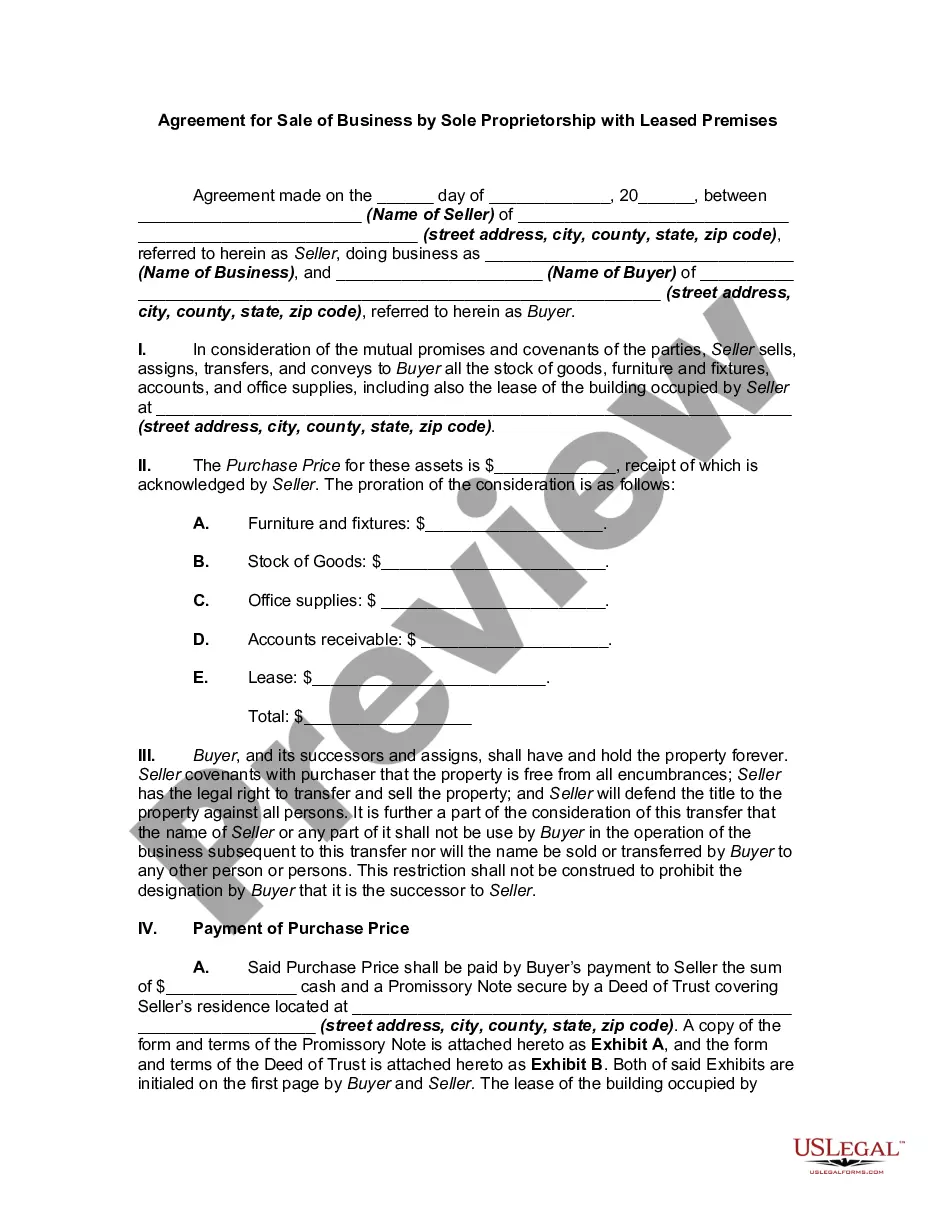

This form involves the sale of a small business where the real estate on which the Business is located is leased from a third party. This form assumes that the Seller has received the right to assign the lease from the lessor/owner.

California Agreement for Sale of Business by Sole Proprietorship with Leased Premises is a legally binding document that outlines the terms and conditions for the sale of a business owned and operated by a sole proprietor. It is specifically designed for transactions involving businesses that operate on leased premises in the state of California. This agreement ensures that the buyer and seller have a clear understanding of their rights and responsibilities, minimizing the risk of any disputes arising in the future. It covers various aspects of the sale, including the purchase price, payment terms, transfer of assets, liabilities, and lease agreement. Typically, there are two main types of California Agreement for Sale of Business by Sole Proprietorship with Leased Premises: 1. Asset Sale Agreement: In this type of agreement, the buyer purchases specific assets of the business, such as equipment, inventory, customer lists, and goodwill. The buyer may assume certain liabilities, but the seller retains ownership of the business entity, including any outstanding debts or legal obligations. 2. Stock Sale Agreement: This type of agreement involves the purchase of all outstanding shares of the business entity, including its assets, liabilities, and contractual obligations. The buyer becomes the new owner of the business, assuming all risks and responsibilities associated with the entity. Some relevant keywords associated with the California Agreement for Sale of Business by Sole Proprietorship with Leased Premises include: — Business salagreementen— - Sole proprietorship sale — Leased premise— - California business transaction — Purchase price negotiation— - Asset transfer — Liability assumptio— - Due diligence - Buyer's obligations — Seller's representations and warranties — Leastransferfe— - Non-compete clauses - Confidentiality agreements — Closing and post-closing procedures It is important to consult a legal professional experienced in California business law to ensure that the agreement complies with all relevant regulations and laws. Failure to do so may result in legal complications and potential financial loss for both parties involved in the transaction.California Agreement for Sale of Business by Sole Proprietorship with Leased Premises is a legally binding document that outlines the terms and conditions for the sale of a business owned and operated by a sole proprietor. It is specifically designed for transactions involving businesses that operate on leased premises in the state of California. This agreement ensures that the buyer and seller have a clear understanding of their rights and responsibilities, minimizing the risk of any disputes arising in the future. It covers various aspects of the sale, including the purchase price, payment terms, transfer of assets, liabilities, and lease agreement. Typically, there are two main types of California Agreement for Sale of Business by Sole Proprietorship with Leased Premises: 1. Asset Sale Agreement: In this type of agreement, the buyer purchases specific assets of the business, such as equipment, inventory, customer lists, and goodwill. The buyer may assume certain liabilities, but the seller retains ownership of the business entity, including any outstanding debts or legal obligations. 2. Stock Sale Agreement: This type of agreement involves the purchase of all outstanding shares of the business entity, including its assets, liabilities, and contractual obligations. The buyer becomes the new owner of the business, assuming all risks and responsibilities associated with the entity. Some relevant keywords associated with the California Agreement for Sale of Business by Sole Proprietorship with Leased Premises include: — Business salagreementen— - Sole proprietorship sale — Leased premise— - California business transaction — Purchase price negotiation— - Asset transfer — Liability assumptio— - Due diligence - Buyer's obligations — Seller's representations and warranties — Leastransferfe— - Non-compete clauses - Confidentiality agreements — Closing and post-closing procedures It is important to consult a legal professional experienced in California business law to ensure that the agreement complies with all relevant regulations and laws. Failure to do so may result in legal complications and potential financial loss for both parties involved in the transaction.