This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

California Promissory Note with no Payment Due Until Maturity and Interest to Compound Annually

Category:

State:

Multi-State

Control #:

US-01471BG

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Promissory Note With No Payment Due Until Maturity And Interest To Compound Annually?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a wide range of legal document templates that you can download or create.

With the website, you can discover numerous forms for business and individual purposes, organized by categories, states, or keywords. You can swiftly find the latest forms such as the California Promissory Note with no Payment Due Until Maturity and Interest Compounding Annually.

If you have a subscription, Log In and download the California Promissory Note with no Payment Due Until Maturity and Interest Compounding Annually from the US Legal Forms library. The Download button will appear on each form you view. You have access to all previously saved forms within the My documents section of your account.

Proceed with the transaction. Use your credit card or PayPal account to complete the transaction.

Select the format and download the form onto your device. Make modifications. Complete, edit, and print and sign the saved California Promissory Note with no Payment Due Until Maturity and Interest Compounding Annually. All forms you add to your account have no expiration date and are yours indefinitely. So, if you wish to download or create another copy, simply go to the My documents section and click on the form you need. Access the California Promissory Note with no Payment Due Until Maturity and Interest Compounding Annually with US Legal Forms, the most extensive library of legal document templates. Utilize numerous professional and state-specific templates that meet your business or personal needs and requirements.

- Ensure you have selected the correct form for your city/state.

- Click on the Review button to check the form's content.

- Examine the form outline to confirm you have selected the right form.

- If the form does not meet your requirements, use the Search box at the top of the screen to find one that does.

- If you are satisfied with the form, confirm your selection by clicking the Buy now button.

- Then, choose the pricing plan you prefer and provide your details to create your account.

