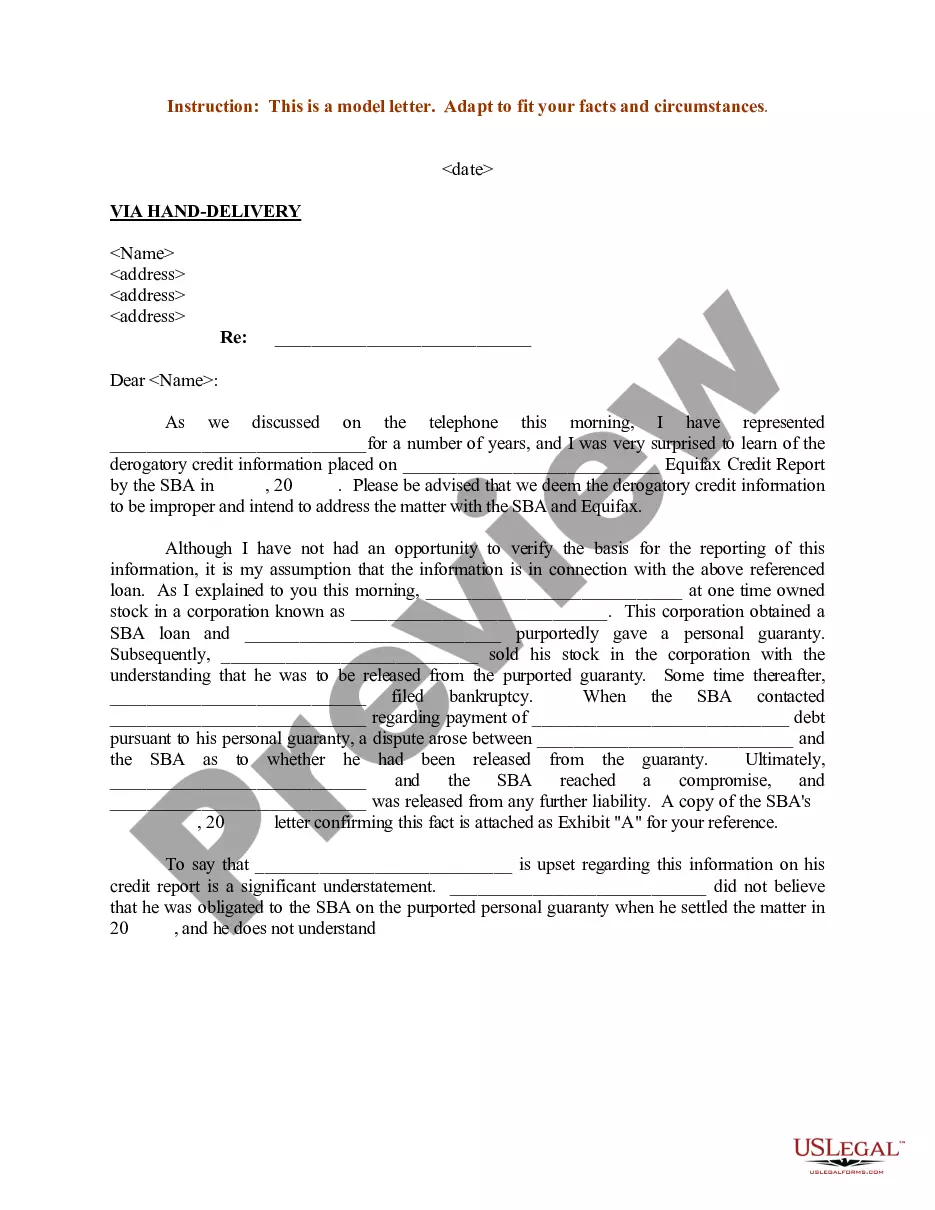

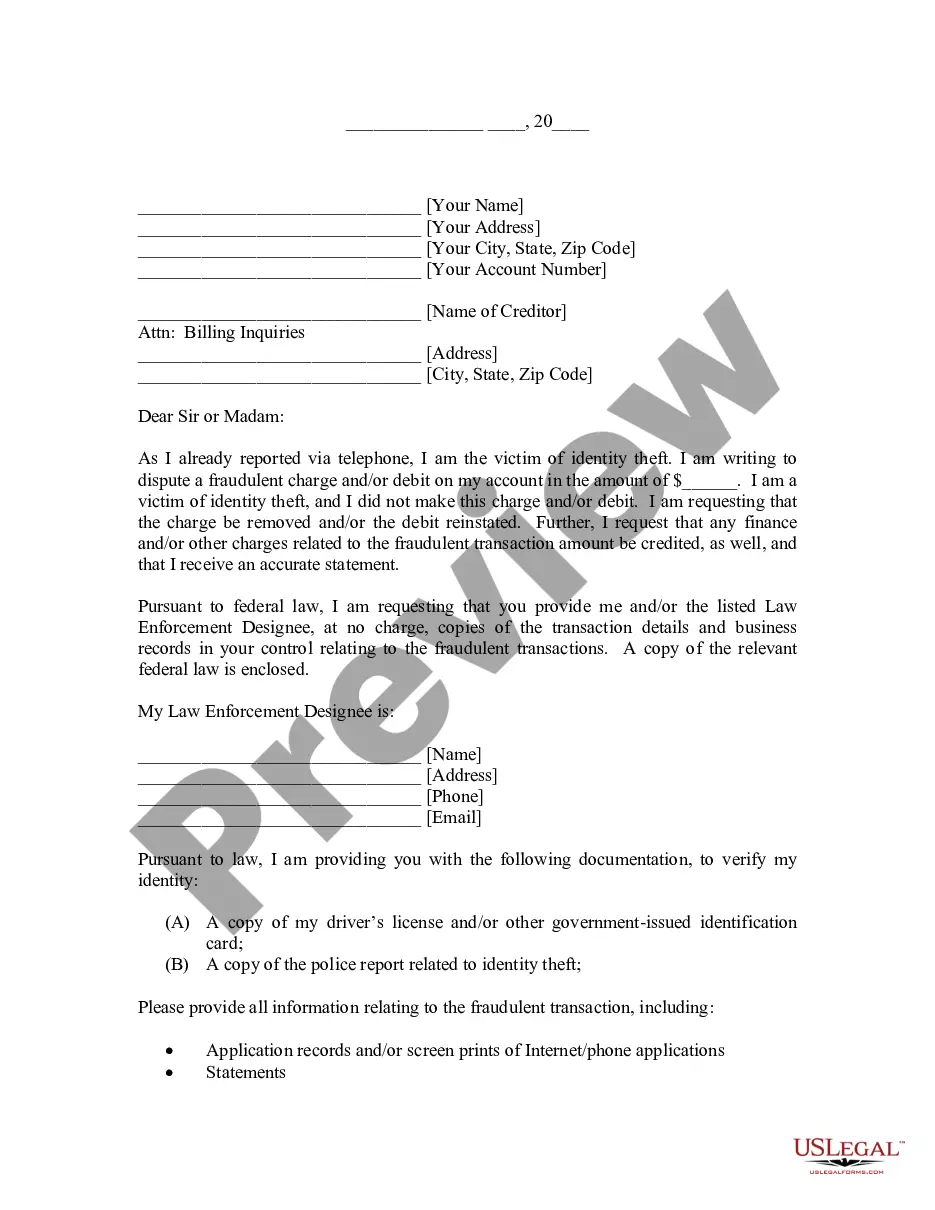

Some information obtained by credit reporting bureaus is based on statements made by persons, such as neighbors who were interviewed by the bureau's investigator. Needless to say, these statements are not always correct and are sometimes the result of gossip. In any event, such statements may go on the records of the bureau without further verification and may be furnished to a client of the bureau who will regard the statements as accurate. A person has the limited right to request an agency to disclose the nature and substance of the information possessed by the bureau to see if the information is accurate. If the person claims that the information of the bureau is erroneous, the bureau must take steps within a reasonable time to determine the accuracy of the disputed items.

California Letter from Consumer to Credit Reporting Agency Disputing Information in File

Description

How to fill out Letter From Consumer To Credit Reporting Agency Disputing Information In File?

Locating the appropriate valid document template can be challenging. Clearly, there are numerous templates accessible online, but how can you identify the specific template you need? Utilize the US Legal Forms platform. The service provides thousands of templates, including the California Letter from Consumer to Credit Reporting Agency Disputing Information in File, suitable for both business and personal purposes. All the forms are vetted by professionals and comply with state and federal regulations.

If you are already registered, Log In to your account and click on the Acquire option to locate the California Letter from Consumer to Credit Reporting Agency Disputing Information in File. Use your account to review the legal forms you may have previously acquired. Navigate to the My documents tab of your account and obtain another copy of the document you need.

If you are a new user of US Legal Forms, here are simple instructions to follow: First, ensure you have chosen the correct form for your area/county. You can examine the form using the Review option and read the form description to confirm this is the right choice for you. If the form does not meet your needs, utilize the Search feature to find the appropriate form. When you are certain that the form is suitable, select the Buy now option to obtain the form. Choose your payment method and enter the necessary information. Create your account and complete the transaction using your PayPal account or credit card. Select the file format and download the legal document template to your device. Complete, modify, print, and sign the obtained California Letter from Consumer to Credit Reporting Agency Disputing Information in File. US Legal Forms is the largest repository of legal forms where you can find various document templates. Take advantage of the service to download professionally crafted documents that meet state requirements.

