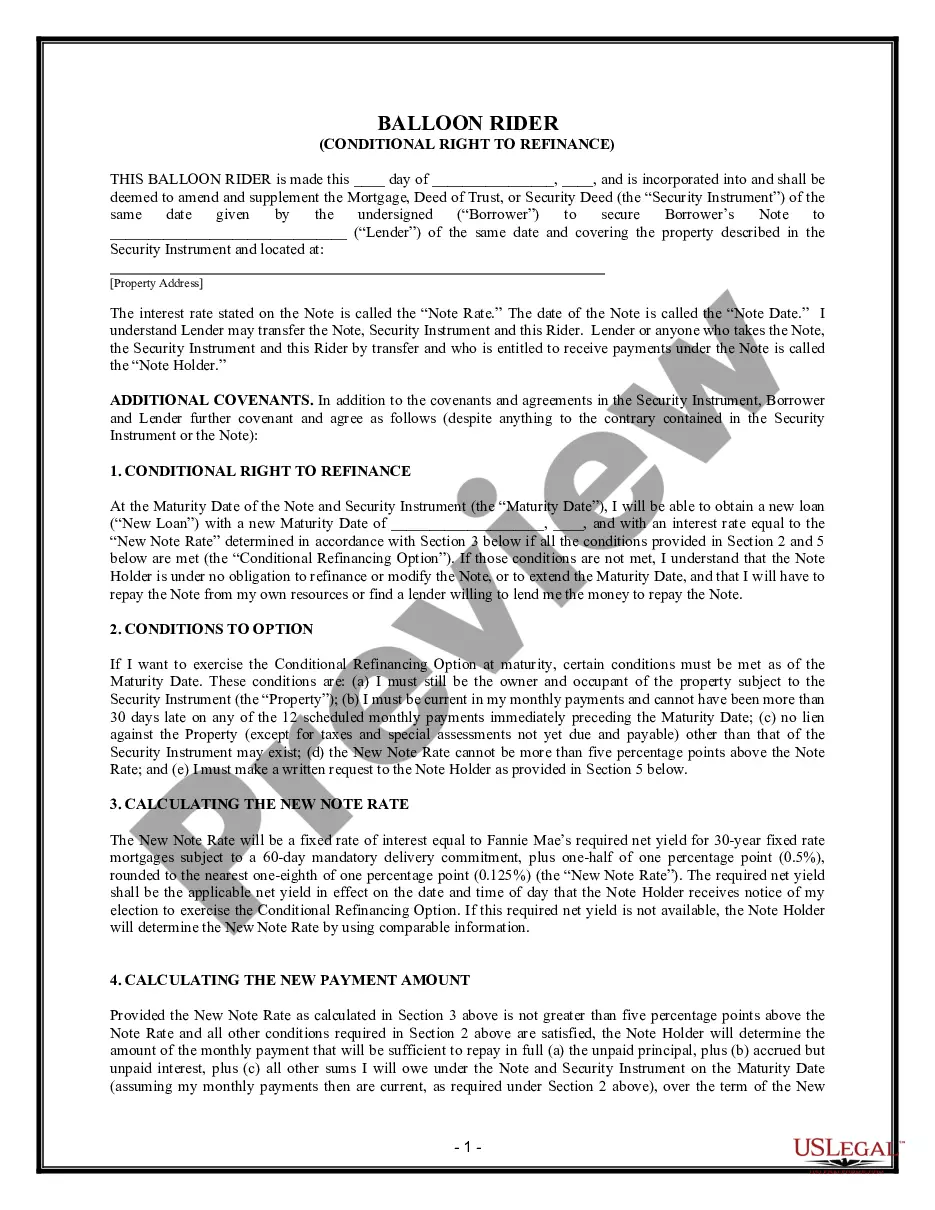

US Legal Forms - one of the largest collections of legal documents in the United States - offers a variety of legal paper templates that you can download or print. By utilizing the site, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can find the most recent forms, such as the California Commercial Mortgage as Security for Balloon Promissory Note in just seconds.

If you already possess a monthly subscription, Log In and download the California Commercial Mortgage as Security for Balloon Promissory Note from your US Legal Forms repository. The Download option will appear on each document you view. You can access all previously downloaded forms in the My documents section of your account.

If you are using US Legal Forms for the first time, here are simple steps to help you get started: Ensure you have chosen the correct form for your city/county. Select the Review option to examine the form's details. Read the form description to confirm you have selected the correct one. If the form does not meet your needs, utilize the Search field at the top of the screen to find one that does. If you are satisfied with the form, confirm your choice by clicking the Buy now button. Then, choose the payment plan you prefer and provide your information to register for an account. Complete the transaction. Use your Visa or Mastercard or PayPal account to finalize the transaction. Select the format and download the form to your device. Make modifications. Fill out, edit, print, and sign the downloaded California Commercial Mortgage as Security for Balloon Promissory Note. Every template you add to your account has no expiration date and belongs to you permanently. Therefore, if you wish to download or print another copy, simply visit the My documents section and click on the form you need.

- Access the California Commercial Mortgage as Security for Balloon Promissory Note with US Legal Forms, one of the most extensive collections of legal document templates.

- Utilize a multitude of professional and state-specific templates that meet your business or personal needs and requirements.