Form popularity

FAQ

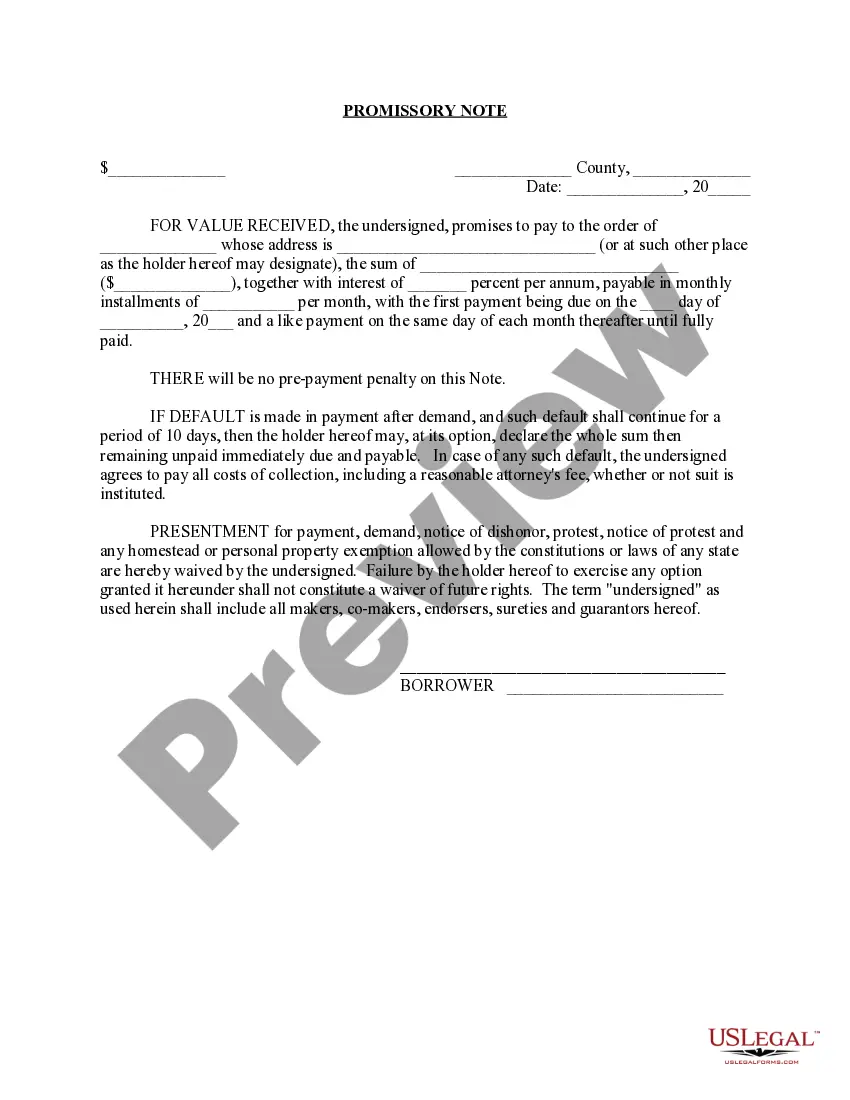

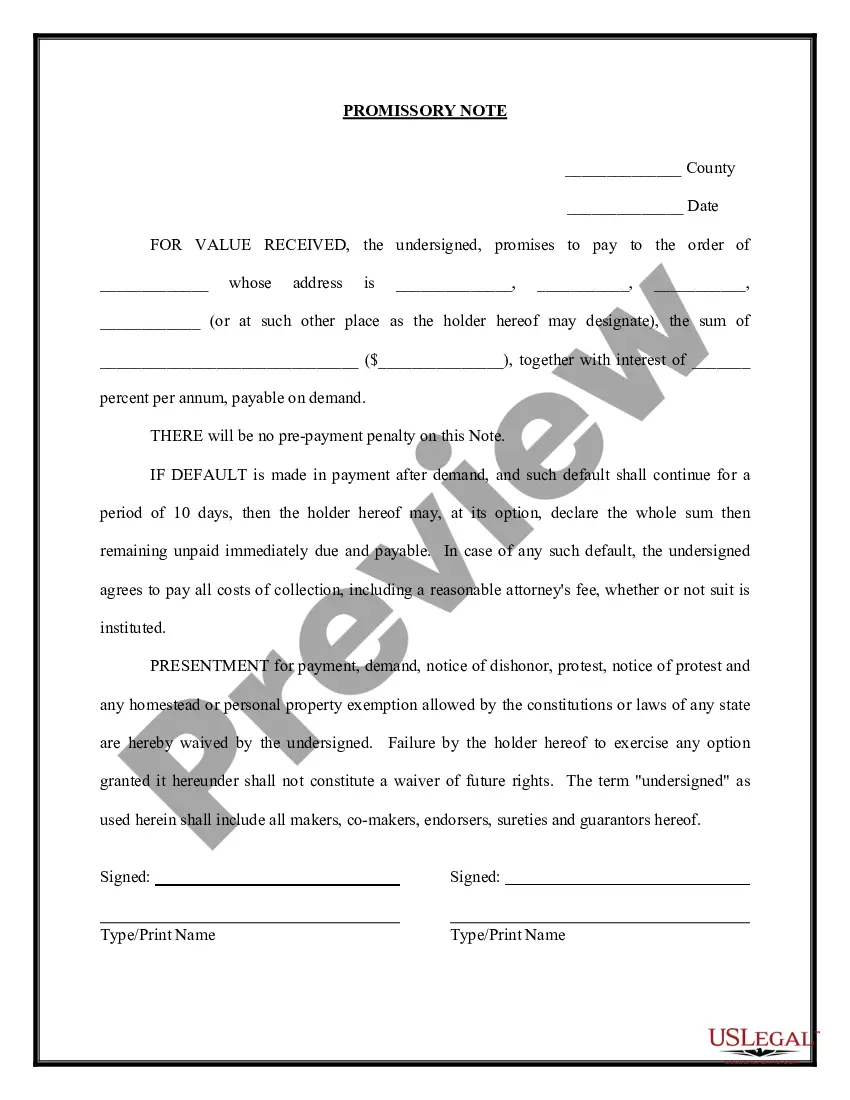

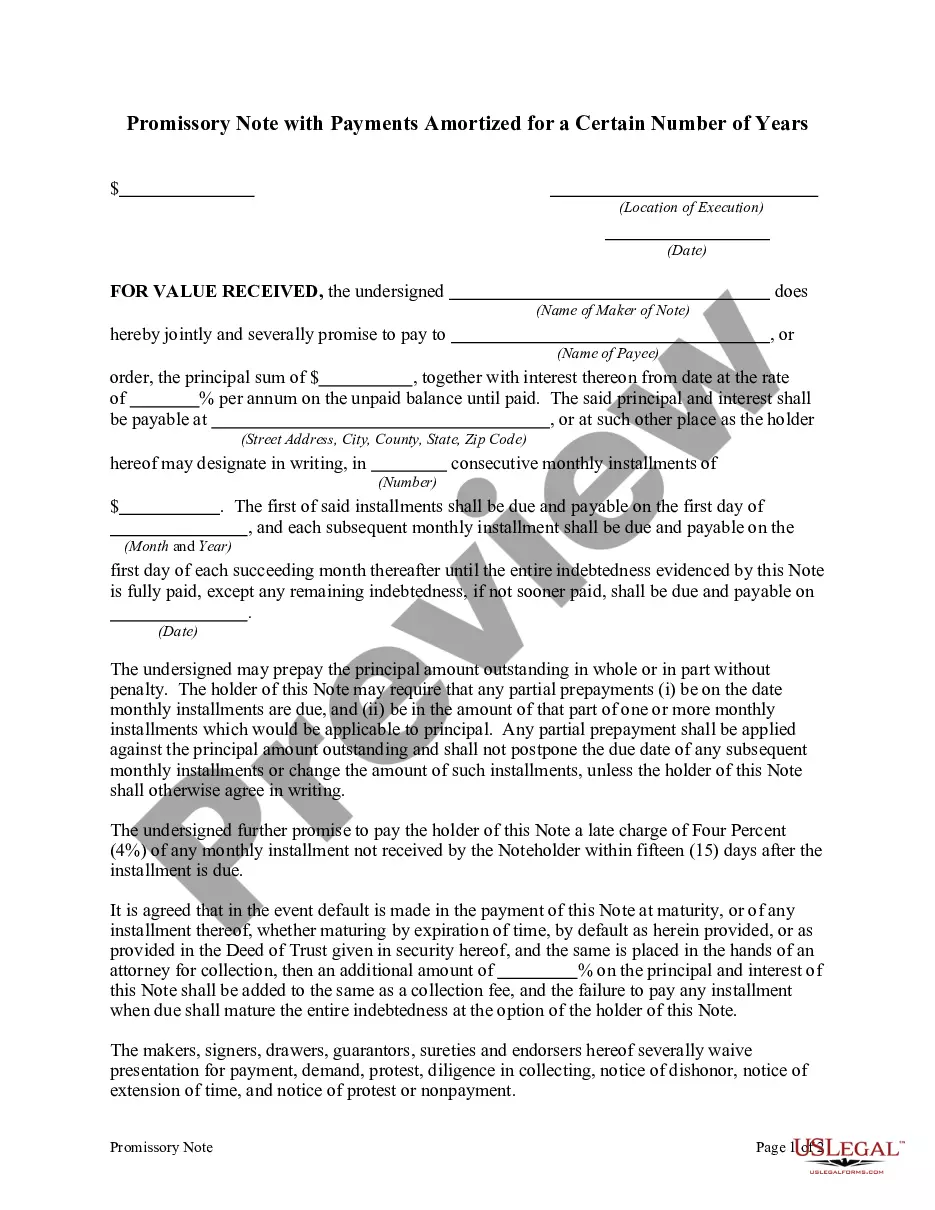

The maturity value of a California Promissory Note with no Payment Due Until Maturity and Interest to Compound Annually represents the total amount due at the end of the note's term. This amount includes the principal and any interest that has accrued over the life of the note. Understanding this value is crucial for borrowers and lenders alike, as it clarifies what will be owed upon maturity. By using the US Legal Forms platform, you can easily create and manage your promissory note to ensure all details are clear and compliant with California laws.

Promissory notes must include specific elements to be legally binding, such as the borrower's promise to repay the amount, the repayment schedule, and interest rate terms. In creating a California Promissory Note with no Payment Due Until Maturity and Interest to Compound Annually, it's crucial to clearly state the maturity date and how interest accumulates. It's also important to sign the document in front of a witness or notary to strengthen its validity. Familiarizing yourself with these rules helps ensure your agreement is enforceable.

Yes, promissory notes are legally binding documents in California, provided they meet all necessary legal criteria. A California Promissory Note with no Payment Due Until Maturity and Interest to Compound Annually creates enforceable obligations for both parties involved. This legal backing protects lenders while assuring borrowers of their commitments.

A properly executed promissory note can hold up in court if disputes arise. Courts generally uphold the terms of a California Promissory Note with no Payment Due Until Maturity and Interest to Compound Annually, as long as it follows the law. Having a well-documented agreement minimizes risks and strengthens your position in legal proceedings.