Use the service to download professionally crafted documents that comply with state regulations.

- Locating the right valid document template can be challenging.

- US Legal Forms provides thousands of templates.

- All forms are vetted by professionals.

- If you are already registered, Log In to your account.

- Utilize the Search feature to find the appropriate form.

- US Legal Forms is the largest repository of legal forms.

Form popularity

FAQ

Are 609 letters effective? There's no evidence to suggest a 609 letter is more or less effective than the usual process of disputing an error on your credit report?it's just another method of gathering information and seeking verification of the accuracy of the report.

A 609 dispute letter points out some inaccurate, negative, or erroneous information on your credit report, forcing the credit company to change them. You'll find countless 609 letter templates online; however, they do not always promise that your dispute will be successful.

If you identify an error on your credit report, you should start by disputing that information with the credit reporting company (Experian, Equifax, and/or Transunion). You should explain in writing what you think is wrong, why, and include copies of documents that support your dispute.

I am requesting that this item be removed [or request another specific change to correct the information]. [List and describe any other items you are disputing.] Enclosed is documentation supporting my request: [describe the documents you're sending, for instance: my credit report, with the disputed items circled.]

Steps for writing and submitting a 609 letter You can use this guide on how to read a credit report. Note that your 609 letter doesn't need to be notarized. It is recommend sending the letter via certified mail through the U.S. Post Office. This way, you can receive a mail receipt confirming delivery.

Under section 609 of the FCRA, a consumer reporting agency must, upon a consumer's request, disclose to the consumer information in the consumer's file.

Asked by: Mr. Jillian Rau | Last update: February 9, 2022 Score: 4.1/5 (71 votes) Section 623 of the FRCA allows you to dispute any inaccurate information on your credit report directly with the original creditor, as long as you've already completed the process with the credit bureau.