A promissory note may be considered invalid if it lacks essential elements like signatures, proper wording, or a clear lending purpose. Additionally, if it violates state laws or public policy, it may lose validity. A California Promissory Note with no Payment Due Until Maturity and Interest to Compound Annually must adhere to specific legal formulations to remain enforceable.

Yes, promissory notes are generally enforceable in California, provided they meet certain legal requirements. A California Promissory Note with no Payment Due Until Maturity and Interest to Compound Annually can be upheld in court if properly drafted and executed. Ensuring that all parties understand the terms strengthens the note's legal standing.

Typically, a promissory note should include a maturity date to ensure clarity regarding when the debt must be settled. For a California Promissory Note with no Payment Due Until Maturity and Interest to Compound Annually, incorporating a specific maturity date provides both parties with a clear understanding of their obligations and timelines. This detail enhances the document's structure and is vital for enforceability.

In California, promissory notes do not have a statutory expiration date. However, the validity of a California Promissory Note with no Payment Due Until Maturity and Interest to Compound Annually can be affected if not enforced within a reasonable time. It’s essential to stay vigilant to avoid potential issues with enforceability based on the statute of limitations.

Yes, interest can compound on a promissory note. In the case of a California Promissory Note with no Payment Due Until Maturity and Interest to Compound Annually, the interest accumulates over time, increasing the total amount due at maturity. This feature allows for a more substantial return on investment, benefiting both borrowers and lenders.

Yes, a promissory note can be structured without a maturity date, resulting in an indefinite repayment timeline. While this can provide flexibility, it may lead to confusion regarding when repayment should occur. A California Promissory Note with no Payment Due Until Maturity and Interest to Compound Annually exemplifies a unique agreement where borrowers and lenders need to set clear expectations. Clarifying such terms upfront can prevent disputes later.